Author’s Note

When I first started tracking household financial patterns across India, I noticed families were treating debt as a normal part of monthly budgeting. The professional who used her credit card for groceries represents thousands of similar stories I encounter regularly. This Household Debt Surge isn’t just about numbers – it’s about how we’ve unconsciously shifted from saving first to borrowing first. Through my work with families, I’ve seen how small debt decisions create lasting financial stress. My hope is that by understanding these patterns, we can make more intentional choices about when debt serves us versus when it controls us.

Key Takeaways

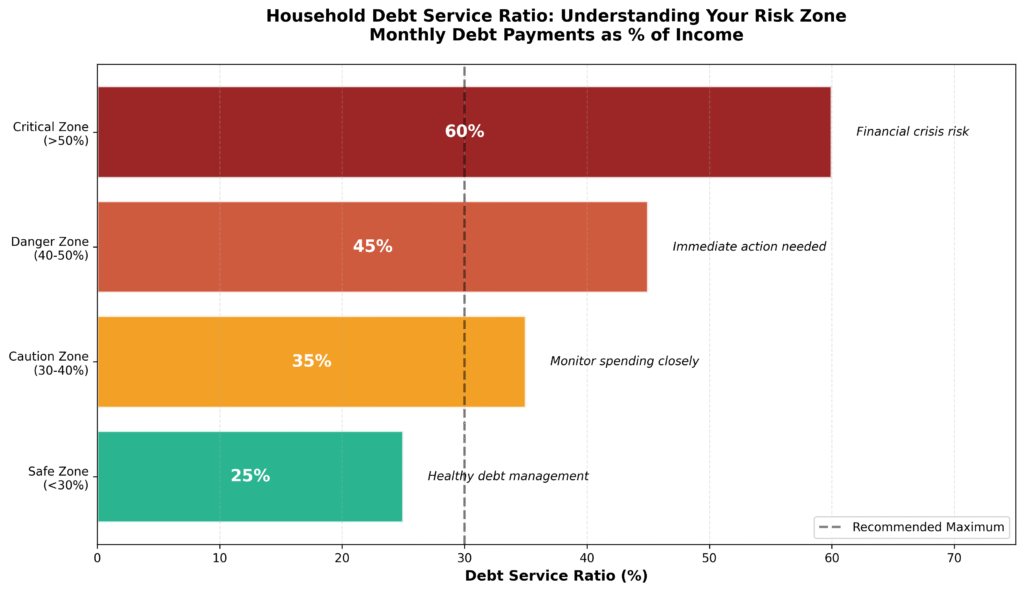

- Track your monthly credit card and loan payments as a percentage of income – if it exceeds 30%, you’re in the danger zone for debt dependency

- The current Household Debt Surge reflects a cultural shift where families normalize financing basic needs instead of adjusting spending to match income

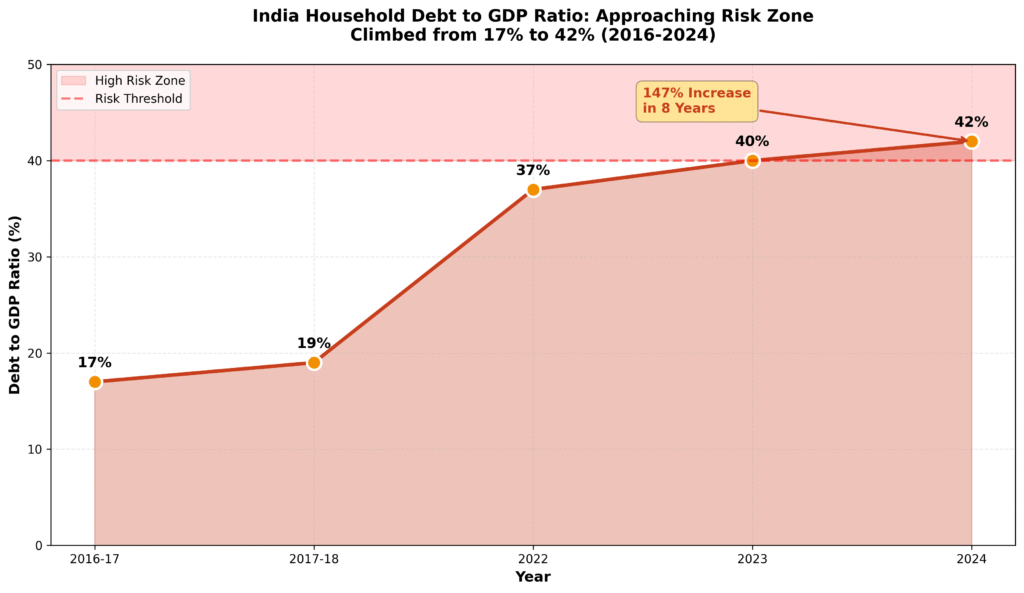

- With India’s household debt to GDP ratio reaching 42%, your family’s financial decisions now impact and reflect broader economic stability

- Create a 3-month emergency fund before using credit for any non-urgent expenses to break the cycle of financing everyday necessities

Understanding India’s Household Debt Surge Crisis

Most of us have stood in a grocery store checkout line, telling ourselves this purchase is just temporary. A professional found herself in exactly this situation, using her credit card for weekly grocery runs while waiting for her next salary hike. What began as ₹3,000 monthly grocery bills gradually expanded to ₹8,000 as household items and personal care products found their way into her cart. By the time she sought financial advice, she was paying ₹2,400 monthly just in minimum payments – nearly what she originally spent on groceries entirely.

Her wake-up call came with an important realization: she was paying interest on food consumed months earlier. This scenario reflects a broader pattern we see across Indian households today, where seemingly manageable expenses compound into significant financial burdens. The normalization of financing basic necessities has become so widespread that many families no longer recognize when they have crossed the line from convenience to dependency.

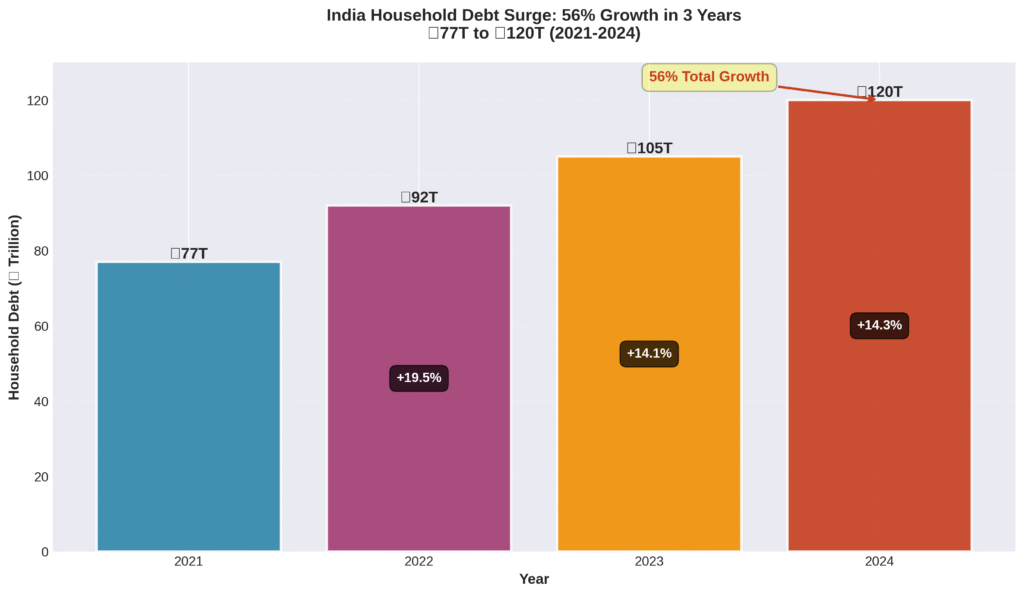

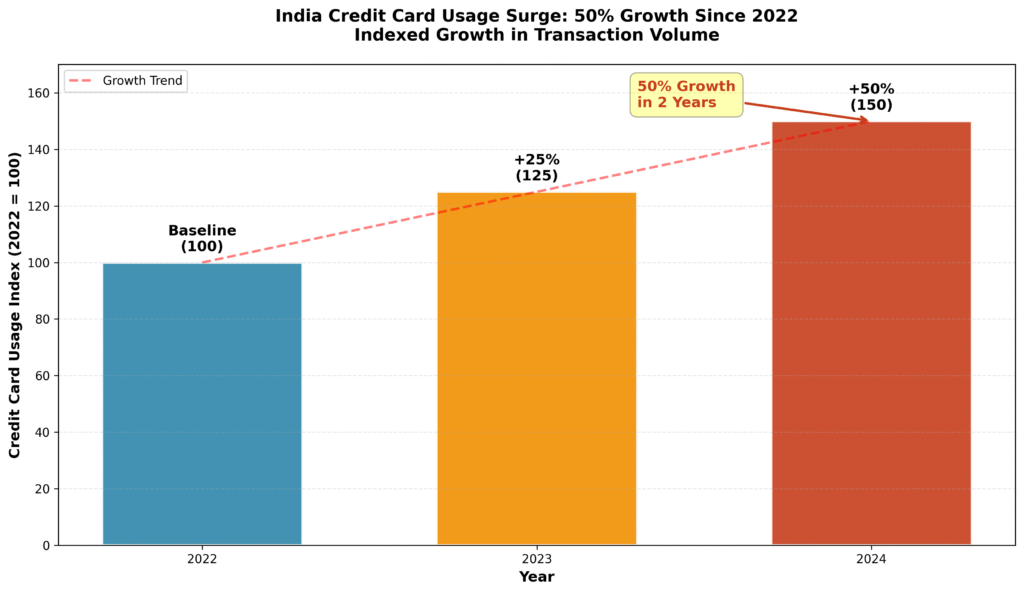

The numbers paint a revealing picture of how common this experience has become. Household debt in India reached 42% of GDP by the end of 2024, with total debt surging from ₹77 trillion to ₹120 trillion in just three years. Credit card usage alone increased by 50% since 2022, suggesting that more families are turning to borrowed money for everyday expenses. This household debt surge represents more than statistical growth – it signals a fundamental shift in how we manage our daily financial lives.

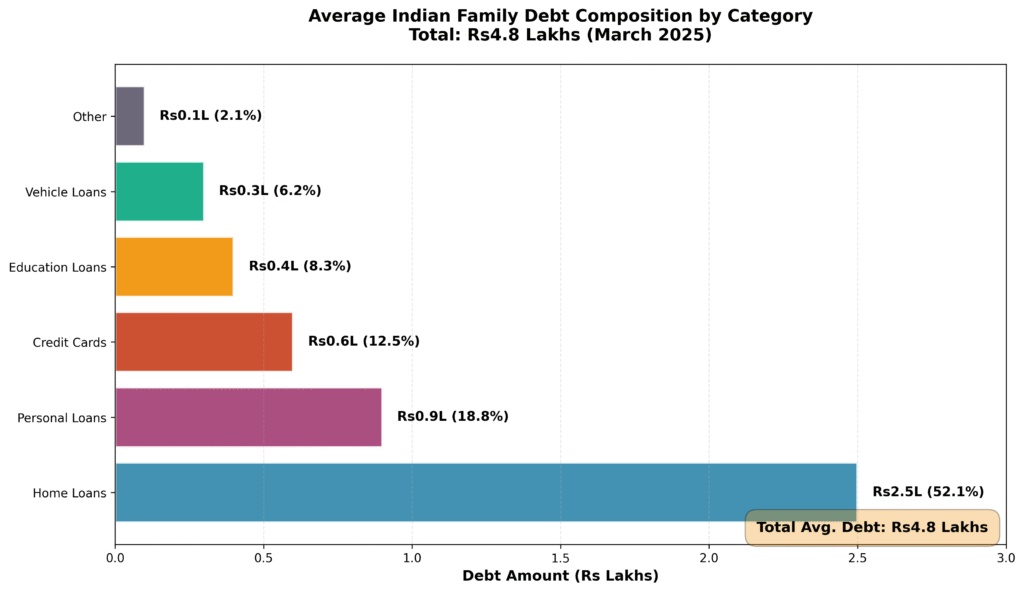

We find ourselves in an era where the average family debt has climbed to ₹4.8 lakh by March 2025, yet many households remain unaware of the long-term implications of their borrowing patterns. The convenience of digital payments and instant credit approvals has made it easier than ever to finance immediate needs, but this accessibility often masks the true cost of such decisions.

Understanding this landscape becomes crucial for anyone seeking to build lasting financial stability. The path forward requires recognizing how small, recurring debt decisions can fundamentally alter our financial trajectory and learning to distinguish between necessary financial tools and potentially harmful debt accumulation patterns.

How Household Debt Surge Impacts Indian Families

Most of us have experienced that moment when we realize our monthly expenses exceed our income, yet we continue living the same lifestyle through borrowed money. A family I recently met after they took their third personal loan in two years – this time for their daughter’s school fees and uniform expenses. They had started with a small education loan for coaching classes, then borrowed for a laptop for online learning, and finally needed another loan just to pay the school fees they could easily afford three years earlier. Each loan payment was manageable individually, but together they consumed 60% of their monthly income. The father confided that they now planned their child’s school activities around their loan EMI schedule, declining field trips and extra-curricular activities that they once considered essential.

This family’s experience is not unique; it reflects a wider trend across many households throughout India. When we examine the data, household debt grew at an annualized rate of 1.8 times between 2016-17 and 2017-18, jumping from ₹3.7 lakh crore to ₹6.74 lakh crore. The acceleration has only intensified since then, creating a web of financial obligations that many families struggle to untangle.

This broader crisis manifests in individual choices where financing basic family needs has become completely normalized. Parents justify educational loans for coaching classes, couples take personal loans for wedding expenses, and families use credit cards for monthly groceries when salaries run short. Each decision seems reasonable in isolation, but collectively they create a debt structure that fundamentally changes how families make life choices.

Average Family Debt Breakdown in India

The emotional toll extends far beyond the monthly EMI payments. Families find themselves constantly calculating whether they can afford experiences that were once automatic – a weekend outing, a child’s birthday celebration, or even basic healthcare needs. The stress of managing multiple loan payments often leads to relationship strain and anxiety about the future, creating a cycle where financial pressure impacts every aspect of family life.

Breaking free from this pattern requires understanding that debt elimination is not just about paying off balances – it involves restructuring our entire approach to family financial management. The debt avalanche method, combined with a carefully crafted budget that prioritizes essential expenses, can help families regain control over their financial decisions and rebuild the foundation for long-term stability.

(Read – Credit Card Delinquencies: Defaults Soar Across Income Groups)

The Shift from Savings to Debt-Based Living in India

Most of us today face a reality that would have surprised our parents: borrowing money for groceries, school fees, and basic utilities has become routine. The household debt surge has fundamentally altered how we approach daily expenses, transforming necessities into financed purchases that stretch family budgets beyond recognition. What once required careful saving now happens with a quick swipe of a credit card or a digital loan approval.

Consider an individual who seemed to have everything under control. He managed a car loan, a modest personal loan for furniture, and used credit cards responsibly, always paying them off each month. His financial structure appeared solid until his company downsized and he faced four months of unemployment. Unable to make full payments, he started paying minimums, then borrowing from one card to pay another. By the time he secured new employment at 20% lower pay, his manageable ₹15,000 monthly obligations had ballooned to ₹35,000 due to penalties and compounding interest.

Credit Card Usage Growth Accelerates Debt Problems

This pattern repeats across millions of households where temporary income disruptions reveal how precarious debt-financed living actually is. We often find ourselves in situations where carefully balanced financial equations collapse when even one variable changes. A medical emergency, job loss, or unexpected expense can transform manageable payments into an overwhelming cycle that takes years to resolve.

The shift from savings-based to debt-based consumption creates a psychological trap where borrowing feels easier than the discipline of waiting and saving. We convince ourselves that taking a loan for a child’s coaching classes or financing a family celebration makes sense because the payments seem small. However, these decisions accumulate into a lifestyle where we are perpetually paying for past consumption while struggling to afford present needs.

Breaking this cycle requires more than just financial strategies – it demands a fundamental shift in how we perceive and use credit. Understanding the true cost of debt-financed consumption, including interest payments and opportunity costs, helps families make more informed decisions about when borrowing serves their long-term interests versus when it merely postpones difficult financial realities.

Practical Debt Elimination Strategies for Indian Households

Most of us facing the household debt surge need a systematic approach that addresses both the mathematical reality of debt and the behavioral patterns that created it. The debt avalanche method provides the most cost-effective path forward by targeting high-interest obligations first while maintaining minimum payments on all other debts. List every debt with its interest rate, minimum payment, and current balance, then create a bare-bones budget that cuts all non-essential expenses to maximize the amount available for debt elimination.

Most of us find success by paying minimums on all debts while directing every extra rupee toward the highest interest rate obligation. This approach saves thousands in interest payments compared to paying debts equally or focusing on smallest balances first. Consider debt consolidation only if it genuinely reduces your overall interest rates, not just to lower monthly payments by extending the repayment period. Negotiate with creditors for lower interest rates or modified payment plans, especially if you have been a consistent payer facing temporary hardship.

Understanding Your Debt Service Ratio Risk Zone

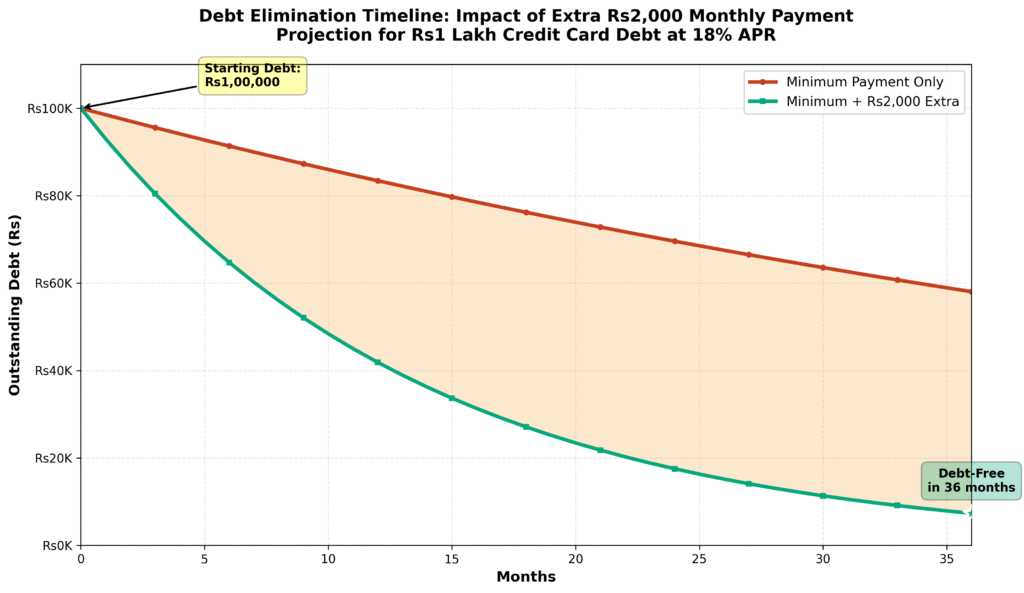

Credit card debt elimination requires immediate behavioral changes alongside the mathematical strategy. Cut up all credit cards except one designated for true emergencies, and transfer balances to the lowest interest rate card if this reduces costs. Pay the minimum plus an additional ₹2,000 monthly on your highest interest card while using only debit cards or cash for new purchases. Set up automatic payments to avoid late fees that can quickly derail progress and damage your credit score further.

Supporting these debt elimination efforts requires better control over daily spending habits. The envelope method transforms spending from abstract digital transactions into tangible cash decisions. Allocate specific cash amounts for groceries, utilities, and other essentials at the beginning of each month, and when the envelope is empty, spending in that category stops. This physical limitation prevents the unconscious overspending that digital payments enable and creates immediate awareness of spending patterns that may have been invisible before.

Debt Elimination Timeline with Extra Payments

Emergency fund building must happen simultaneously with debt elimination, even if progress feels slow. Start with saving ₹500 to ₹1,000 monthly in a separate account dedicated solely to unexpected expenses. This fund prevents new debt accumulation when life presents its inevitable surprises like medical bills or vehicle repairs. Build this emergency buffer to ₹10,000 before focusing resources on other financial goals, as this foundation prevents temporary setbacks from creating permanent financial damage.

Expected outcomes become realistic when we commit to these structured approaches consistently. Credit card debt elimination typically improves credit scores by 100 points or more within two to four years, while systematic debt reduction can decrease total obligations by 20 to 30 percent in the first year alone. The key lies not in perfection but in persistent application of these proven strategies until they become automatic habits that support long-term financial stability.

Moving Forward: Taking Control of Your Financial Future

Many families face increasing household debt burdens, but we have control over the path forward. The statistics show an increase in average family debt to ₹4.8 lakh and household obligations now representing 42% of our GDP. These numbers highlight the potential for financial improvement when we take systematic action.

Starting today requires nothing more than choosing one debt elimination strategy and committing to it for thirty days. Whether we select the debt snowball method to build momentum or the avalanche approach to minimize interest costs, the power lies in beginning immediately rather than waiting for perfect conditions that never arrive. Consider using a debt tracking app to list our obligations in order of priority, and aim to make an extra payment toward your chosen target debt this week.

Small daily decisions compound into remarkable long-term results when we maintain consistency over months and years. Redirecting just ₹200 daily from unnecessary purchases toward debt reduction creates ₹6,000 monthly in extra payments, potentially eliminating credit card balances two to three years faster than minimum payments alone. The emergency fund we build simultaneously protects these gains from being erased by unexpected expenses that might otherwise force new borrowing.

Our financial future improves when we recognize that the current household debt surge represents a temporary challenge rather than a permanent condition. Families across India are successfully implementing these debt elimination strategies and rebuilding their financial foundations despite starting from difficult circumstances. The tools, knowledge, and resources exist today for us to begin the journey toward debt freedom and long-term financial security.

We can take action now by selecting our first debt target and making an extra payment this week. Starting today rather than postponing change until tomorrow creates momentum that builds over time. Household Debt to GDP India patterns can shift when individual families like ours commit to systematic debt reduction and consistent financial discipline.

FAQs

Q: How do I know if my debt level is manageable or problematic? Calculate your total monthly debt payments (including minimum credit card payments) as a percentage of your take-home income. If this exceeds 30%, you’re likely overextended and should prioritize debt reduction over new purchases.

Q: Is it normal for Indian families to have this much debt now? While debt levels have increased significantly, normal doesn’t mean healthy. Many families are financing basic expenses that previous generations paid for with cash, creating long-term financial vulnerability despite short-term convenience.

Q: What should I do if I’m already using credit cards for groceries regularly? Start by tracking exactly what you’re charging monthly, then create a plan to gradually reduce these purchases while building a small cash buffer for essentials.

External Sources

- Reserve Bank of India – Household Finance Statistics

- National Sample Survey Office – Household Debt and Investment Survey

- Credit Information Bureau India Limited – Credit Card Usage Trends Report 2024

- Ministry of Statistics and Programme Implementation – Household Consumer Expenditure Survey

About the Author: Chitransh Saxena

Chitransh Saxena is the Founder of MoneyHum and a behavioural finance specialist with over seven years of experience in global financial markets, psychology-driven money systems, and low-risk investing frameworks. His work blends data, decision science, and financial clarity to help readers build calm, reliable wealth habits.

Learn more at the full profile: moneyhum.com/about-us/

Disclaimer: This article is for educational and informational purposes only. It is not financial advice. Consult a licensed financial advisor for personalised recommendations.

Disclosure: While the core content and ideas are human, tools were utilised for research and editing.