Author’s Note

As I researched this piece, I kept thinking about that professional who started using her credit card for groceries during a salary delay. Her story could be any of ours. The ease with which we can now access credit has fundamentally changed how Indian families manage money, often without us realizing the long-term implications. When I saw that India’s household debt to GDP ratio has nearly doubled in less than a decade, it became clear that we’re facing a quiet crisis that deserves urgent attention. This isn’t about judging financial choices, but about understanding the landscape we’re navigating and making informed decisions. I hope this article helps you recognize the warning signs and take proactive steps to protect your family’s financial future.

Key Takeaways

- Track your debt-to-income ratio monthly and aim to keep total debt payments below 40% of your income

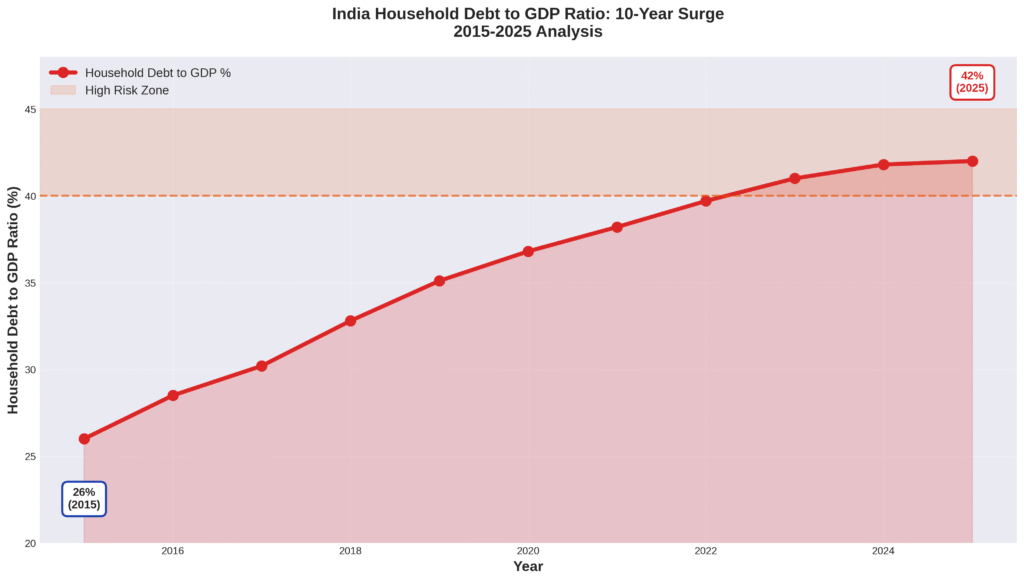

- India’s household debt to GDP ratio has surged from 26% in 2015 to 42% in 2025, signaling widespread financial stress

- Rising costs combined with stagnant per capita income growth are forcing families to bridge gaps through borrowing

- Create an emergency fund covering 6 months of expenses before relying on credit for unexpected situations

Many families find themselves relying on credit cards for everyday expenses when faced with financial delays. A professional started using her credit card for weekly groceries when her salary got delayed by a month. What began as a temporary solution became a habit. Soon she was swiping for vegetables, milk, even her daughter’s school stationery. Within six months, her minimum payments consumed 30% of her salary, and she realized she was paying 36% interest on tomatoes she had eaten months ago. The wake-up call came when she calculated that a ₹500 grocery bill, if only minimum payments were made, would actually cost her ₹1,200 over two years.

This story resonates with millions of Indian families today. We are living through a silent debt crisis that has crept into our homes without much fanfare or headlines. While we debate inflation and job markets, a more fundamental shift has been happening right under our noses. Indian households are borrowing at unprecedented levels to maintain their standard of living.

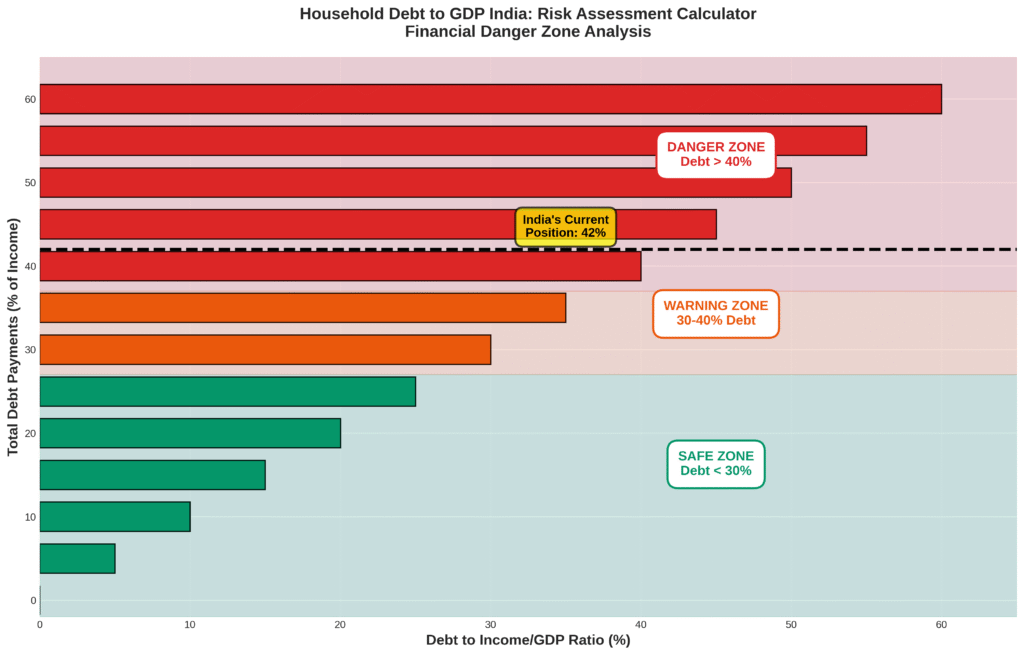

The numbers tell a sobering story. India’s household debt has surged from 26% of GDP in 2015 to a staggering 42% in 2025. This means that for every ₹100 the country produces, Indian families now owe ₹42, nearly double what they owed just ten years ago.

Most of us can relate to the pressures that drive these borrowing decisions. Rising education costs, medical emergencies, lifestyle aspirations, and sometimes just the need to bridge the gap between paydays. Credit has become easier to access than ever before, from instant personal loans approved through mobile apps to credit cards with generous limits. Yet this convenience masks a dangerous reality that many families discover too late.

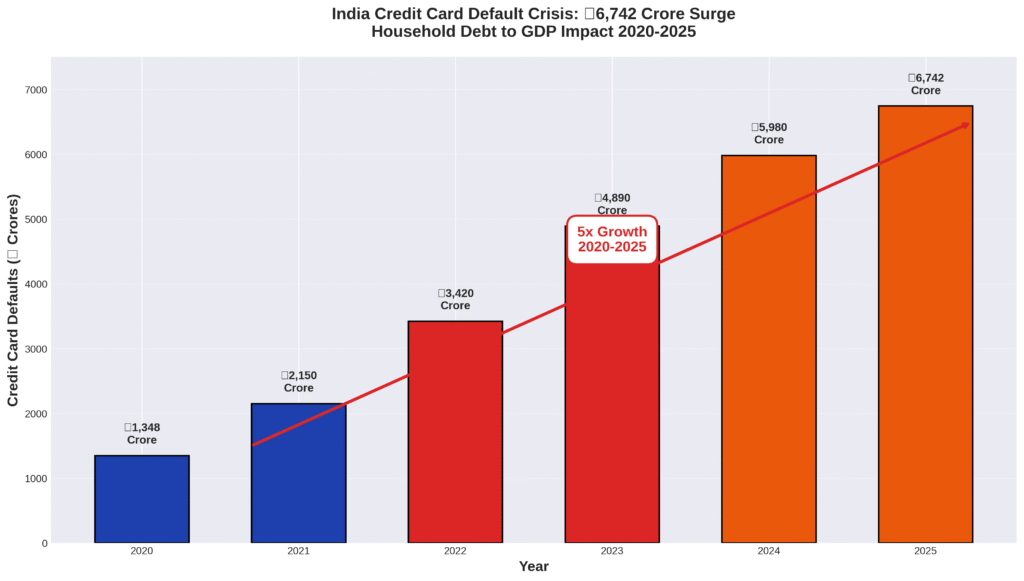

The scale of this crisis becomes clearer when we look at specific sectors. Credit card defaults alone have exploded to ₹6,742 crore, a mind-numbing 5 folds increase since 2020. The average household debt per person has jumped by ~23% in just two years. These are not just statistics. They represent real families struggling with debt burdens that often began with what seemed like reasonable financial decisions.

We need to understand what is driving this surge, recognize the warning signs in our own financial lives, and most importantly, learn how to navigate this landscape without falling into the debt traps that are claiming so many households across the country.

Understanding India’s Household Debt to GDP Crisis

When Basic Needs Become Debt Burdens

The most concerning trend in India’s household debt crisis is families borrowing money for basic necessities like groceries and school fees. When parents cannot afford to feed their children or pay school fees without taking loans, we have crossed from financial strain into genuine financial distress. The average family debt in India has reached ₹5 lakh, with a growing portion of this borrowed for essential expenses rather than luxuries or investments.

Middle and lower-income families with children face the harshest reality of this crisis. Parents describe feeling ashamed and anxious about their inability to provide basic necessities without borrowing. The psychological toll is immense when something as fundamental as buying groceries requires a credit card or personal loan. This creates a vicious cycle where families borrow for essentials, then struggle with EMI payments, leading to more borrowing just to stay afloat.

Consider an individual who proudly showed me his investment portfolio worth ₹8 lakhs, accumulated over four years of disciplined monthly investments. His confidence shattered when we examined his complete financial picture. He carried personal loans totaling ₹6 lakhs and credit card debt of ₹3 lakhs. Despite feeling wealthy from his growing mutual fund statements, he was actually ₹1 lakh in the red. He was surprised to learn that his loan EMIs cost him ₹18,000 monthly while his investments were only ₹12,000. He was essentially borrowing money at 15% interest to invest at potentially 12% returns.

Breaking free from this cycle requires immediate action on two fronts. First, families must create an emergency fund, even if it starts with just ₹500-1000 monthly saved in a separate account. Second, switching to cash-only budgeting for essentials helps break the borrowing habit. This means withdrawing the exact amount needed for groceries, utilities, and school fees each week and using only cash instead of cards. The psychological impact of spending physical money creates natural spending boundaries that digital payments often lack.

The path out takes time but delivers results. Most families can stop borrowing for basic necessities within three to six months using this approach. Building a meaningful emergency fund takes about a year, but the peace of mind that comes from knowing you can handle grocery bills and school fees without borrowing is invaluable. Parents report feeling significantly less stressed once they break free from the cycle of borrowing for essentials, even if their overall debt situation takes longer to resolve.

Why India’s Household Debt to GDP Ratio Keeps Rising

The Debt Acceleration Problem

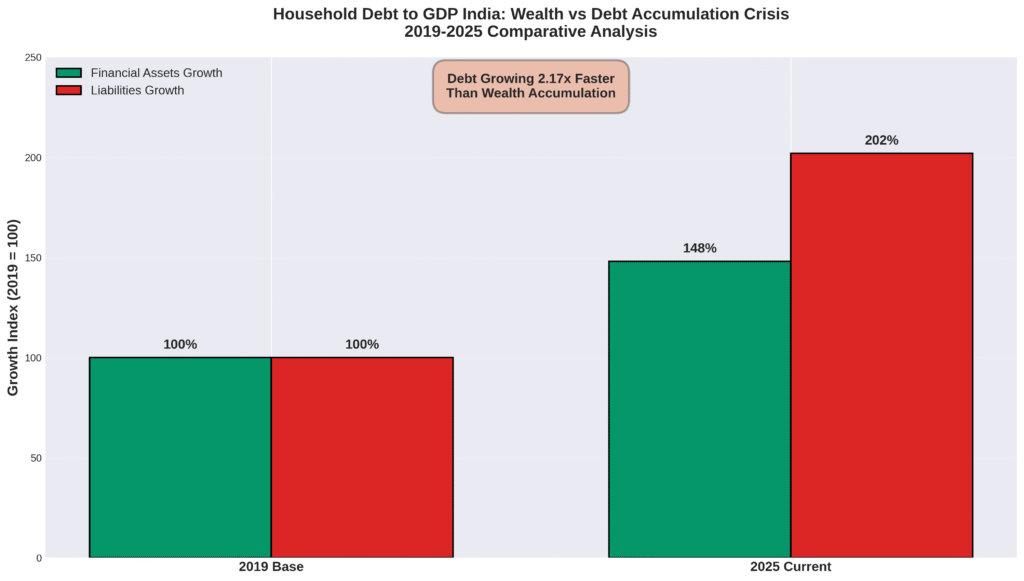

Most of us believe that as our income grows, our financial health automatically improves. The reality is different. Between 2019 and 2025, Indian households added financial assets worth 48% more than their starting point, yet their liabilities increased by 102%. This means we are accumulating debt more than twice as fast as we are building wealth, which could impact our financial stability over time.

This trend becomes clear when we look at individual stories that mirror what many of us experience. A small business owner took a personal loan for ₹2 lakhs to pay his son’s engineering college fees during COVID. The plan seemed reasonable, repay it within a year once things normalized. But then came his daughter’s school trip, his wife’s medical emergency, and the festival season expenses. All of these were funded by extending the same loan. Three years later, what started as education financing had morphed into a ₹4.5 lakh debt covering everything from medical bills to wedding gifts. This example shows how easily we can fall into the debt acceleration trap, where one loan becomes the solution for multiple financial needs.

This pattern repeats across income groups, but we middle-class households feel the squeeze most acutely. India’s household debt to GDP ratio has jumped from 26% in 2015 to 42% in March 2025. Credit card defaults alone have reached ₹6,500 crore, representing a 500-fold increase since 2020. These numbers reveal how we have become trapped in a cycle where every financial goal gets funded through borrowed money rather than saved money.

Understanding Your Personal Debt Danger Zone

The household debt to GDP ratio provides a macro view, but we need to understand what these numbers mean for individual families. Financial advisors use the debt-to-income ratio to assess household financial health. Calculate yours by adding all monthly debt payments and dividing by monthly income. If this number exceeds 40%, you have entered the danger zone where financial stress becomes severe and any unexpected expense could trigger a crisis.

Breaking Free from the Household Debt to GDP Trap

Practical Solutions for Indian Families

Most of us know what needs to be done but struggle with how to achieve it. The solution begins with creating an emergency fund and switching to cash-only budgeting for essentials. This breaks the borrowing cycle that traps us in debt for basic necessities like groceries and utility bills. Start by listing every essential monthly expense and calculating the exact amount needed. Then implement a weekly cash envelope system where you withdraw only the budgeted amount for essentials and leave your cards at home. This cash-only approach naturally leads to the next crucial step of building a financial cushion that prevents future borrowing.

Building this emergency cushion requires saving ₹500-1000 monthly in a separate savings account, even if it means cutting one non-essential expense. This may seem impossible when money feels tight, but most of us find we can redirect spending from subscription services, dining out, or unnecessary shopping. Contact your child’s school to discuss fee payment plans or explore scholarship opportunities if available. Within 3-6 months, this approach stops the borrowing cycle for basic needs and begins building financial breathing room.

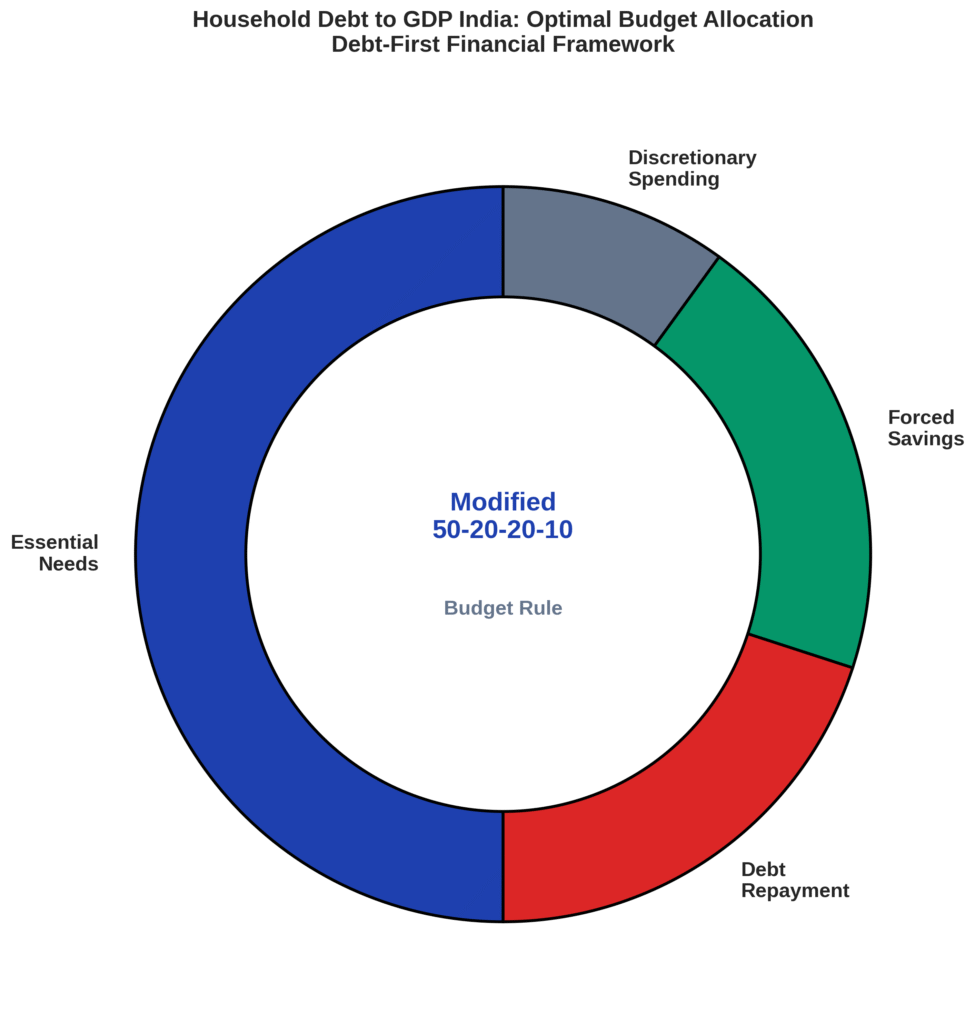

The Modified 50-20-20-10 Budget Rule for High Debt Households

The modified 50-30-20 rule transforms how we debt-heavy households allocate income while India’s household debt to GDP continues climbing toward 42.60%. Dedicate 50% for essential needs only, 20% specifically for debt repayment starting with highest interest rate debts, 20% for forced savings through automatic transfers, and limit discretionary spending to just 10%. This debt-first modification feels restrictive initially but addresses the root cause of wealth destruction rather than just managing symptoms.

Credit Card Debt Elimination Strategy

Credit card debt elimination requires the avalanche method combined with credit score protection. List all cards with outstanding balances, interest rates, and minimum payments. Pay minimum amounts on all cards, then direct every extra rupee toward the highest interest rate card. Contact your credit card companies to request lower interest rates or payment plans before missing payments. Set up automatic minimum payments to avoid late fees and further credit score damage. Once cleared, keep cards active with small monthly purchases like phone bills and pay in full to rebuild your credit history.

These solutions work when we implement them consistently over 12-24 months. We who follow this approach typically see our wealth-to-debt ratio improve within 18 months, with credit scores beginning recovery in just 6 months. The key lies in treating debt repayment as automatically as we treat essential bills, non-negotiable and systematic. This disciplined approach reverses the dangerous trend of building debt faster than building wealth, creating the foundation for genuine financial security.

Moving Forward: Your Action Plan Against Rising Household Debt to GDP

Many families find that their journey toward debt freedom starts with a single decision today. The numbers show that household debt to GDP continues to climb, but they also reveal something powerful: every percentage point of debt we eliminate creates breathing room for wealth building. Most families who commit to the debt-first budget modification see measurable progress within 90 days, with the psychological boost of clearing that first credit card providing momentum for the entire process.

Take inventory of your complete financial picture this week. List every debt with its interest rate and minimum payment, calculate your true monthly income after taxes, and identify which expenses serve your goals versus which drain your resources. This clarity alone shifts us from reactive spending to intentional wealth building. Set up automatic transfers for debt payments and savings before discretionary spending has a chance to consume those funds.

Understanding where we stand financially reveals why timing matters so much with debt elimination. Debt reduction can mirror the benefits of compounding investments. Every month we delay action, interest charges multiply our burden while inflation erodes our purchasing power. Conversely, every extra payment toward high-interest debt creates immediate guaranteed returns that few investments can match. A credit card charging 24% annual interest means every rupee of extra payment delivers an instant 24% return on that money.

Your financial future depends more on consistent small actions than perfect strategies. Start with the 50-20-20-10 budget framework this month, focus on eliminating one credit card completely, and build the habit of reviewing your progress weekly. These practices, maintained over 12-18 months, create the foundation for genuine wealth accumulation rather than the illusion of prosperity built on borrowed money.

The path from debt burden to financial security exists for every household willing to prioritize long-term wealth over short-term comfort. We have the tools, the framework, and the knowledge needed to reverse the trend of household debt to GDP growth. Your commitment to starting today, with whatever amount you can dedicate to debt elimination, begins the transformation from financial stress to financial strength that defines true prosperity.

FAQs About Household Debt to GDP India

Q: How do I know if my family’s debt level is dangerous?

If your total monthly debt payments exceed 40% of your income, you’re in the danger zone. Also watch for signs like making only minimum payments, borrowing to pay other debts, or using credit for basic necessities regularly.

Q: Why are Indian households borrowing so much more now?

Easy credit access through apps and cards, rising costs of education and healthcare, lifestyle inflation, and income delays are key factors. Credit has become the go-to solution for bridging financial gaps that were previously managed through savings.

Q: What should I do if I’m already trapped in high-interest debt?

List all debts by interest rate and focus on paying off the highest-rate debt first. Consider debt consolidation options, negotiate with lenders for better terms, and create a strict budget that prioritizes debt repayment over discretionary spending.

External Sources

- Reserve Bank of India Household Financial Savings Data

- Reserve Bank of India Financial Stability Reports

- Reserve Bank of India Database on Indian Economy

About the Author:

Chitransh Saxena is the Founder of MoneyHum and a behavioural finance specialist with over seven years of experience in global financial markets, psychology-driven money systems, and low-risk investing frameworks. His work blends data, decision science, and financial clarity to help readers build calm, reliable wealth habits.

Learn more at the full profile: moneyhum.com/about-us/

Disclaimer: This article is for educational and informational purposes only. It is not financial advice. Consult a licensed financial advisor for personalised recommendations.

Disclosure: While the core content and ideas are human, tools were utilised for research and editing.