Author’s Note

As someone who has analyzed hundreds of family financial situations, I’ve witnessed the subtle shift happening in Indian households. The marketing professional’s story isn’t unique – I see similar patterns across income brackets. What strikes me most is how gradually debt accumulates, often while we feel financially secure. The rise in household debt to GDP from 35% to over 42% represents millions of families making incremental decisions that compound over time. This article examines not just the numbers, but the human stories behind them. My hope is that by understanding these patterns, we can make more informed choices about our financial futures and recognize warning signs before they become overwhelming burdens.

Key Takeaways

- Track your total debt across all sources monthly, not just individual account balances, to see the complete picture of your financial obligations

- Monitor how household debt to GDP trends affect lending rates and credit availability, as these macro indicators influence your borrowing costs and options

- Calculate your debt-to-income ratio against per capita income growth to ensure your borrowing remains sustainable as economic conditions change

- Create a debt elimination priority list, focusing on high-interest credit cards first while maintaining minimum payments on all accounts

A marketing professional started with one credit card for emergencies in 2022. By late 2024, she was juggling four cards, using one to pay the minimum on another. What began as a ₹15,000 shopping spree for festival clothes had snowballed into ₹2.8 lakh of revolving debt across multiple cards. She was paying ₹18,000 monthly just in minimum payments, barely touching the principal, while her salary remained the same. Every swipe felt justified until the bills became bigger than her rent.

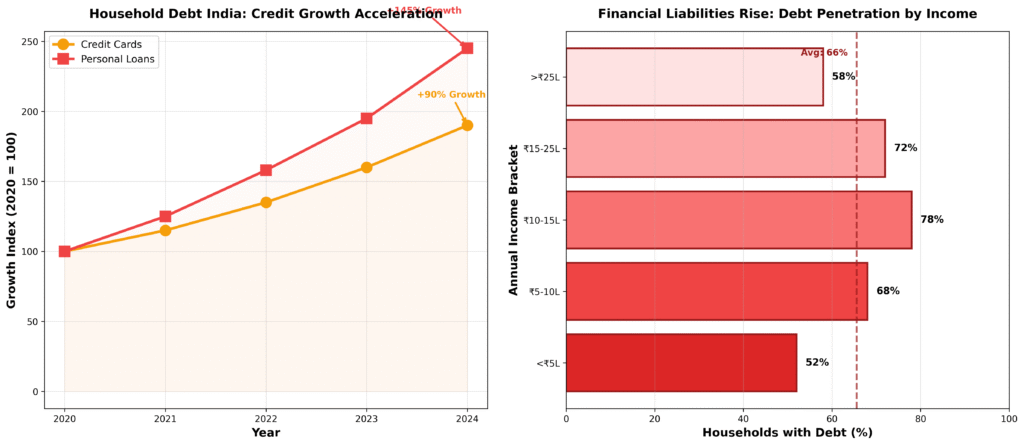

Her story reflects a broader pattern we are witnessing across families in India. Credit cards amplify spending habits, both good and bad. The 50% surge in credit card usage since 2022 is not just numbers; it represents millions making the same seemingly small decisions that compound dangerously over time.

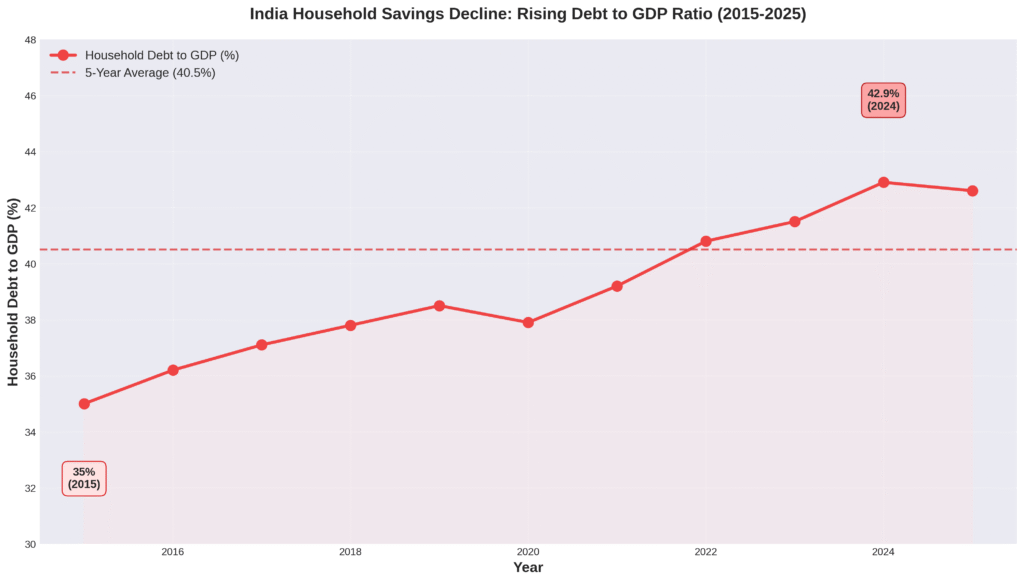

Most of us think debt problems happen to others. We convince ourselves that our borrowing is different, strategic, temporary. Yet household debt levels tell a different story. India’s household debt to GDP has climbed from 35% in 2015 to over 42% by the end of 2024, according to the Reserve Bank of India. This puts us above the five-year average and on track to reach 42.60% in the second quarter of 2025.

Behind these statistics lie real families stretching their finances thinner each month. Home loans that seemed manageable when interest rates were lower now consume larger portions of monthly budgets. Personal loans bridge gaps that keep widening. Credit card balances roll over month after month, accumulating interest that exceeds what many earn on our investments.

We are living through a quiet financial shift that deserves our attention. Understanding how household debt to GDP affects our daily financial decisions can help us navigate these changing times more wisely. The numbers matter because they represent the collective financial health of families like ours, and the choices we make today will shape our financial security tomorrow.

Understanding India’s Household Savings Decline and Rising Debt Crisis

Consider how deceptive wealth can feel in today’s investment-driven culture. A software engineer proudly showed me his investment app displaying ₹4.2 lakh in mutual funds – his disciplined SIP contributions over three years. What he did not mention until later was the ₹6.8 lakh personal loan he had taken for his sister’s wedding and the ₹2.1 lakh he owed on his bike and credit cards. Despite feeling wealthy watching his portfolio grow, his net worth was actually negative ₹4.7 lakh. The satisfaction of growing investments had blinded him to the bigger picture.

This story reflects a troubling reality we face across Indian households today. We are creating financial assets faster than ever, but debt is growing even faster. Wealth is not just what we own – it is what we own minus what we owe. Yet most of us focus only on the assets side of this equation, celebrating investment milestones while debt quietly accumulates in the background.

Net Financial Savings at Historic Lows

The numbers paint a stark picture of this imbalance. India’s household debt to GDP has climbed to 42.9% by the end of 2024, up from 35% in 2015. This places us above the five-year average and represents the highest debt relative to our income capacity. With per capita income at just ₹1,85,854 annually, we are borrowing at unprecedented levels compared to what we actually earn. The financial literacy gap compounds this problem, as many of us lack the knowledge to assess our true debt capacity.

Most concerning is how this debt burden affects those of us with limited income buffers. Middle and lower-middle class households are stretching our finances dangerously thin, with total debt payments consuming ever-larger portions of monthly budgets. Home loans that seemed manageable when interest rates were lower now strain our finances. Personal loans fill gaps that keep widening. Credit card balances roll over month after month, accumulating interest that often exceeds our investment returns.

The Emotional Toll of Household Debt India

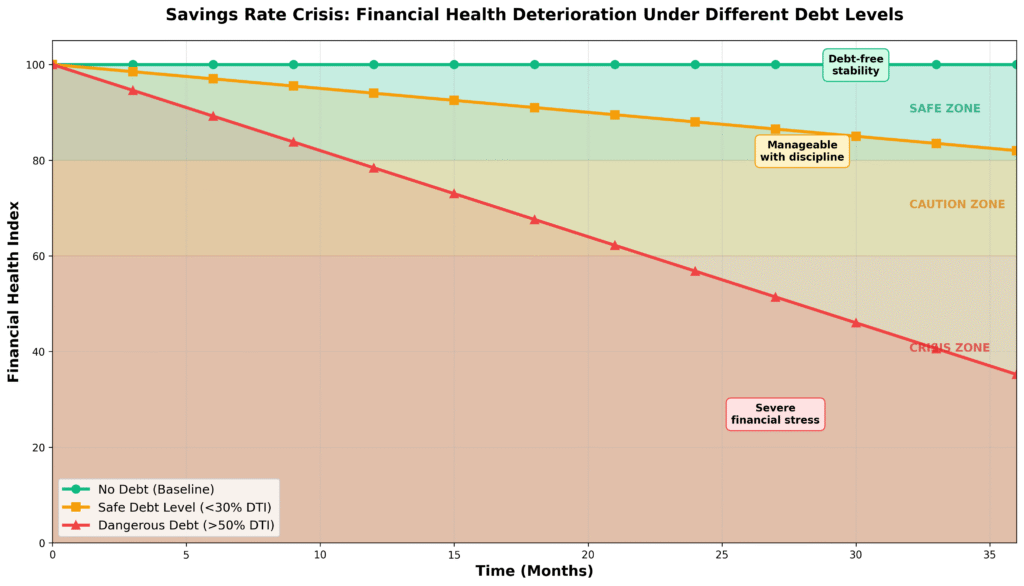

The emotional toll runs deeper than the financial calculations. We report growing anxiety about meeting debt obligations, fear about financial security, and stress from the constant pressure of multiple EMIs. What starts as optimism about building assets gradually transforms into worry about sustaining debt payments, especially during income disruptions or emergencies.

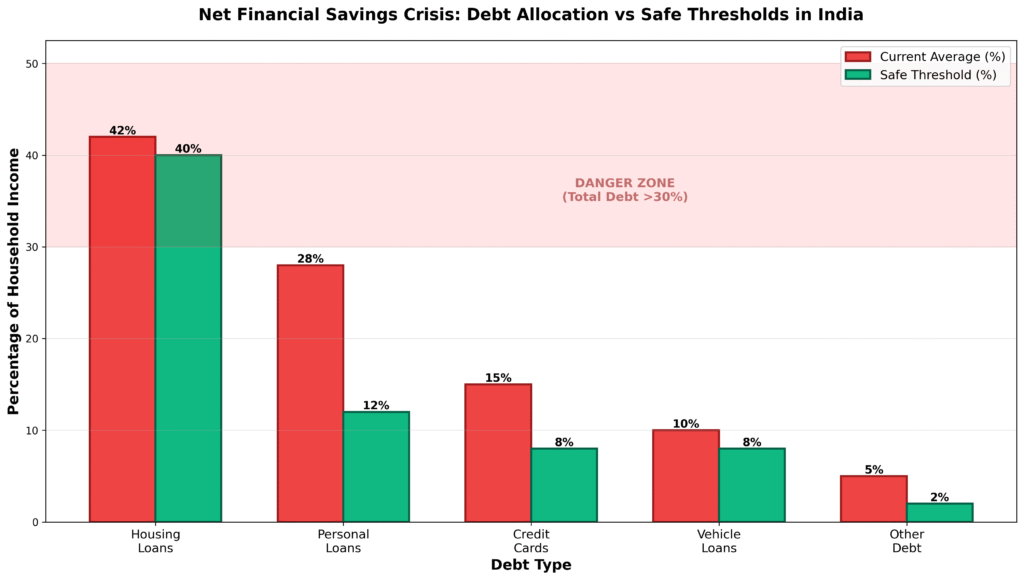

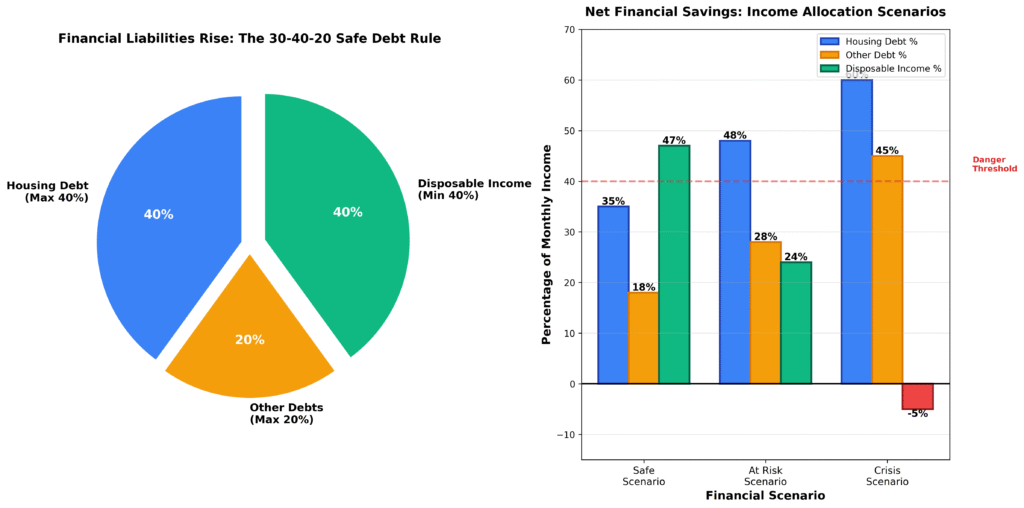

This debt trap operates quietly but powerfully. We feel wealthy watching our investment portfolios grow, unaware that our net worth is actually declining. The solution requires implementing strict debt safety rules: never let total debt payments exceed 30% of gross income, with housing at 40% maximum and other debts at 20% maximum. Calculating your current debt-to-income ratio and creating a systematic reduction plan can prevent the dangerous overleveraging that threatens our financial security today.

How Easy Credit Accelerates the Savings Rate Crisis

Most of us have experienced the flood of pre-approved loan offers arriving through every digital channel imaginable. A software engineer recently shared how he received loan offers worth ₹12 lakh within a single week – via SMS, WhatsApp, and email notifications promising money in his account within two hours, no paperwork required. When his family faced a medical emergency, he grabbed ₹3 lakh from a fintech app at 24% annual interest, convinced he would repay it quickly. Eight months later, after paying ₹1.8 lakh in EMIs, he still owed ₹2.4 lakh on the original loan.

This story illustrates how household debt to GDP has accelerated rapidly, jumping from 35% in 2015 to 45% in 2024 – a 10 percentage point surge in just nine years. The convenience of instant credit masks the dangerous reality of accumulating debt obligations that compound faster than most of us anticipate. Digital lending platforms make borrowing feel effortless, but the repayment burden grows heavier with each passing month.

Financial Liabilities Rise Across All Income Groups

The acceleration stems from multiple converging factors. Easy loan approvals bypass traditional risk assessments, allowing us to accumulate debt across multiple platforms simultaneously. Many of us discover we have taken loans from three or four different apps before realizing the cumulative impact on our monthly cash flow. The low savings rate among Indian households means we lack adequate buffers to handle these overlapping debt obligations, creating a perfect storm for financial distress.

Breaking this cycle requires establishing a personal borrowing policy with strict criteria before taking any new debt. Create a written checklist that asks three critical questions: Is this for an appreciating asset? Can I afford twice the EMI amount? Do I have six months of payments saved as a buffer? Implement a mandatory 48-hour cooling period before applying for any loan, allowing emotions to settle and rational analysis to prevail.

Setting Annual Debt Limits to Combat Household Savings Decline

Set annual debt limits that prevent total borrowing from increasing by more than 10% of your annual income in any given year. This simple rule acts as a circuit breaker against the temptation of easy credit. Review and update your borrowing policy every six months, adjusting limits based on income changes and existing debt obligations. These safeguards may seem restrictive initially, but they prevent the debt spiral that traps so many households in unsustainable financial commitments.

The goal is not to eliminate all debt, but to maintain control over our borrowing decisions. When credit flows too easily, we forget that borrowed money still needs to be repaid with interest. A systematic approach to debt decisions helps distinguish between productive borrowing that builds wealth and impulsive borrowing that erodes our financial foundation over time.

Strategic Solutions to Reverse Net Financial Savings Decline

Most of us know the feeling of watching our monthly commitments creep higher while our income stays relatively flat. With household debt to GDP reaching high levels in India, the time for reactive financial management has passed. We need proactive solutions that address the root causes of our borrowing patterns, not just the symptoms.

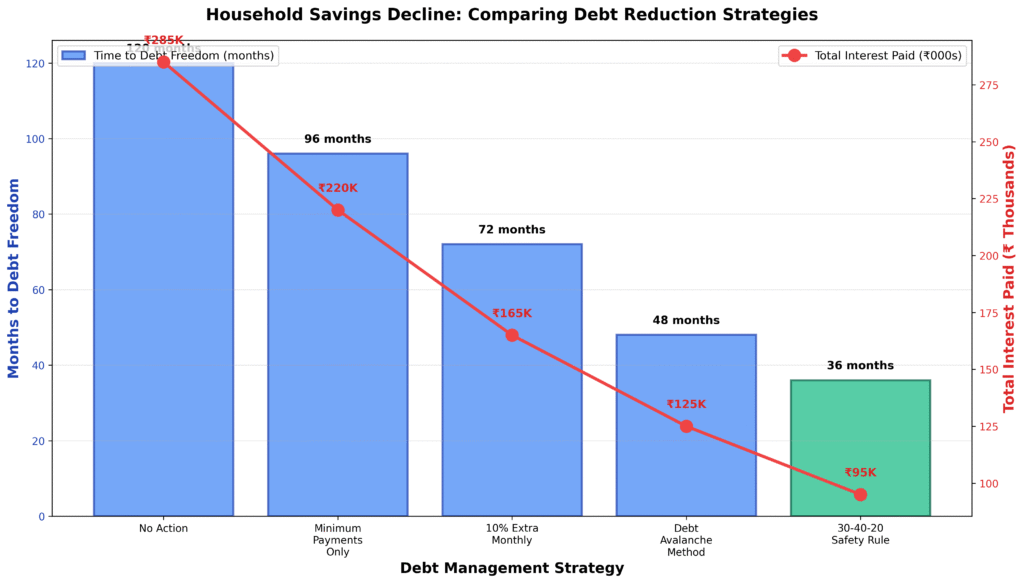

Implementing the 30-40-20 Debt Safety Rule

A foundational strategy in debt control is implementing the 30-40-20 debt safety rule. Our total debt payments should never exceed 30% of our gross monthly income, with housing costs capped at 40% and all other debts limited to 20%. We need to calculate our current debt-to-income ratio by adding all monthly debt payments and dividing by our gross monthly income. If we are above the 30% threshold, we must create an aggressive debt reduction plan targeting our highest interest rate obligations first.

We should set up automatic transfers to a separate debt payment account to ensure consistency in our repayment schedule. This prevents the temptation to skip payments when other expenses arise. When salary increments or bonuses come our way, we must resist the urge to upgrade our lifestyle immediately. We should channel these windfalls directly toward debt reduction, accelerating our path to financial freedom.

Breaking the Consumption Debt Cycle

Breaking the consumption debt cycle requires us to replace high-cost borrowing with strategic cash flow management. We need to list all our credit cards and personal loans along with their interest rates, then systematically eliminate the most expensive debt first. We should convert to debit card or cash-only spending for six months to break the psychological habit of treating credit as available money. This period of financial discipline helps us rewire spending behaviors that contribute to credit card delinquencies across all income groups.

We can create a dedicated consumption fund by saving ₹5,000 to ₹10,000 monthly in a liquid mutual fund. This becomes our source for discretionary purchases, eliminating the need for credit card financing. When we encounter 0% EMI offers, we should use them only for essential purchases and only when we have the full amount already saved and earmarked for that expense.

Timeline for Financial Transformation

The transformation from debt-dependent to debt-controlled living typically takes us 6 to 18 months, depending on our starting position. The effort we invest in establishing these systems pays compound dividends over time. As our debt burden lightens, we will find more money available for wealth-building activities like investments and asset accumulation, creating a positive financial cycle that builds long-term prosperity.

Building Financial Resilience Despite Household Debt India Trends

Rising household debt to GDP levels in India signal an urgent need for individual action, but the path forward remains entirely within our control. Each of us can begin today by taking one simple step toward financial discipline. We might start by tracking our expenses for just one week, or by setting up an automatic transfer of ₹2,000 to a separate savings account. These small actions create momentum that builds into lasting financial transformation.

The data shows us where we stand collectively, but our individual journey starts with personal commitment. We can download a budgeting app tonight, call our bank tomorrow to understand our exact debt obligations, or simply write down three financial goals we want to achieve this year. The key lies not in the perfection of our initial steps, but in the consistency of taking them. Every rupee we redirect from consumption debt to emergency fund building strengthens our financial foundation.

From Reactive Spending to Proactive Planning

Achieving financial freedom involves shifting from reactive spending to proactive planning. We can establish simple systems like the 50-30-20 rule for income allocation, or commit to reviewing our credit card statements weekly instead of monthly. These practices help us catch debt accumulation early and adjust our spending patterns before problems compound. The families who successfully navigate rising debt levels are those who treat financial management as a regular habit, not an occasional activity. By integrating these practices into our routine, we lay the groundwork for long-term financial health.

These consistent habits create something powerful: financial discipline that compounds over time, just like debt does in reverse. When we consistently choose delayed gratification over immediate consumption, we create space for wealth building and genuine financial security. The current household debt to GDP trends in India represent a challenge, but they also present an opportunity for those willing to act differently from the crowd.

Your financial future depends on the decisions you make starting today. The tools, strategies, and knowledge exist to build lasting financial stability regardless of broader economic trends. Take the first step now, stay consistent with your efforts, and trust that small daily choices create extraordinary long-term results. Financial freedom awaits those who choose to pursue it systematically and patiently.

FAQs

Q: How does rising household debt to GDP affect my personal borrowing capacity? When household debt to GDP rises significantly, banks typically tighten lending criteria and may increase interest rates. This means you might face stricter income verification, higher EMIs, or reduced loan amounts for future borrowing needs.

Q: Should I be concerned if my debt is growing faster than my income? Yes, this is a red flag. If your debt growth consistently outpaces income growth, you’re essentially becoming poorer over time. Focus on eliminating high-interest debt first and avoid taking new loans until this ratio improves.

Q: What if interest rates continue rising on my existing variable-rate loans? Consider refinancing to fixed rates if you expect further hikes, or create a buffer fund specifically for EMI increases. Calculate how much extra you’d pay if rates rise by 1-2% and plan accordingly.

External Sources

About the Author: Chitransh Saxena

Chitransh Saxena is the Founder of MoneyHum and a behavioural finance specialist with over seven years of experience in global financial markets, psychology-driven money systems, and low-risk investing frameworks. His work blends data, decision science, and financial clarity to help readers build calm, reliable wealth habits.

Learn more at the full profile: moneyhum.com/about-us/

Disclaimer: This article is for educational and informational purposes only. It is not financial advice. Consult a licensed financial advisor for personalised recommendations.

Disclosure: While the core content and ideas are human, tools were utilised for research and editing.