Author’s Note

As I researched this piece, I kept thinking about that marketing professional and her grandmother’s jewelry. Her story isn’t unique – it’s playing out in millions of households across India. What struck me most while analyzing the data was how quickly we’ve normalized borrowing for everyday expenses. The household debt to GDP ratio tells a stark story, but behind every percentage point are real families making difficult choices. I’ve seen friends and colleagues caught in similar cycles, where what starts as a temporary financial bridge becomes a permanent burden. Writing this felt personal because it reflects conversations I’ve had with so many people who never expected to find themselves in debt spirals. We need to have honest discussions about money, not just celebrate consumption.

Key Takeaways

- Monitor your debt-to-income ratio monthly and set up automatic alerts when credit utilization exceeds 30% to prevent debt accumulation from spiraling out of control.

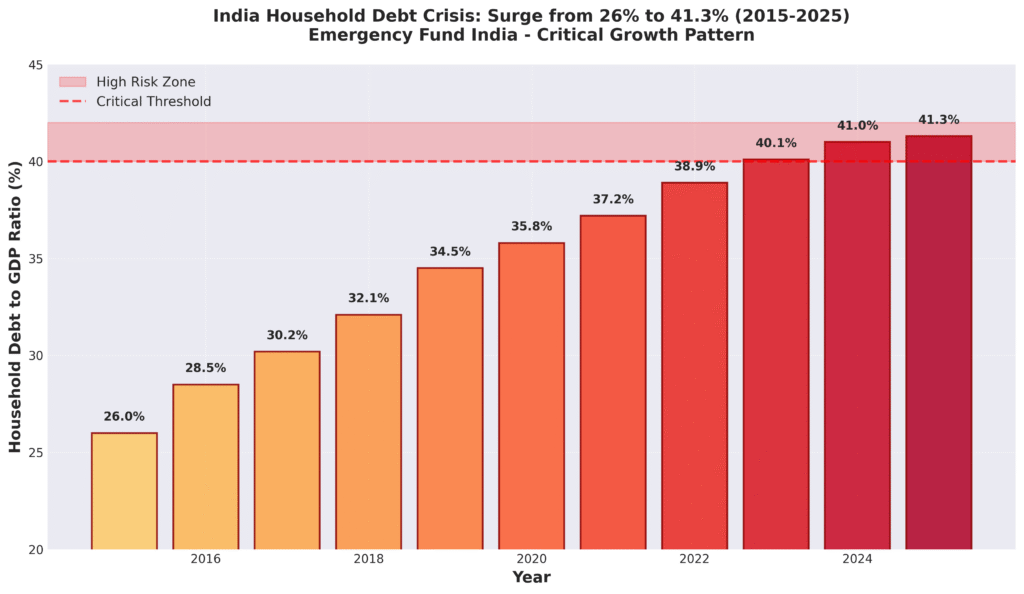

- The household debt to GDP ratio has surged from 26% to 41.3% in nine years, indicating that Indian families are borrowing at an unprecedented pace that outstrips economic growth.

- Rising debt levels combined with stagnant per capita income growth means families have less real purchasing power while carrying heavier financial burdens than previous generations.

- Create an emergency fund covering 6-8 months of expenses before taking any non-essential loans to avoid using family assets as collateral during financial stress.

Most of us have witnessed a moment when financial desperation transforms family treasures into mere collateral. A marketing professional in an Indian city had always treasured the gold jewelry her grandmother passed down – delicate earrings, a traditional necklace, and bangles that held decades of family memories. When her daughter’s school fees doubled and her husband’s salary got delayed for three months, she found herself at a gold loan counter, hesitantly placing these precious heirlooms as collateral for ₹2.5 lakhs. What started as a temporary solution became a recurring pattern – every few months, she would renew the loan, paying only the interest, unable to break free from the cycle.

Her story reflects a troubling reality spreading across Indian families. We are living through an unprecedented borrowing surge that has pushed household debt from 26% of GDP in 2015 to a significant 41.3% as of March 2025, according to the Reserve Bank of India. This substantial increase means that for every rupee our economy produces, more than 40 paise now represents what Indian families owe to lenders.

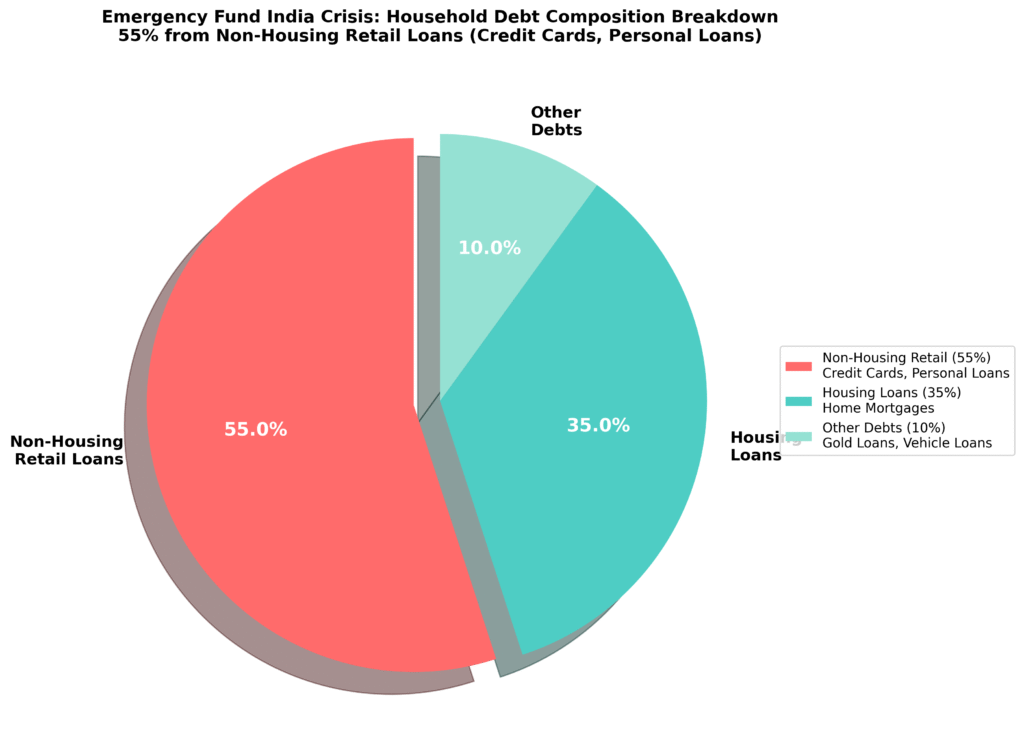

Behind these numbers lies a fundamental shift in how we manage money. The data reveals that 55% of household debt stems from non-housing retail loans – credit cards, personal loans, and consumer financing that promise instant gratification but deliver long-term financial strain. We have moved from borrowing for assets that appreciate to borrowing for consumption that disappears.

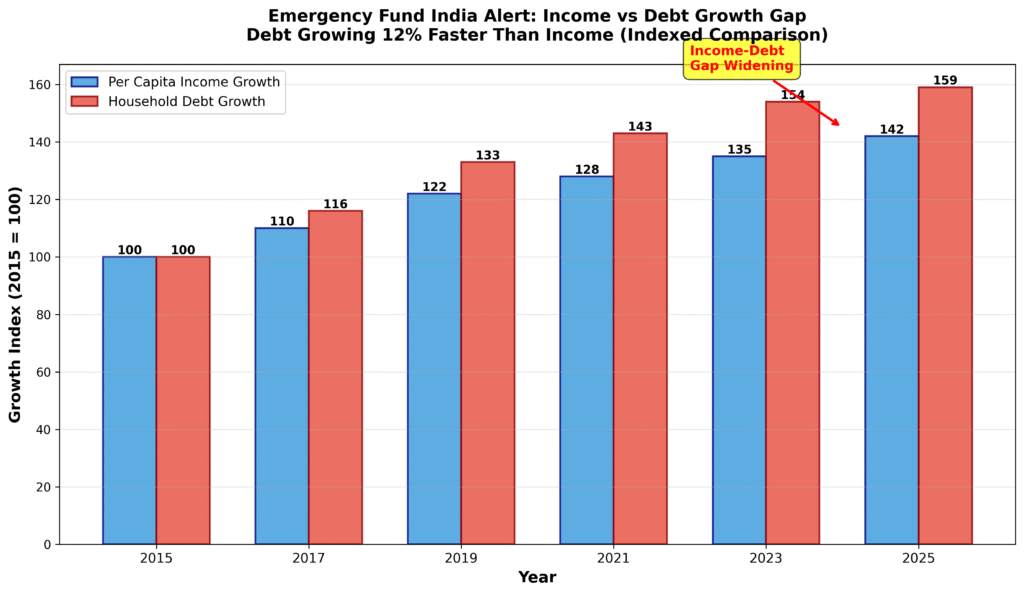

This shift in borrowing behavior has accelerated the growth of debt at an unprecedented pace. What makes this household debt to GDP ratio particularly concerning is the speed of its increase. In just nine years, Indian families have added debt equivalent to 15% of the entire nation’s economic output. This acceleration coincides with rising aspirations, stagnant real incomes, and the proliferation of easy credit options that make borrowing as simple as downloading an app.

The implications extend far beyond individual balance sheets. When families struggle under debt burdens, they reduce spending on education, healthcare, and investments that drive long-term prosperity. We risk creating a generation that inherits financial stress rather than financial security, where gold chains become emergency funds and family heirlooms transform into temporary cash flow solutions.

Understanding this crisis requires us to look beyond the statistics and examine the human stories behind each percentage point. Every uptick in the debt ratio represents thousands of families making difficult choices, trading future financial freedom for present-day survival or lifestyle maintenance.

Understanding the Emergency Fund India Crisis: Rising Household Debt

The Household Debt Trap Swallowing Indian Families

Most of us remember the days when our parents saved for months before making a major purchase. Today, that discipline has been replaced by the seductive promise of instant gratification through easy credit. The numbers paint a stark picture: household debt to GDP has jumped from 26% in 2015 to over 41% by 2024, representing one of the fastest debt accumulations in recent Indian economic history. This surge reflects a fundamental shift in how we approach money management, where borrowing has become the default solution for bridging the gap between aspirations and income.

The most significant aspect of this debt explosion lies in its composition. Unlike previous generations who borrowed primarily for productive assets like homes or business ventures, today’s borrowers are funding consumption through retail loans, credit cards, and personal financing. A young IT professional in an urban area exemplifies this trend perfectly. He started with one credit card for emergencies in 2022, but soon found himself juggling five different cards, using cash advances from one to pay minimums on another. What began as ₹50,000 in convenient purchases has ballooned to ₹3.2 lakhs in total debt, with monthly EMI payments consuming 70% of his salary. He later admitted during our consultation that he initially believed he was being smart by earning reward points and building credit history, only to realize he had constructed a financial prison instead.

Financial Safety Net Breakdown: Debt Composition Analysis

This pattern of credit card debt accumulation has become disturbingly common across urban India. The Reserve Bank of India data reveals that 55% of household debt now comes from non-housing retail loans, marking a dangerous departure from asset-backed borrowing. Families are increasingly using credit to maintain lifestyles rather than build wealth, creating a vicious cycle where debt grows faster than assets.

The convenience of digital lending platforms and instant approval processes has made borrowing so frictionless that many households accumulate multiple loan obligations without fully understanding the compound effect on their financial health. The financial implications of this borrowing behavior extend deeply into personal lives, affecting more than just bank balances.

Household Savings Crisis: The Human Cost of Debt

The human cost of this debt spiral extends far beyond monthly EMI calculations. Families under severe debt stress often sacrifice essential investments in education, healthcare, and emergency funds to service their loan obligations. We are witnessing a generation that inherits financial anxiety rather than financial security, where family gold becomes emergency liquidity and future earnings are already mortgaged to present consumption. The psychological burden manifests as constant worry about making payments, damaged relationships due to financial stress, and a persistent feeling of running on a financial treadmill without making progress.

What makes this household debt crisis particularly concerning is its acceleration during a period of relatively modest income growth. While per capita income increased from ₹2,353 to ₹2,481 between 2022 and 2023, debt accumulation has far outpaced this growth. This mismatch suggests that families are not borrowing from a position of strength but rather from financial desperation or lifestyle pressure.

The result is a national balance sheet where household liabilities are growing faster than household assets, effectively destroying wealth at the family level while appearing as economic growth in aggregate statistics.

The path forward requires acknowledging that our current borrowing patterns are unsustainable and implementing systematic changes to prioritize asset building over debt accumulation. The solution lies not in eliminating debt entirely, but in ensuring that every rupee borrowed either appreciates in value or generates income that exceeds the cost of borrowing. This fundamental shift in mindset, combined with disciplined budgeting practices, can help reverse the wealth destruction currently plaguing Indian households and restore the balance between present needs and future financial security.

Emergency Savings India Reality: 75% Without Safety Net

The Alarming Rainy Day Fund Gap

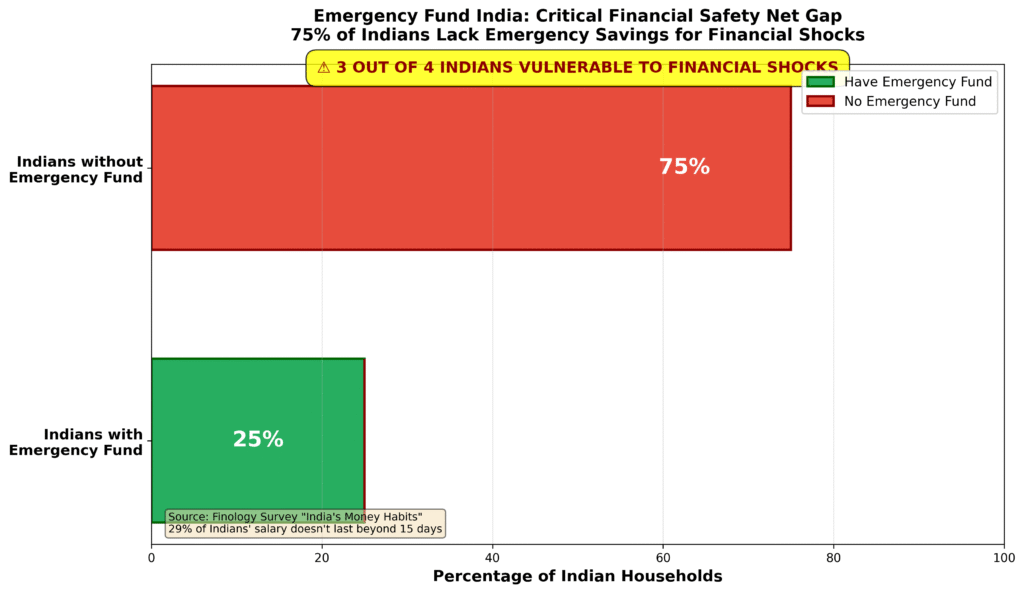

The emergency fund crisis in India has reached alarming proportions, with data revealing that 75% of Indians lack any form of emergency savings, according to the comprehensive “India’s Money Habits” survey by Finology. This means that three out of every four Indian households are completely vulnerable to financial shocks – whether from sudden job loss, medical emergencies, or unexpected expenses. The absence of a financial safety net forces families to resort to high-interest loans, liquidate long-term investments, or pledge family assets during crisis moments.

What makes this statistic particularly troubling is the cascading effect it creates. Without emergency savings, households are forced into debt cycles during unexpected events, further eroding their ability to build wealth. The survey also revealed that 29% of Indians reported their salary doesn’t last beyond 15 days of the month – highlighting how close many families live to financial disaster. This paycheck-to-paycheck existence leaves no room for building the recommended 6-8 months of emergency fund coverage.

Emergency Fund India: Building Your Financial Safety Net

The lack of emergency savings stems from multiple factors: rising cost of living, stagnant real wage growth, lifestyle inflation, and inadequate financial literacy about the importance of maintaining liquid reserves. Many Indians mistakenly view family and friends as their emergency fund, creating social and emotional complications during financial crises. One in three Indians has neither health insurance nor an emergency fund, compounding the vulnerability during medical emergencies that represent the most common financial shock for Indian households.

Creating an emergency fund requires a systematic approach. Financial experts recommend the 3-6-12 month rule: single individuals with stable jobs need 3 months of expenses, families with dependents require 6 months, while those with variable income or dependent parents should target 9-12 months of living expenses. The ideal allocation splits emergency funds across three instruments: 30% in instant-access savings accounts, 30% in fixed deposits with sweep-in facilities, and 40% in liquid mutual funds that offer 6-7% returns with next-day liquidity.

The emergency fund should cover only essential monthly expenses – rent, EMIs, utilities, groceries, insurance premiums, and a small buffer. Non-essential expenses like entertainment, dining out, and vacations should be excluded from emergency fund calculations. This focused approach ensures the fund adequately covers genuine emergencies without being unnecessarily large. For a typical urban family spending ₹50,000 monthly on essentials, the target emergency fund should range from ₹3 lakhs (6 months) to ₹6 lakhs (12 months) depending on income stability and family situation.

Building this corpus can feel overwhelming, but starting small with ₹5,000-10,000 monthly through systematic transfers makes the goal achievable within 2-3 years. The key is to treat emergency fund contributions as a non-negotiable expense – paying yourself first before allocating to discretionary spending. Every bonus, tax refund, or windfall should directly boost the emergency fund until reaching the target amount. Once established, the fund should remain untouched except for genuine emergencies, with immediate replenishment after any withdrawal to maintain the financial safety cushion that protects against future shocks.

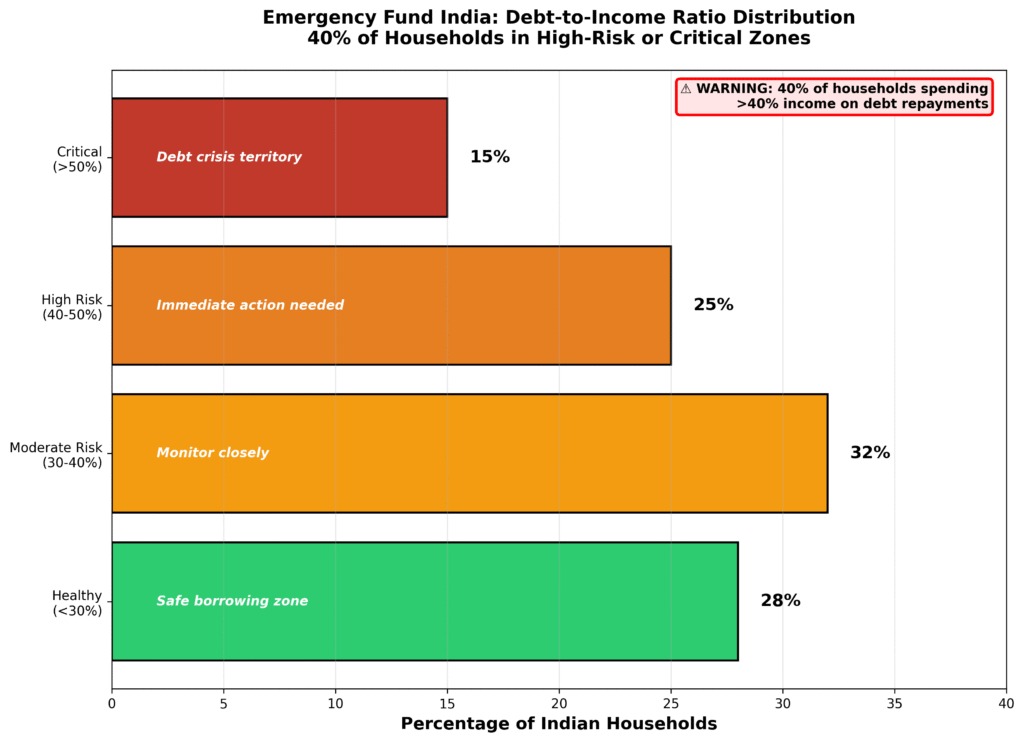

Emergency Savings India: Debt-to-Income Danger Zones

Understanding where your household stands on the debt-to-income spectrum is crucial for financial health. The debt-to-income ratio measures what percentage of your monthly income goes toward debt repayments – a critical indicator of financial stress. Only 28% of Indian households maintain the healthy zone below 30% debt-to-income ratio, while 40% of families find themselves in high-risk or critical zones spending more than 40% of their income on debt servicing.

When debt payments exceed 30% of income, households enter moderate risk territory requiring immediate attention. At 40-50%, families face high risk of default and should urgently restructure their debt obligations. Beyond 50%, households are in critical debt crisis territory where normal financial functioning becomes nearly impossible. These families often enter vicious cycles of borrowing to repay existing debt, leading to exponential growth in liabilities.

The debt-to-income calculation is straightforward: add all monthly debt payments (EMIs, credit card minimums, personal loans, gold loan interest) and divide by gross monthly income. A family earning ₹80,000 monthly and paying ₹35,000 in various EMIs has a 43.75% debt-to-income ratio, placing them in the high-risk category requiring immediate corrective action. This could involve debt consolidation at lower interest rates, income augmentation through additional earning sources, or aggressive debt elimination using the avalanche method.

Building Your Financial Safety Net: Emergency Fund Action Plan

The 50-30-20 Asset-First Budget for Emergency Fund India

Most of us need to flip our financial priorities completely to escape the debt trap that has pushed India’s household debt to GDP ratio above 41%. The traditional budgeting advice of paying bills first, then saving whatever remains, keeps us perpetually behind. Instead, we must implement an asset-first approach that prioritizes wealth building over debt accumulation from the very beginning.

The 50-30-20 Asset-First Budget Rule provides the framework we need to break this cycle. Calculate your monthly take-home income and multiply by 0.20 to determine your mandatory investment amount. This 20% goes directly into a systematic investment plan in diversified equity mutual funds on the 1st of every month, before we even consider discretionary spending. Create a simple debt-to-asset ratio tracker and aim to keep total debt below 40% of your total assets. Before taking any loan, ask yourself one critical question: will this purchase appreciate in value or generate income?

Eliminating High-Cost Debt to Build Your Rainy Day Fund India

Addressing high-cost debt can feel overwhelming, but we can take immediate steps that make a real difference within weeks. List every debt with its interest rate and target credit cards charging 18-36% annual interest for immediate elimination. Apply for a personal loan at 10-14% interest to pay off all credit card balances immediately, potentially cutting interest costs in half. Convert credit cards to emergency-only mode by removing them from wallets and online payment apps. Set up automatic payments to ensure any future credit card usage gets paid in full monthly, preventing the cycle from restarting.

After consolidating our high-cost debt, we can explore the debt avalanche method, which many find efficient for eliminating remaining obligations. Pay minimum amounts on all debts, then direct every extra rupee toward the highest-interest obligation first. This approach saves significantly more money than paying off smaller balances for emotional satisfaction. Most of us can reduce our interest burden by 50-70% through consolidation and disciplined repayment, freeing up cash flow that can finally build wealth instead of enriching lenders.

Creating Multiple Income Streams for Emergency Savings India

Creating multiple income streams becomes essential when debt payments consume more than 30% of our household income. Calculate your debt-to-income ratio by dividing total monthly debt payments by monthly income. If this exceeds 30%, immediately contact lenders to restructure payment terms or consider debt consolidation. Develop one additional income source through freelancing, part-time work, or skill monetization targeting ₹5,000-15,000 monthly. Apply the extra income rule strictly: 70% toward debt repayment, 30% toward building an emergency fund that prevents future debt accumulation.

The path out of debt requires consistent execution over 18-36 months, but the alternative of remaining trapped in high-cost debt for decades makes this temporary sacrifice worthwhile. Track your progress monthly and celebrate small wins while maintaining focus on the larger goal of financial freedom. As household debt to GDP continues rising across India, those who take decisive action now will build lasting wealth while others remain stuck in the debt cycle.

Taking Action: Your Emergency Fund India Checklist

Start Small, Think Big: Building Your Financial Safety Net

Most of us can benefit from taking steps now to manage our debt before household debt to GDP reaches levels that make recovery exponentially harder. Every month we delay starting our debt reduction plan, compound interest works against us rather than for us. Begin with one simple step this week: list every debt with its balance, minimum payment, and interest rate. This clarity often encourages immediate action by revealing the true scope of our debt.

Most of us underestimate how quickly small changes compound into major financial improvements. Redirect just ₹2,000 monthly from unnecessary expenses toward debt repayment, and watch a ₹50,000 credit card balance disappear 18 months sooner. Cancel one subscription service, pack lunch twice weekly, or sell items gathering dust at home. These micro-adjustments feel manageable but create macro results that transform our financial trajectory within months.

From Debt to Wealth: The Emergency Fund Transformation

Once we manage our debt, we find ourselves with more resources to allocate toward savings. Building better savings habits becomes natural once we eliminate high-interest debt payments that previously consumed our disposable income. The ₹8,000 monthly we once sent to credit card companies can now fund systematic investment plans, emergency funds, or skill development that increases our earning capacity. This shift from debt servicing to wealth building creates a positive feedback loop where money works for us instead of against us.

The rising household debt crisis in India affects millions of families, but we have the power to choose a different path. Start with the debt avalanche method today, create one additional income stream this month, and track progress weekly rather than hoping things improve on their own. Financial freedom requires consistent action over comfortable wishes, but the peace of mind and opportunities that emerge make every sacrifice worthwhile.

By taking control of our financial future today, we set ourselves on a path to financial independence. The compound effect of starting today versus starting next year could significantly impact the timeline of achieving financial independence. Your future self will thank you for the courage to begin this journey today.

Frequently Asked Questions: Emergency Fund India

Q: How can I break free from a debt renewal cycle like the gold loan example?

Create a structured repayment plan by allocating 20% of monthly income toward principal reduction. Consider debt consolidation at lower interest rates and avoid taking new loans until existing ones are cleared completely.

Q: Is the current household debt level dangerous for India’s economy?

Yes, the rapid increase to 41.3% of GDP is concerning. When combined with slowing income growth and rising consumption-based borrowing, it creates systemic risks that could impact financial stability and economic growth.

Q: What happens if household debt continues growing at this pace?

Continued growth could lead to widespread defaults, reduced consumer spending, and economic slowdown. Families may face asset liquidation, reduced investments in education and healthcare, creating intergenerational financial stress.

Q: How much should I keep in my emergency fund India?

Financial experts recommend 6-8 months of essential expenses for most families. Single individuals with stable jobs may manage with 3 months, while those with variable income or dependents should target 9-12 months of living expenses.

Q: Where should I keep my emergency fund for quick access?

Split your emergency corpus across three instruments: 30% in instant-access savings accounts for immediate needs, 30% in fixed deposits with sweep-in facilities for higher returns, and 40% in liquid mutual funds offering 6-7% returns with next-day liquidity.

Q: Can I use my emergency fund for investing in stocks or mutual funds?

No. Emergency funds should never be invested in volatile assets like stocks or equity mutual funds. The purpose is capital preservation and instant liquidity during crises, not wealth creation. Keep emergency money in low-risk, liquid instruments only.

Q: What’s the difference between a rainy day fund and emergency fund?

A rainy day fund (₹20,000-50,000) covers minor unexpected expenses like vehicle repairs or appliance replacement. An emergency fund (6-12 months expenses) handles major life events like job loss or medical emergencies requiring larger sums.

Q: How quickly can I build a ₹5 lakh emergency fund?

With disciplined monthly savings of ₹10,000, you can build ₹5 lakhs in approximately 50 months (4+ years). However, you can accelerate this by: directing bonuses/windfalls to the fund, creating additional income streams, and aggressively cutting discretionary spending during the initial build phase.

External Sources

About the Author: Chitransh Saxena

Chitransh Saxena is the Founder of MoneyHum and a behavioural finance specialist with over seven years of experience in global financial markets, psychology-driven money systems, and low-risk investing frameworks. His work blends data, decision science, and financial clarity to help readers build calm, reliable wealth habits.

Learn more at the full profile: moneyhum.com/about-us/

Disclaimer: This article is for educational and informational purposes only. It is not financial advice. Consult a licensed financial advisor for personalised recommendations.

Disclosure: While the core content and ideas are human, tools were utilised for research and editing.