Author’s Note

As someone who has witnessed countless talented individuals struggle to articulate their business potential to financial institutions, I understand how devastating the language barrier can be. The financial literacy gap in India isn’t just about numbers or percentages – it’s about real people with real dreams being held back by systems they cannot navigate. Through my work, I’ve seen brilliant entrepreneurs, skilled artisans, and capable women lose opportunities not because they lack talent, but because they lack the vocabulary to communicate their worth. This article reflects my commitment to breaking down these invisible barriers and making financial knowledge accessible to everyone who needs it to transform their aspirations into reality.

Key Takeaways

- Learn basic financial vocabulary including terms like interest rates, collateral, cash flow, and credit scores to communicate effectively with financial institutions

- The financial literacy gap in India affects 73% of the population, creating systemic barriers to economic participation and opportunity access

- Women face a particularly severe disadvantage with only 20% possessing adequate financial knowledge compared to higher rates for men, representing a significant gender gap in financial literacy

- Government schemes and opportunities often remain inaccessible due to communication barriers rather than lack of eligibility or business potential

Picture a talented seamstress who had built a loyal customer base working from her small tailoring setup, dreaming of expanding her business. When she heard about government schemes offering loans to women entrepreneurs, she felt this was her moment. But sitting across from the bank officer, she realized she could not explain her cash flow, did not understand interest calculations, and had no idea what collateral meant. The loan application that seemed like a golden opportunity became a wall of confusing financial jargon. She walked away empty-handed, not because she lacked business acumen, but because she lacked the financial vocabulary to communicate her potential.

Many entrepreneurs lose out on opportunities simply because we cannot speak the language of finance. This scenario plays out thousands of times across India every day, where the financial literacy gap in India creates invisible barriers between people and their aspirations. Financial literacy is not just about personal money management; it is the bridge between having dreams and accessing the tools to achieve them.

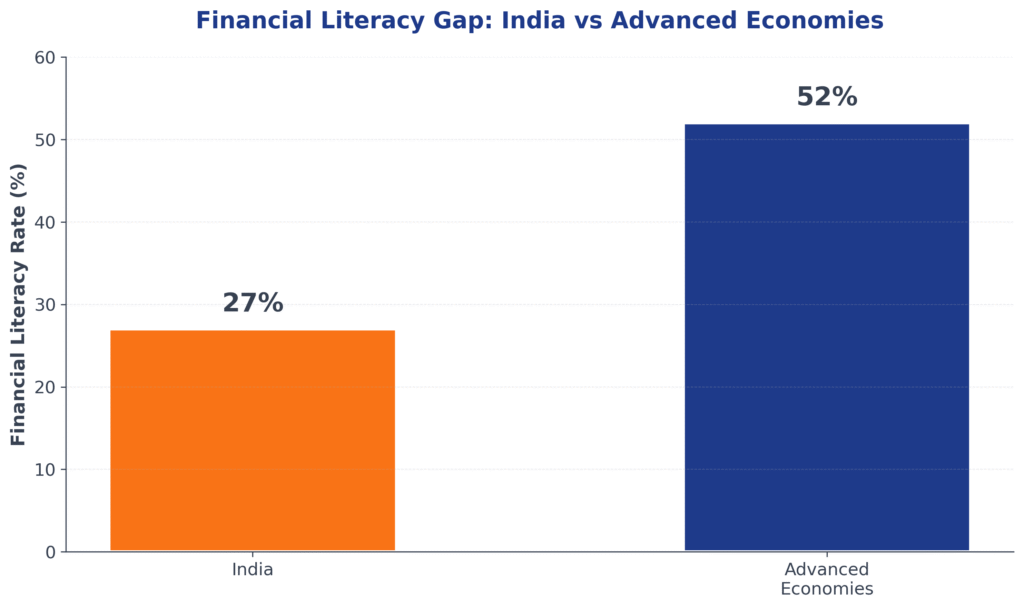

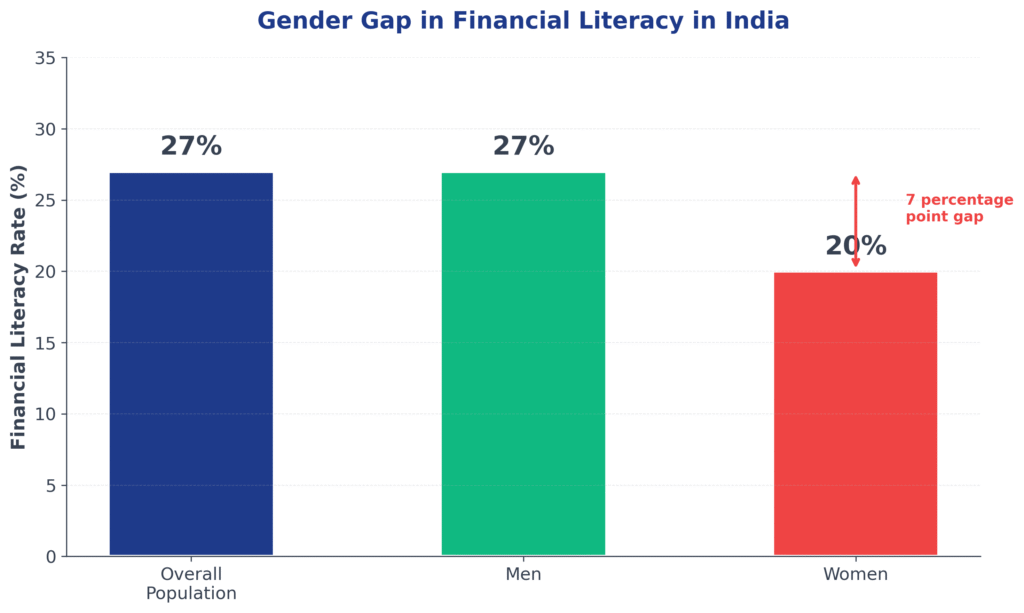

The numbers tell a stark story. Only 27% of India’s population possesses adequate financial knowledge, according to the National Centre for Financial Education. For women, this figure drops to just 20%, creating a double disadvantage in a society where financial independence often determines personal freedom. In states like Punjab, the financial literacy rate for females is only 9.8%, highlighting a significant disparity compared to 28.3% for males.

We live in an economy where financial products surround us at every turn, from digital payment apps to investment platforms, insurance policies to loan applications. Yet most of us navigate this landscape with limited understanding, making decisions based on incomplete information or avoiding opportunities altogether out of confusion. The cost is not just individual; it ripples through families, communities, and the broader economy.

This financial literacy gap in India represents more than just a knowledge deficit. It is a systemic challenge that affects everything from poverty reduction to economic growth, from gender equality to entrepreneurship. When we cannot understand the financial tools available to us, we remain passive participants in our own economic lives, dependent on others to make crucial decisions about our money and future.

Understanding this gap becomes essential for bridging it. Financial literacy matters deeply for all of us, and we can make financial knowledge accessible, practical, and empowering for every Indian, regardless of their background or current level of understanding.

Understanding the Financial Literacy Gap in India

What Financial Literacy Really Means for Indian Families

Many of us assume that a good education automatically prepares us for financial success, but The Kerala Paradox reveals a challenge in our understanding of education and competence. In a state celebrated for achieving 100% literacy, a group of college graduates recently sat for a basic financial literacy test. These were not struggling students or dropouts but the pride of Kerala’s education system, fluent in multiple languages and skilled in technology. When faced with simple questions about compound interest, insurance basics, or investment fundamentals, they scored barely 44%. One graduate later admitted being able to solve complex calculus problems but never learned how credit card interest actually worked. Despite academic brilliance, this person remained financially vulnerable in ways that would cost thousands over a lifetime.

This disconnect between traditional education and financial knowledge affects millions across India. We can master advanced subjects, excel in professional fields, and navigate complex technologies, yet remain confused when choosing between mutual funds or understanding loan terms. The financial literacy gap in India creates a peculiar situation where highly educated individuals make poor financial decisions simply because nobody taught them the basics of money management.

Most of us experience this knowledge gap daily without fully recognizing it. We might delay investing because the options seem overwhelming, choose insurance policies based on agent recommendations rather than actual needs, or avoid taking beneficial loans because we cannot calculate the real costs. These decisions compound over time, creating missed opportunities and unnecessary expenses that affect our long-term financial security.

The Kerala Paradox: Education vs Financial Knowledge

The emotional toll of financial illiteracy extends beyond money itself. When we lack confidence in financial decision-making, we experience stress, anxiety, and a sense of helplessness about our economic future. Many Indians report feeling overwhelmed when discussing investments with friends or family, leading to either paralysis or impulsive decisions based on fear rather than understanding. This confidence crisis over financial literacy in young adults particularly affects career starters who earn well but struggle with basic money management.

Financial literacy represents a skill set that requires intentional learning, separate from traditional academic education. Unlike subjects taught in school, financial knowledge must be actively sought out and applied to real-life situations. The encouraging news is that basic financial concepts are not inherently complex; they simply require dedicated time and practice to master, making this gap entirely bridgeable with the right approach and resources.

Gender Gap in Financial Literacy Across India

Women’s Financial Literacy Crisis: Only 20% Are Financially Literate

Gender differences in financial knowledge create a particularly concerning aspect of India’s financial literacy challenge. Many of us witness this disparity in our own families and communities, where women face significantly greater barriers to understanding money management. Only 20% of women possess adequate financial literacy compared to 27% of men, and while this seven-percentage-point difference might seem modest, it translates into millions of women making financial decisions without proper knowledge or avoiding financial decisions altogether.

Many families find themselves dealing with severe gender-based divides in financial understanding. In states like Punjab, we see stark differences with 28.3% of males demonstrating financial literacy versus just 9.8% of females. This disparity creates households where financial decisions rest entirely with men, leaving women dependent and uninformed about their own economic security. Many of us have observed this pattern in rural and traditional communities, where cultural norms often exclude women from financial discussions and decision-making processes.

Punjab’s Severe Gender Disparity in Financial Education

These statistics translate into real barriers for women’s economic participation and independence. When women lack financial knowledge, they cannot effectively negotiate salaries, manage household budgets, or make informed decisions about savings and investments. This knowledge gap becomes especially problematic during life transitions such as widowhood, divorce, or sudden financial responsibility, where women without financial literacy find themselves vulnerable and dependent on others who may not have their best interests at heart.

The consequences extend beyond individual women to affect entire families and communities. Children whose mothers lack financial literacy often inherit poor money management habits, perpetuating cycles of financial vulnerability across generations. Women entrepreneurs, who could drive significant economic growth, remain unable to access credit or scale their businesses because they cannot communicate effectively with financial institutions or understand the terms being offered to them.

Cultural Barriers Preventing Women’s Financial Independence

Breaking this cycle requires targeted intervention that acknowledges both the knowledge deficit and the cultural barriers women face. Financial literacy programs designed specifically for women must address not just technical concepts but also confidence-building and practical application in contexts relevant to their daily lives. Success stories from women who have gained financial independence through education serve as powerful motivators for others facing similar challenges.

Practical Solutions to Bridge India’s Financial Literacy Gap

Daily Learning Routines for Financial Knowledge Building

Individual learning routines work exceptionally well when combined with community support, particularly for women who face unique financial challenges. Creating local learning circles of 5-8 women provides the social reinforcement that makes financial concepts less intimidating and more achievable. These groups meet weekly for one hour, discussing topics like opening savings accounts, understanding interest rates, or planning for emergencies using examples from their own lives. The shared experience builds confidence while practical activities like visiting banks together or practicing mobile banking applications remove barriers that often prevent women from engaging with financial services.

Community-Based Financial Literacy Programs for Women

Students and young adults need gamified approaches that make financial learning engaging rather than burdensome. The money management challenge transforms abstract concepts into concrete actions by using expense tracking apps, creating mock budgets with real income sources, and starting small investments through user-friendly platforms. When a college student begins tracking expenses for 30 days using apps like Walnut, they discover spending patterns that reveal opportunities for better money management without feeling restricted or overwhelmed. Understanding these patterns becomes crucial as young people face increasing financial pressures, including India’s Household Debt-Surge that affects families across all income levels.

Gamified Financial Learning for Students and Young Adults

Success in addressing India’s financial literacy gap comes from making learning practical, social, and immediately applicable to daily life. We must focus on building habits that create lasting behavioral changes rather than simply memorizing financial terms or formulas. The combination of daily learning routines, community support systems, and hands-on practice with real money creates the foundation for genuine financial competence that serves individuals throughout their lives.

Moving Forward: Closing the Financial Literacy Gap

Small Actions That Create Lasting Financial Impact

The statistics provide a clear view of our current situation. Only 27% of India’s population possesses adequate financial knowledge, with women facing even steeper challenges at just 20% literacy rates compared to 27% for men. In states like Punjab, only 9.8% of females are financially literate, highlighting significant gender disparity. Yet these numbers also represent significant potential for growth and positive change.

Small actions today create lasting impact tomorrow. We can begin by dedicating just 10 minutes daily to learning one financial concept, whether through apps, videos, or simple conversations with financially savvy friends. Opening that first savings account, downloading an expense tracking app, or attending a community workshop may seem insignificant, but these steps build the foundation for comprehensive financial competence. The Reserve Bank of India’s Financial Inclusion Index shows 4.3% growth in FY25, proving that collective efforts toward better financial literacy are already showing results.

Building Community Support Networks for Financial Education

Community involvement enhances individual efforts significantly. When we share our learning journey with family members, friends, or colleagues, we create support networks that sustain long-term behavioral changes. A mother teaching her daughter about budgeting while learning herself, or friends challenging each other to save specific amounts monthly, transforms financial education from solitary struggle into shared growth experience.

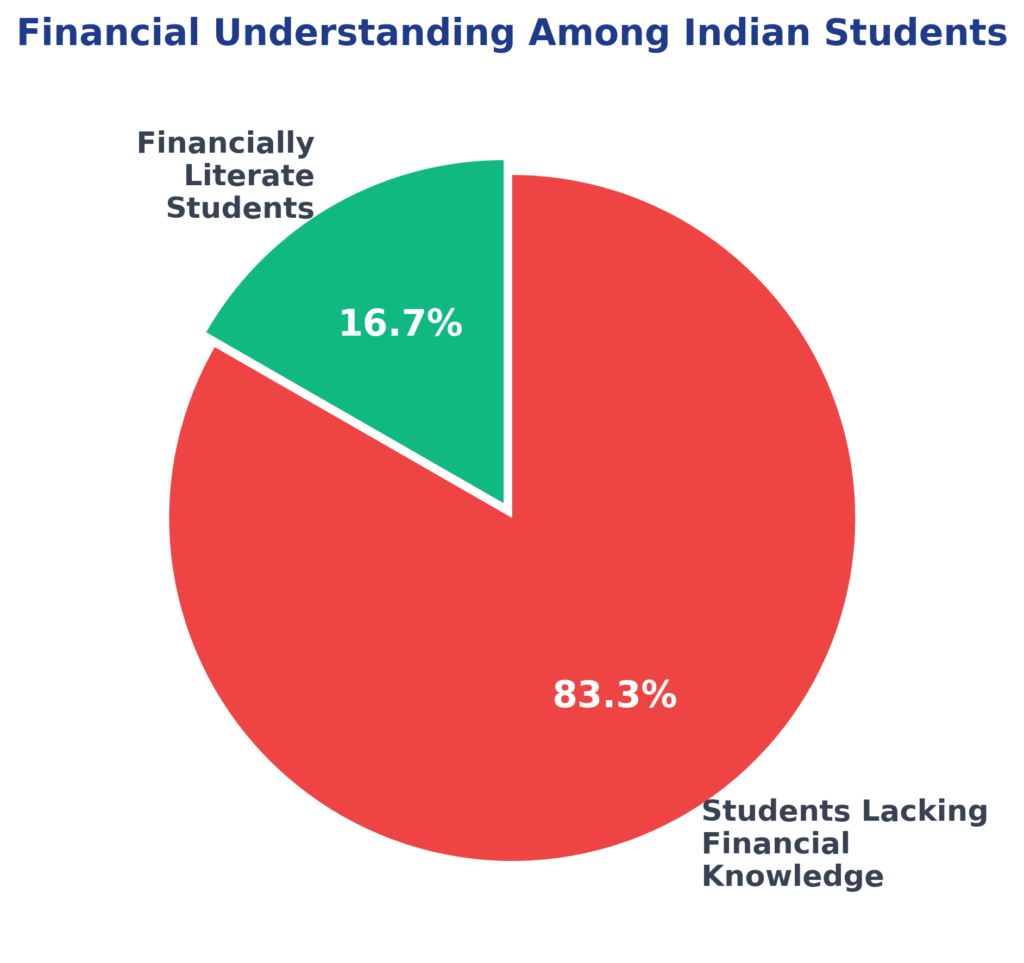

Understanding financial concepts is crucial, especially when only 16.7% of Indian students grasp basic money management skills. Today’s financial decisions shape tomorrow’s economic stability, making immediate action essential rather than optional. Rising household debt levels across the country, detailed in Household Debt to GDP India, underscore why developing financial literacy should not be delayed until conditions are perfect or knowledge is complete.

Your financial journey begins with the next choice you make. Whether that means opening your first investment account, creating a monthly budget, or simply starting to track daily expenses, taking steps forward is more beneficial than overanalyzing. We have the tools, resources, and growing awareness needed to bridge India’s financial literacy gap. The question is not whether we can improve our financial knowledge, but whether we will choose to start today.

Every financially literate person becomes a catalyst for broader change within their family and community. As more individuals develop these crucial skills, we collectively build a more financially resilient nation where informed decisions replace guesswork and strategic planning replaces reactive spending. The transformation begins with you, today, with whatever small step feels most manageable and meaningful for your current situation.

FAQs About Financial Literacy Gap in India

Q: What are the most important financial terms every entrepreneur should know? Key terms include cash flow (money coming in and out), collateral (assets securing loans), interest rates, credit scores, profit margins, and working capital. Understanding these basics enables meaningful conversations with lenders and investors.

Q: How does poor financial literacy specifically impact women entrepreneurs? Women entrepreneurs face dual challenges: lower financial literacy rates (20% vs higher male rates) and cultural barriers to financial discussions. This limits access to funding, business growth opportunities, and financial independence.

Q: Can someone build a successful business without formal financial education? While possible, lack of financial literacy creates significant barriers to scaling, accessing funding, and making informed decisions. Basic financial knowledge dramatically improves success rates and growth potential for any business venture.

External Sources

- Ministry of Women and Child Development – Women Entrepreneurship Data

- National Centre for Financial Education – Financial Literacy Statistics India

- Reserve Bank of India – Financial Inclusion Reports

- National Sample Survey Office – Household Financial Literacy Studies

About the Author: Chitransh Saxena

Chitransh Saxena is the Founder of MoneyHum and a behavioural finance specialist with over seven years of experience in global financial markets, psychology-driven money systems, and low-risk investing frameworks. His work blends data, decision science, and financial clarity to help readers build calm, reliable wealth habits.

Learn more at the full profile: moneyhum.com/about-us/

Disclaimer: This article is for educational and informational purposes only. It is not financial advice. Consult a licensed financial advisor for personalised recommendations.

Disclosure: While the core content and ideas are human, tools were utilised for research and editing.