Author’s Note

As someone who has worked closely with families struggling with financial challenges, I’ve witnessed firsthand how transformative proper financial education can be. The story of that mother resonates deeply with me because it represents thousands of families I’ve encountered who simply needed the right tools and knowledge to break free from cycles of financial stress. Financial Literacy in Young Adults isn’t just an academic concept—it’s a lifeline that can determine whether the next generation thrives or merely survives financially. Through my work, I’ve learned that even small steps toward financial understanding can create ripple effects that benefit entire communities. Every time I see a young person confidently make their first investment or successfully manage their budget, I’m reminded why this mission matters so much.

Key Takeaways

- Start tracking your expenses immediately using simple mobile apps to identify hidden money drains that could be costing you thousands monthly

- Financial Literacy in Young Adults serves as the foundation for breaking generational cycles of debt and building long-term wealth for families

- Address Financial Decision-Making Anxiety by starting with small, manageable financial goals rather than overwhelming yourself with complex investment strategies

- Join local financial literacy programs or online communities where you can learn practical money management skills alongside peers facing similar challenges

Every parent knows the stress of managing family finances while feeling completely lost about money management. Picture a mother of two young children struggling with a complex array of family expenses, credit card bills, and informal loans from relatives. Every month felt like a juggling act, paying school fees while avoiding late charges, borrowing from one source to pay another. When she joined a local financial literacy program, she learned to track her spending using a simple mobile app and discovered she was losing ₹3,000 monthly to unnecessary charges and poor planning. Within six months, she had created her first emergency fund and was teaching her neighbors the same budgeting techniques that transformed her financial chaos into clarity.

This story reflects a harsh reality across India today. Only 24% of Indian adults possess basic financial literacy skills, while the situation among young adults is even more concerning. Financial decision-making anxiety runs high among this demographic, severely impacting their confidence in investments and savings when they need it the most. We are witnessing an entire generation entering their earning years without the fundamental knowledge to manage their money effectively.

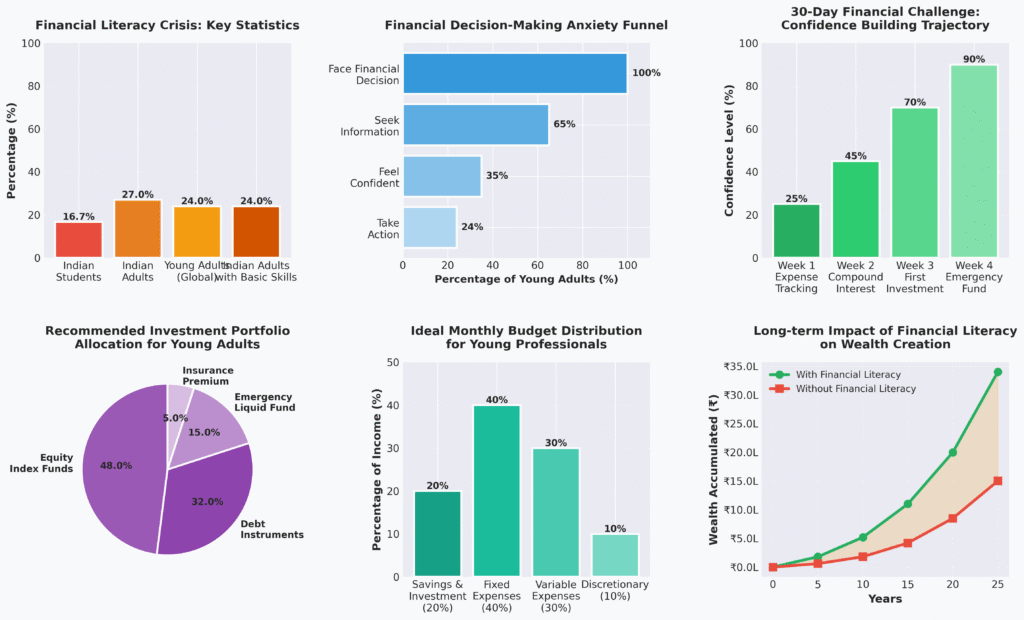

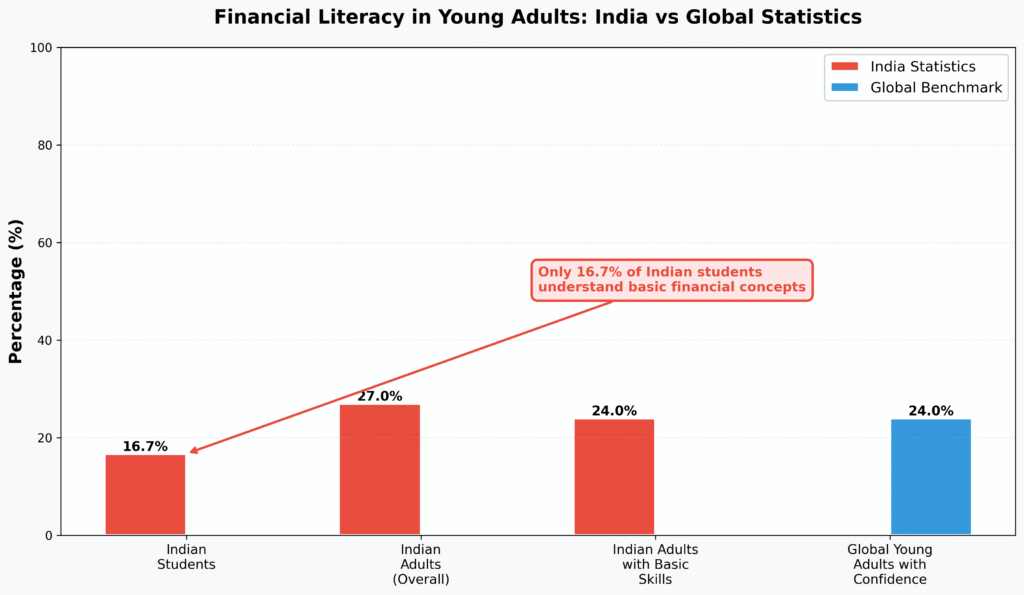

India’s financial literacy crisis: Only 16.7% of students and 24% of adults understand basic financial concepts compared to global benchmarks

Her experience mirrors what millions of Indian families face daily, highlighting the widespread lack of basic financial education in our society. The numbers paint a concerning picture of our financial education crisis. Research shows that only 16.7% of Indian students understand basic financial and money management concepts, setting them up for years of financial struggles ahead. When we examine Financial Literacy Gap in India, the scope of this challenge becomes evident across all age groups and regions.

Young adults today face complex financial decisions about student loans, credit cards, investments, and insurance without adequate preparation. We are essentially asking them to navigate sophisticated financial markets with elementary school-level knowledge. Financial literacy in young adults represents a critical life skill that determines long-term economic stability and growth.

Many families face vulnerability to predatory lending, poor investment choices, and debt cycles that can persist for decades when young adults lack financial literacy. We see families trapped in patterns of financial stress that could be prevented with proper education and planning tools. The mother in our opening story represents millions of Indians who discover financial wisdom too late, after years of costly mistakes.

Understanding this crisis is the first step toward building a financially literate generation. We must examine why traditional education systems fail to prepare young adults for real-world money management and explore practical solutions that can bridge this dangerous knowledge gap before it widens further.

The Reality of Financial Literacy Gap Among Young Adults

Most of us who graduated in recent years find ourselves in an impossible situation. We possess advanced technical skills and can navigate complex digital platforms, yet we struggle with basic financial decisions that will shape our entire future. A software engineer earning ₹80,000 monthly might excel at coding algorithms but feel completely lost when choosing between term insurance policies or understanding how mutual fund expense ratios affect long-term returns.

Consider a recent graduate who landed a dream job at a multinational company. Despite impressive academic credentials, this person found themselves overwhelmed by decisions about employee provident fund contributions, health insurance options, and tax-saving investments. They could build sophisticated mobile applications but could not distinguish between a fixed deposit and a systematic investment plan. Their first year of working became a series of costly financial mistakes that could have been avoided with basic money management knowledge.

Comprehensive analysis: Financial literacy rates, anxiety funnel, 30-day challenge progress, investment allocation, budget distribution, and long-term wealth impact

We face unique financial challenges that previous generations never encountered. Online lending platforms, cryptocurrency investments, and digital payment systems create both opportunities and risks that require sophisticated understanding. We must navigate peer-to-peer lending, robo-advisors, and complex investment apps without adequate preparation. We are digitally native but financially vulnerable, a combination that makes us prime targets for financial scams and poor investment decisions.

Understanding the Urban-Rural Financial Literacy Divide

This knowledge gap extends beyond individual choices to affect our entire families and communities. When we lack financial literacy, we cannot break cycles of debt, build generational wealth, or make informed decisions about major purchases like homes and vehicles. The Urban-Rural Literacy Divide shows how this problem varies across different regions, with urban youth facing different but equally challenging financial complexities.

H3: The Paralyzing Effect of Financial Decision-Making Anxiety

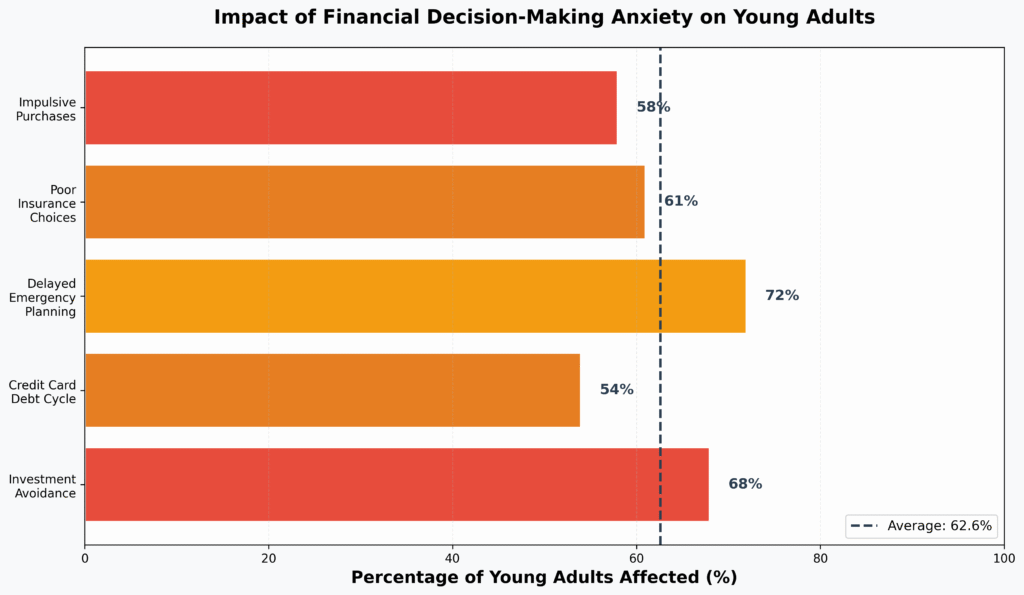

Many of us experience financial decision-making anxiety that creates a paralyzing effect where we avoid important financial choices altogether. We delay investing, skip insurance coverage, or make impulsive purchases because we lack confidence in our financial judgment. This avoidance behavior compounds over time, as delayed financial decisions become increasingly expensive and complex to address later in life.

The cost of this financial illiteracy extends far beyond our individual bank accounts. We see young adults trapped in credit card debt cycles, falling victim to investment frauds, and missing opportunities for wealth creation during their highest earning potential years. Our families suffer when financial emergencies arise without proper planning, and the broader economy loses productive investment capital that could fuel growth and innovation.

Financial Decision-Making Anxiety: The Hidden Crisis in Young Adults

The anxiety surrounding financial decisions creates a particularly vicious cycle for young adults today. Most of us have experienced that overwhelming feeling when faced with investment options, insurance policies, or even choosing the right savings account. We scroll through countless financial apps, read conflicting advice online, and end up paralyzed by the fear of making the wrong choice. This decision-making anxiety is so prevalent that many of us simply avoid financial planning altogether, telling ourselves we will figure it out later when we have more money or more knowledge.

How financial anxiety affects young adults: Investment avoidance (68%), emergency planning delays (72%), and poor insurance choices (61%) dominate behavioral patterns

Breaking the Cycle Through Practical Financial Skills

The root cause of this anxiety stems from a fundamental mismatch between the complexity of modern financial products and our preparation level. Banks offer dozens of account types, investment platforms present hundreds of fund options, and insurance companies sell policies with technical jargon that sounds like a foreign language. Without basic financial literacy in young adults, these choices feel impossible to navigate confidently.

What makes this situation particularly frustrating is that most financial decisions are not actually that complicated once we understand the fundamentals. The difference between a term insurance policy and an endowment plan becomes clear with just thirty minutes of focused learning. Understanding how expense ratios affect mutual fund returns requires basic math skills we already possess. The knowledge barrier is much lower than we imagine, but the anxiety makes it feel insurmountable.

The 30-Day Path to Financial Confidence

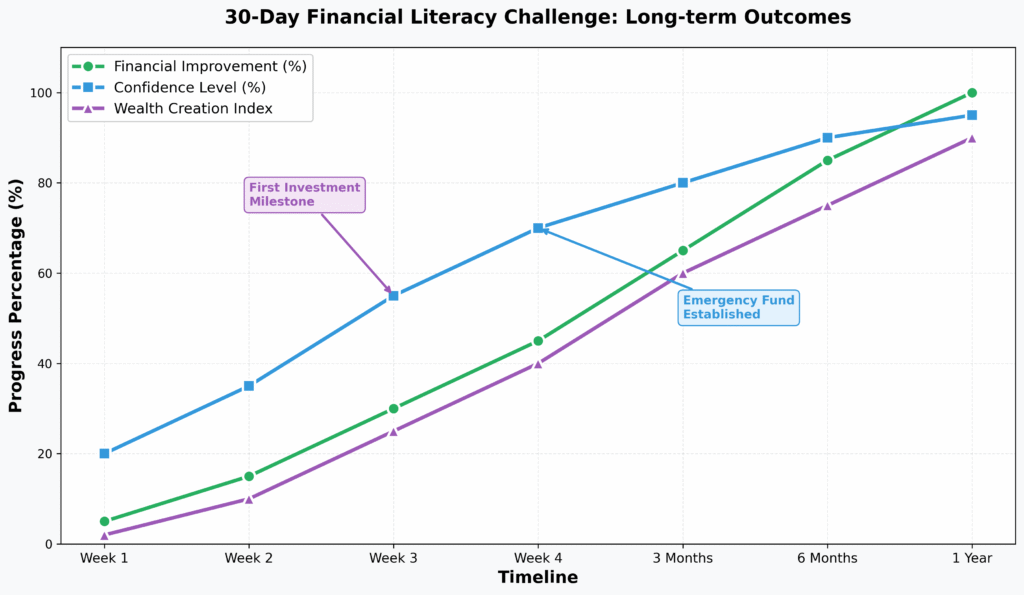

We can break this anxiety cycle through a structured approach that builds confidence through small, achievable actions. Instead of trying to master all financial concepts at once, we can focus on one specific area each week, creating tangible progress that reduces our anxiety while building genuine competence. This gradual approach transforms overwhelming financial literacy into manageable steps that fit into our busy lives.

Progressive improvement trajectory: Financial literacy challenge showing confidence building from 20% to 95% and wealth creation from basic to advanced levels over one year

The first week focuses purely on awareness through expense tracking. We can download a free budgeting app like Mint or YNAB and record every purchase for seven days, no matter how small. This simple exercise reveals spending patterns often unnoticed and creates the foundation for all our future financial decisions. By week two, we shift focus to understanding compound interest using online calculators to see how ₹1000 invested monthly for ten years can grow to surprising amounts. This visualization makes the abstract concept of long-term investing feel real and achievable for us.

Week three introduces actual investing through a systematic investment plan with just ₹500 monthly in an index fund. This amount feels manageable while providing genuine market experience and the satisfaction of taking concrete action. The final week establishes emergency planning by setting up automatic transfers to a separate savings account, creating a safety net that reduces our financial anxiety. Within 30 days, we will have experienced budgeting, investing, and emergency planning firsthand rather than just reading about them.

Building Long-term Financial Security Systems

Once we have established these basics through our 30-day challenge, we can explore more sophisticated strategies to enhance our financial journey. Implementing a gradual investment strategy builds our confidence through controlled exposure, starting with just ₹100 monthly in a liquid fund to understand mutual fund mechanics without significant risk. After two months of comfort with this process, we can add ₹200 monthly to an equity index fund while using educational investment apps like Groww or Zerodha Coin. These platforms combine learning with doing, making the investment process less intimidating for us through built-in guidance and community features.

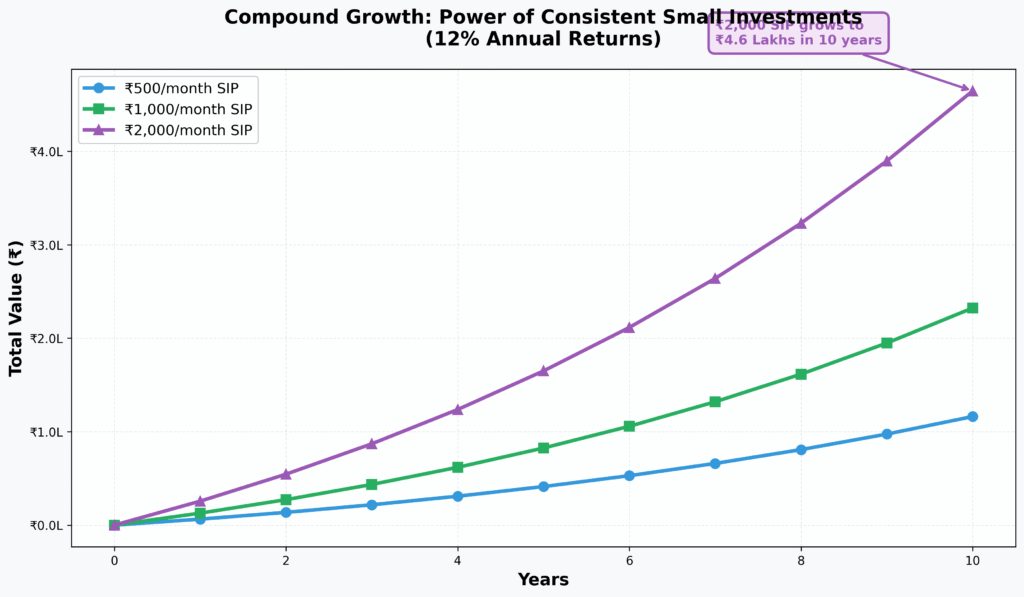

Mathematical proof: ₹500 monthly SIP grows to ₹1.16L, ₹1,000 to ₹2.32L, and ₹2,000 to ₹4.65L in 10 years at 12% annual returns through compound interest

Creating long-term financial security requires multiple layers of protection and income diversification that we can build systematically. Our priority involves building a six-month emergency fund starting with ₹1000 monthly contributions, followed by securing basic term life insurance coverage of ₹50 lakh, which costs approximately ₹8000 annually for a 25-year-old. Simultaneously, we should develop skills in a secondary area for additional income potential while investing 20% of our income in a diversified portfolio split between 60% equity and 40% debt instruments. This comprehensive approach addresses both our immediate security needs and long-term wealth building goals.

The transformation from financial anxiety to confidence happens through consistent small actions rather than dramatic changes. Each step we complete, whether tracking expenses for a week or making our first mutual fund investment, builds evidence that we can handle financial responsibility. This evidence-based confidence proves far more durable than confidence built on theoretical knowledge alone, creating a foundation for increasingly sophisticated financial decisions as our income and experience grow.

Moving Forward: From Financial Anxiety to Empowerment

Many of us feel overwhelmed when we see the financial literacy statistics in our country. With only 16.7% of Indian students understanding basic money management and merely 27% of adults possessing adequate financial knowledge, we face a generation-wide challenge that demands immediate action. These numbers represent real people struggling with financial decisions that will shape their futures, but they also represent an opportunity for those willing to break free from this cycle.

Taking the First Step Today

Addressing this widespread challenge begins with individual actions we can take today. Transforming our financial future only requires opening a notebook and writing down every expense for the next seven days. This simple act begins rewiring our relationship with money from passive to active, from anxious to informed. Within two weeks, we can download a budgeting app and categorize these expenses, creating our first clear picture of where our money actually goes versus where we think it goes.

Building Sustainable Financial Habits

Building on this foundation, our path from financial anxiety to confidence unfolds through these small, consistent actions rather than waiting for the perfect moment or complete knowledge. Each month we track expenses, each mutual fund investment we make, each emergency fund contribution we complete builds tangible evidence that we can handle financial responsibility. This evidence-based confidence proves far more reliable than theoretical knowledge alone.

What makes this journey achievable is that financial literacy in young adults transforms from an overwhelming concept to manageable skill development when we focus on implementation over perfection. The young professional who starts with a ₹1000 monthly SIP today will have developed both the habit and the knowledge needed to make increasingly sophisticated financial decisions as their career progresses. Their future self will thank them not for waiting until they understood everything, but for starting with what they knew.

Today presents us with a clear choice: we can remain part of the 83.3% who struggle with basic financial concepts, or we can join the minority who take control of their financial future starting right now. The tools, platforms, and information we need are readily available. What matters now is taking that first small step, because every expert was once a beginner who decided to begin.

Frequently Asked Questions About Financial Literacy in Young Adults

Q: What’s the most important financial skill young adults should learn first?

Expense tracking and budgeting form the cornerstone of financial health. Before investing or taking loans, young adults must understand where their money goes and create realistic spending plans that align with their income and goals.

Q: How can parents help their children develop better financial habits?

Parents should involve children in age-appropriate financial discussions, demonstrate good money management behaviors, and encourage hands-on experiences like managing small allowances or part-time job earnings with proper guidance and support.

Q: What should I do if I’m already struggling with debt as a young adult?

Start by listing all debts, prioritize high-interest obligations, and consider debt consolidation options. Seek guidance from financial counselors or literacy programs, and focus on building emergency savings alongside debt repayment strategies.

External Sources and Research References

- Reserve Bank of India Financial Literacy Survey Reports

- National Centre for Financial Education (NCFE) research data

- Ministry of Finance financial inclusion statistics

- Academic research on financial literacy among Indian youth demographics

About the Author: Chitransh Saxena

Chitransh Saxena is the Founder of MoneyHum and a behavioural finance specialist with over seven years of experience in global financial markets, psychology-driven money systems, and low-risk investing frameworks. His work blends data, decision science, and financial clarity to help readers build calm, reliable wealth habits.

Learn more at the full profile: moneyhum.com/about-us/

Disclaimer: This article is for educational and informational purposes only. It is not financial advice. Consult a licensed financial advisor for personalised recommendations.

Disclosure: While the core content and ideas are human, tools were utilised for research and editing.