Author’s Note

The story of that tea shop owner’s daughter in Kerala perfectly captures something I’ve witnessed countless times—brilliant minds held back not by ability, but by location. The Urban-Rural Literacy Divide isn’t just about statistics; it’s about families making heartbreaking choices between opportunity and togetherness. When I see parents sacrificing everything to move their children to cities for better education, I’m reminded that technology should be bridging these gaps, not widening them. Every village deserves its own success story.

Key Takeaways

- Establish community-driven digital learning centers that combine technology access with local mentorship programs

- The Urban-Rural Literacy Divide requires targeted investment in both infrastructure and teacher training to create sustainable change

- Address the Educational Infrastructure Gap by prioritizing internet connectivity and digital device access in underserved areas

- Support local entrepreneurs and educators who can maintain long-term educational initiatives within their communities

Most parents across India share a common fear: watching their children face a difficult choice between pursuing opportunities and staying close to family. Geography still plays a significant role in shaping our destinies in a rapidly digitalizing nation.

A small farming community in Kerala recently discovered something that challenges this assumption entirely. When the government established a digital learning center in their village, the local tea shop owner’s daughter became the first in her family to touch a computer. She had never imagined learning to code, yet within two years, she was earning more than her father through freelance web design while remaining in the village she loved. The center did not just teach technology—it taught an entire community that distance from cities does not have to mean distance from opportunity.

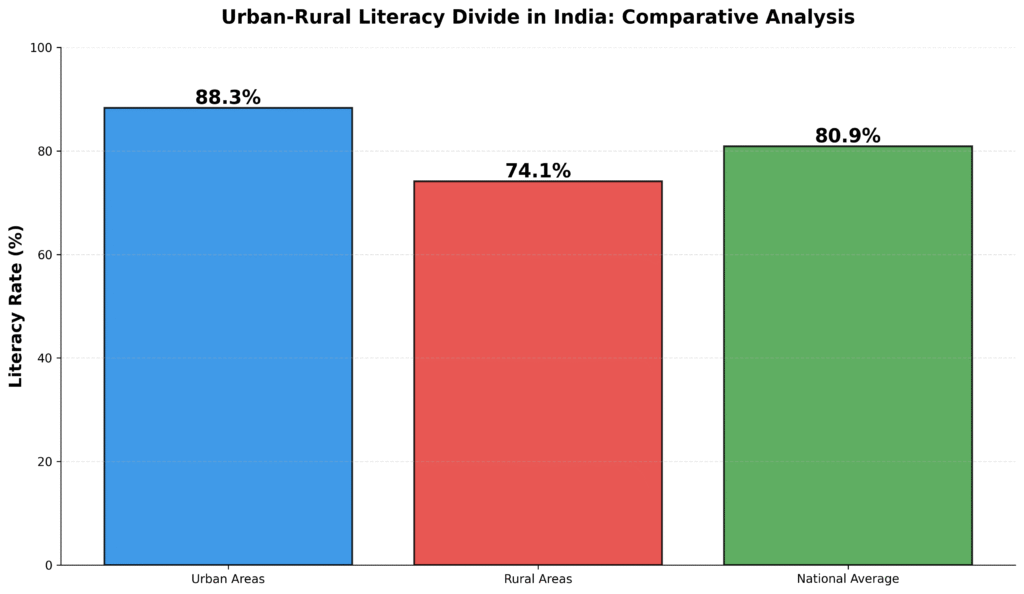

This example from Kerala highlights broader trends seen in national literacy statistics. While our national literacy rate has reached 80.9%, the gap between urban areas at 88.3% and rural regions at 74.1% tells only part of the story. Behind these numbers lie millions of families where talent remains untapped simply because of location.

Figure 1: Comparative analysis showing the 14.2 percentage point gap between urban (88.3%) and rural (74.1%) literacy rates against the national average (80.9%)

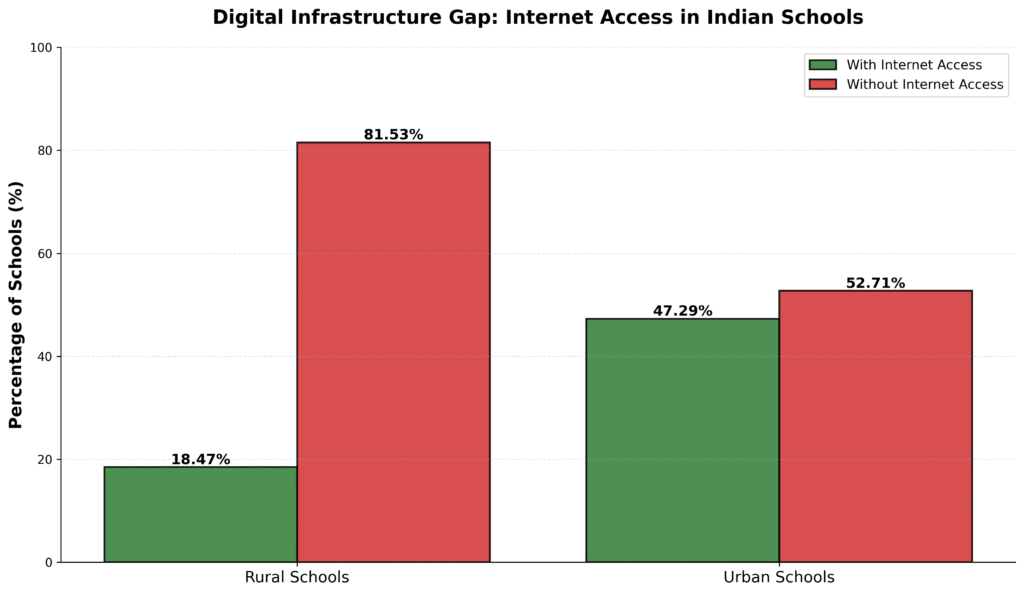

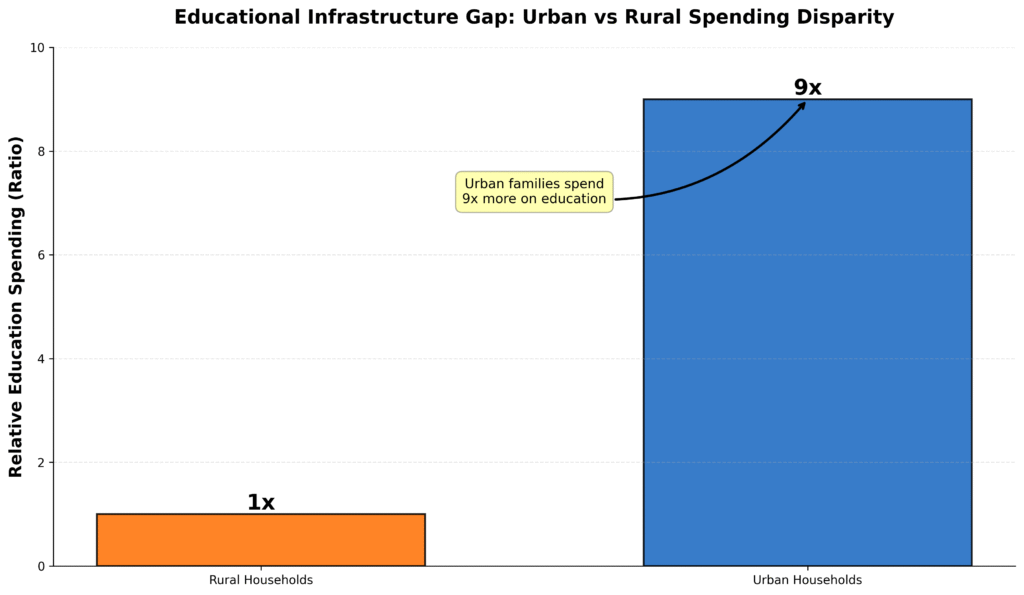

We live in an era where a stable internet connection can matter more than physical proximity to educational institutions. Yet only 18.47% of rural schools have internet access compared to 47.29% in urban areas. Urban families spend nearly nine times more on education than their rural counterparts, creating barriers that extend far beyond simple geographic boundaries.

The implications reach into every aspect of economic development and social mobility. When rural areas face significant teacher shortages and limited digital infrastructure, we are not just discussing education statistics—we are talking about the future earning potential of entire communities. We should consider how to replicate the Kerala village’s success story across similar communities nationwide.

To truly grasp this divide, we must consider more than just literacy rates and examine how access to quality education shapes long-term financial outcomes for families across different regions.

(Read – Household Debt to GDP India: 42.9% Ratio Signals Rising Risk)

The Financial Burden: Urban Education Costs and Household Strain

The financial reality hits hardest when school admission season arrives. We find ourselves caught in an impossible equation: quality education costs that consume 30-40% of household income, leaving little room for other essential expenses or savings. A software engineer earning ₹8 lakhs annually discovers that educating two children in decent schools requires ₹2.5 lakhs per year, forcing us to make difficult choices between present comfort and future security.

Most of us approach education expenses reactively, scrambling for funds when fee deadlines approach. This panic-driven approach often leads to depleting our emergency savings, taking high-interest personal loans, or compromising on the quality of education for our children. The emotional toll becomes as severe as the financial burden, with sleepless nights wondering if we can sustain these expenses through our children’s entire academic journey.

Yet some families break free from this cycle through strategic planning. A transport worker’s story illustrates how methodical preparation transforms educational investments. Despite limited income, he enrolled all three children in an affordable quality school, stretching his budget thin initially. His approach of setting aside small amounts monthly, combined with researching scholarship opportunities, eventually paid remarkable dividends. His eldest daughter now studies engineering on a scholarship, proving that consistent investment in education creates generational change regardless of our starting income levels.

Strategic Education Fund Planning for Long-Term Security

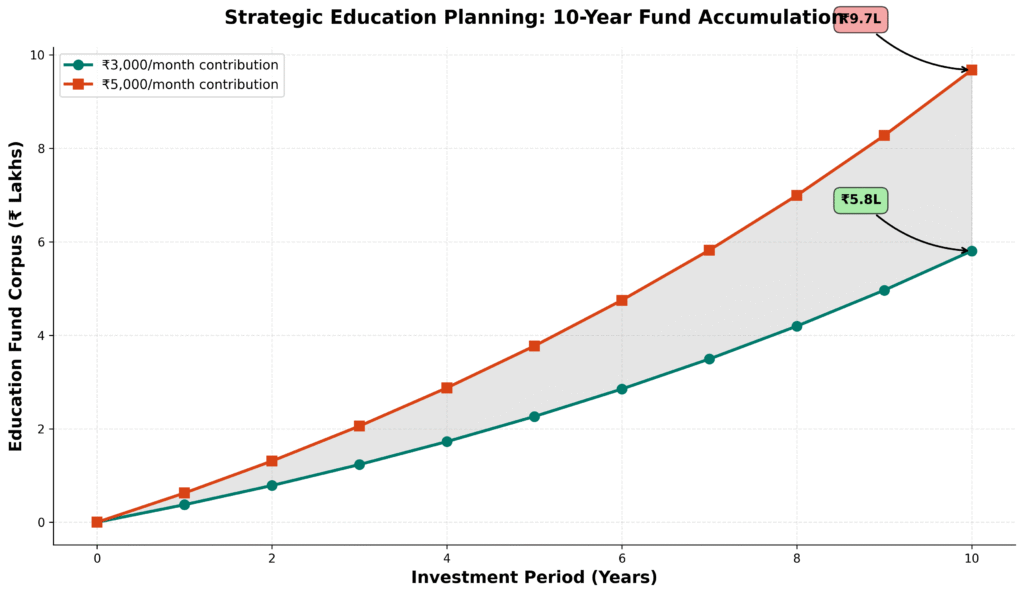

The solution lies in treating education as a long-term financial goal rather than an annual expense crisis. Creating a dedicated education fund through systematic investments can accumulate ₹5-8 lakhs over 10 years with monthly contributions of just ₹3,000-5,000. This approach, combined with exploring education loans at favorable rates and government scholarship programs, reduces our immediate financial stress by 40-50% while ensuring uninterrupted quality education.

Figure 2: Ten-year education fund accumulation showing how monthly contributions of ₹3,000-5,000 can build a corpus of ₹5.8-9.7 lakhs at 9% annual returns

We can also negotiate payment flexibility with schools, spreading annual fees across monthly installments rather than paying lump sums. Some of us form cooperative groups for shared tutoring costs, reducing individual expenses while maintaining educational quality. These strategies require initial effort but create sustainable systems that eliminate the annual education expense panic that affects most urban households.

(Read – No Emergency Fund: 3 in 4 Indians Lack Safety Net)

Digital Literacy Divide: The Educational Infrastructure Gap

We often see talented students in remote villages facing a different kind of educational barrier that goes beyond books and fees. The digital divide creates an invisible wall between rural and urban learning opportunities, with only 18.47% of rural schools having internet access compared to 47.29% in urban areas. This gap affects not just current learning but future career prospects, as digital literacy becomes important for most modern jobs.

Figure 3: Critical infrastructure gap showing that 81.53% of rural schools lack internet access compared to 52.71% of urban schools

Consider a talented student in a remote village who excels in mathematics but has never used a computer. While her urban counterpart attends online coding classes and accesses global educational resources, she struggles to even understand what these opportunities look like. This urban-rural literacy divide extends beyond traditional reading and writing to include digital skills that determine economic mobility in today’s world.

We witness the emotional toll on rural families as parents watch their children’s potential constrained by geographical limitations, knowing that lack of digital exposure will handicap them in future job markets. Teachers in rural schools often feel inadequately prepared to guide students toward technology-based careers, creating a cycle where limited exposure leads to limited aspirations. Rather than accepting these limitations, we can address them through practical community solutions that make digital access affordable and sustainable.

Community-Based Education Solutions Through Digital Hubs

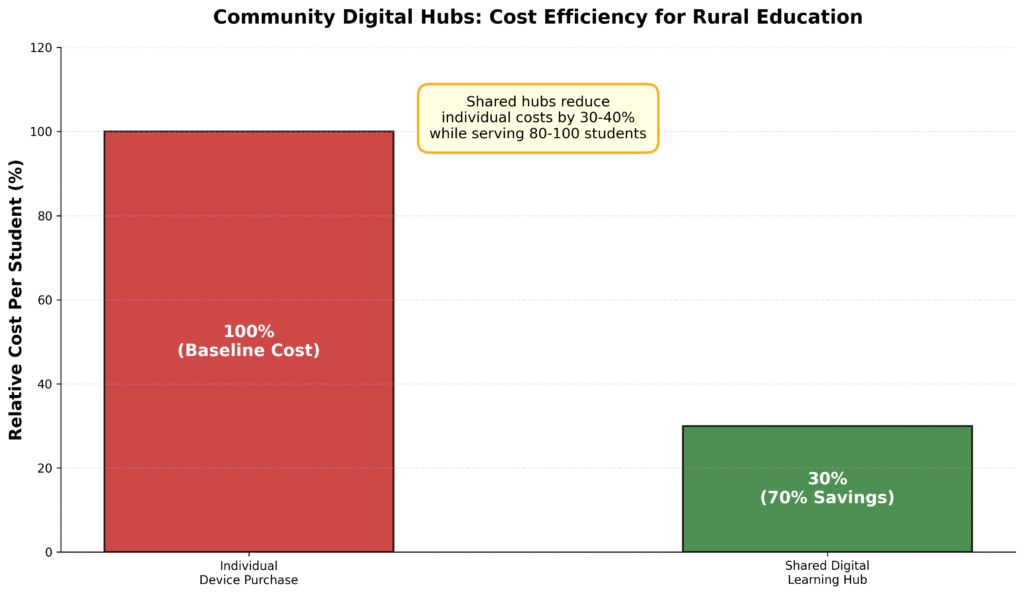

Community-based approaches offer the most practical path forward when we pool our resources effectively. Villages can establish shared digital learning hubs, where 80-100 students access computers and internet connections that individual families cannot afford. Local businesses or cooperative banks can sponsor basic computer labs in community centers, while bulk purchasing of tablets reduces individual costs by 30-40%. These hubs become centers of digital transformation, where one internet connection serves entire neighborhoods.

Figure 4: Financial advantage of shared digital learning hubs showing 70% cost savings compared to individual device purchases while serving 80-100 students

Training local youth as digital literacy instructors creates sustainable programs that do not depend on external volunteers. These young teachers often understand the specific challenges their communities face and can design relevant, practical training programs. Some communities link digital skills to immediate income opportunities—teaching basic graphic design, data entry, or online marketplace management—making technology education financially viable for families who cannot afford to wait years for returns on their investment.

Mobile technology penetration offers another pathway for reaching rural areas cost-effectively. Most rural families own at least one smartphone, which can serve as a gateway to online learning resources. Educational apps designed for low-bandwidth environments, pre-downloaded video content, and community viewing sessions can democratize access to quality instruction without requiring expensive infrastructure investments in every village.

(Read – Student Loan Debt in India: Education Crisis or Investment?)

Women’s Empowerment Through Literacy: Breaking Generational Cycles

Women’s empowerment through literacy creates the strongest foundation for breaking generational cycles of educational disadvantage. Many families find themselves trapped in poverty partly because mothers cannot read government documents or help children with homework. Self Help Groups already operate in thousands of villages across India, and we can integrate basic literacy training with their existing income-generating activities. When women learn to read and write while developing skills like tailoring or food processing, education becomes immediately practical rather than abstract. Evening and weekend classes accommodate the reality that women often work longer hours than men, managing households alongside agricultural or domestic labor.

Consider how financial incentives make women’s literacy programs sustainable for families who depend on every adult’s economic contribution. We can link literacy completion to microfinance opportunities, enabling women to access small business loans once they can read loan documents and maintain basic records. Government schemes often require literate applicants, so literacy training directly connects to benefits like housing subsidies or skill development programs. Peer-to-peer learning models work particularly well, where literate women teach others in exchange for small stipends, creating local employment while spreading knowledge.

Implementation Timeline and Community Impact

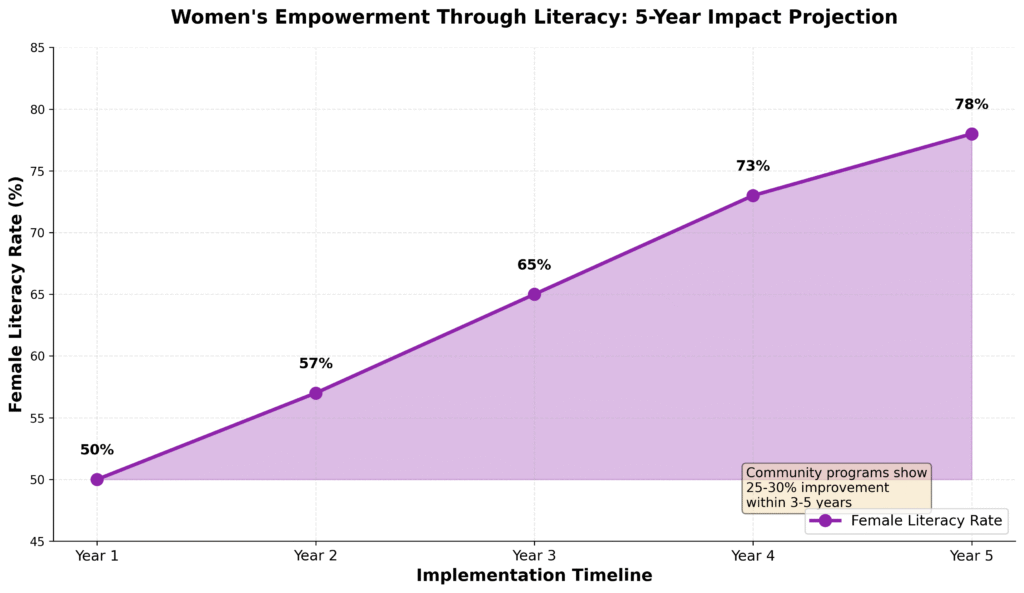

Most of us understand that childcare support during literacy sessions removes one of the biggest practical barriers that prevent women from attending classes. Community volunteers, often older children or retired residents, can supervise younger children while mothers learn. This creates a cycle where educated women later become literacy volunteers themselves, expanding the program’s reach without requiring external funding. Villages that implement these programs typically see female literacy rates increase by 25-30% within three to five years.

Figure 5: Five-year projection showing how community-based women’s literacy programs achieve 25-30% improvement in female literacy rates

Understanding the unique needs of rural communities proves crucial for closing the urban-rural literacy gap. Men might need different approaches than women, and elderly adults require different strategies than young parents. Successful programs adapt to local schedules, cultural practices, and economic realities rather than imposing uniform solutions. When literacy connects directly to improved income or better access to services, families prioritize education even during financially difficult periods.

Connecting Education to Economic Mobility

Think about how these community-based solutions work because they build on existing social structures rather than creating entirely new systems. Villages already have informal networks, leadership structures, and collective decision-making processes that can support education initiatives. We find that connecting literacy and digital skills to immediate, tangible benefits that families can see and measure makes all the difference. When education becomes a pathway to better livelihoods rather than an abstract goal, rural communities invest their limited resources more willingly in learning opportunities.

Figure 6: Stark contrast showing urban households spend 9 times more on education than rural households, highlighting the educational infrastructure gap

(Read – Low Savings Rate in India: 65% Save Under 20% of Income)

Moving Forward: Practical Steps to Bridge the Urban-Rural Literacy Divide

The path forward requires each of us to take concrete steps toward addressing the urban-rural literacy divide. We cannot wait for perfect solutions or comprehensive government programs to emerge. Small actions today create meaningful change tomorrow. Urban professionals can volunteer weekends to teach digital skills in nearby villages, while rural communities can organize evening literacy circles using existing community centers and resources. Technology becomes our most powerful ally in making these efforts more effective and accessible.

Consider the role of technology in bridging gaps when used thoughtfully. A smartphone with educational apps costs less than traditional textbooks and reaches multiple family members. Rural youth who gain basic digital literacy often become teachers for their parents and grandparents, creating knowledge transfer that strengthens entire households. Urban families can sponsor internet connectivity for rural schools or donate devices that still function well but are no longer needed.

Financial institutions and employers play significant roles in this transformation. Banks can design savings products that reward families for investing in education, while companies can create remote work opportunities that make rural areas more economically viable. When rural communities see direct economic benefits from literacy and digital skills, they prioritize education investments even during difficult financial periods.

Most importantly, we must recognize that closing the urban-rural literacy divide benefits everyone. Rural areas with higher literacy rates become stronger markets for urban businesses, while educated rural populations contribute innovations in agriculture, traditional crafts, and local services. The economic growth that emerges from widespread literacy creates opportunities across all sectors of society.

Start with one small step this month. Whether you volunteer time, donate resources, or simply spread awareness about rural education needs, your contribution matters. Every person who gains literacy skills becomes a teacher for others in their community. The urban-rural literacy divide that seems overwhelming today becomes manageable when millions of us take individual action toward collective progress.

(Read – Low Inflation in India: Weak Demand Drives CPI to Historic Lows)

FAQs

Q: How can parents in rural areas access quality education for their children without relocating?

Look for government digital literacy programs, online learning platforms with offline capabilities, and community learning centers. Partner with other families to share resources and advocate for better local infrastructure.

Q: What role can technology play in reducing educational inequality between urban and rural areas?

Technology can democratize access to quality teachers, learning materials, and skill development opportunities. Mobile learning apps, satellite internet, and digital libraries can bring world-class education to remote locations.

Q: How can rural communities sustain educational improvements without continuous external funding?

Focus on training local residents as educators and technology facilitators. Develop income-generating skills like the web design example, creating a cycle where education leads to economic growth that funds further educational development.

External Sources

- Ministry of Education, Government of India – Education Statistics

- National Statistical Office – Household Social Consumption on Education Survey

- UNICEF India – Digital Learning and Skills Report 2023

- Brookings Institution – Rural Education in Developing Countries Research

About the Author: Chitransh Saxena

Chitransh Saxena is the Founder of MoneyHum and a behavioural finance specialist with over seven years of experience in global financial markets, psychology-driven money systems, and low-risk investing frameworks. His work blends data, decision science, and financial clarity to help readers build calm, reliable wealth habits.

Learn more at the full profile: moneyhum.com/about-us/

Disclaimer: This article is for educational and informational purposes only. It is not financial advice. Consult a licensed financial advisor for personalised recommendations.

Disclosure: While the core content and ideas are human, tools were utilised for research and editing.