Author’s Note

As I write this, I can’t help but think about the countless conversations I’ve had with friends and readers who’ve found themselves in similar situations to our marketing professional from Bangalore. What strikes me most about India’s current financial landscape is how quietly the household debt to GDP ratio has climbed from 26% to nearly 43% in less than a decade. This isn’t just a statistical shift – it represents millions of families making increasingly difficult choices between their immediate needs and long-term financial security. Having analyzed financial trends for years, I’ve noticed that we’re not just dealing with numbers on a spreadsheet, but real stories of people trying to bridge the gap between their aspirations and their income reality. This chapter aims to help us understand not just what’s happening, but why it matters for every household in India.

Key Takeaways

- Take immediate action to audit your current debt situation – list all credit cards, personal loans, and monthly obligations to understand your true financial position before it becomes unmanageable

- Monitor how the rising household debt to GDP ratio affects lending policies and interest rates, as banks may tighten credit access when systemic debt levels become concerning

- Recognize that with India’s per capita income at $2,481, any debt exceeding 30% of your monthly income requires immediate restructuring to prevent the consumption debt trap

- Create an emergency fund equivalent to three months of expenses to avoid using credit cards for unexpected costs, breaking the cycle of borrowing for survival rather than growth

Understanding Medical Inflation in India’s Current Crisis

Most of us have experienced that moment of panic when we realize we have swiped our credit card one too many times. A marketing professional in Bangalore knows this feeling intimately. She started using her credit card for small expenses – a coffee here, groceries there. When her company delayed salary payments for two months during a restructuring, those small swipes became a lifeline. What began as ₹15,000 in credit card debt snowballed to ₹2.8 lakhs within eighteen months. The minimum payment that once seemed manageable at ₹3,000 became an impossible ₹25,000 monthly burden. She found herself taking cash advances from one card to pay another, trapped in a cycle that consumed 60% of her income just in interest payments.

This personal struggle is a microcosm of a larger issue affecting many in our society. We are witnessing a significant increase in household debt that has pushed our household debt to GDP ratio from 26% in 2015 to a significant 42.9% by June 2024. This rapid escalation represents one of the fastest debt accumulations in our economic history, with the Reserve Bank of India noting that household debt now stands well above the five-year average of 38.3%.

What makes this situation particularly concerning is the composition of this debt. Unlike previous decades when household borrowing was primarily for home purchases, today 55% of household debt comes from non-housing retail loans, including personal loans and credit card dues. We are essentially borrowing to fund consumption rather than assets, creating a dangerous pattern where families struggle to service debt without building wealth.

The numbers paint a sobering picture of how quickly financial stress can compound. With India’s GDP per capita at just $2,481 in 2023, many households find themselves caught between rising aspirations and limited income growth. Credit cards and personal loans, marketed as convenient solutions, often become debt traps that consume an ever-growing portion of family budgets.

Understanding why we have reached this point is crucial for charting a path forward. The need to explore how we can navigate back to financial stability has never been more critical, requiring not just individual awareness but systemic changes in how we approach credit, consumption, and financial planning as a society.

Health Insurance Premium Increase in India: The Borrowing Trap

When Medical Costs Force Families to Pledge Their Gold

Most of us can relate to that sinking feeling when monthly expenses outpace income growth. A school teacher watched this exact scenario unfold as her monthly expenses climbed while her salary remained frozen for three years. Vegetables that cost ₹80 per kg now demanded ₹140, her daughter’s school fees doubled, but her ₹35,000 salary stayed unchanged. Desperate to maintain her family’s lifestyle, she pledged her wedding jewelry – 50 grams of gold inherited from her mother – for a ₹1.5 lakh loan. The 12% interest seemed reasonable compared to credit card rates, but six months later, she realized she was paying ₹18,000 annually just to afford basic necessities that her salary once easily covered.

Her story reflects a broader crisis affecting millions of Indian families. We are witnessing families mortgage their most precious possessions not for business ventures or home purchases, but simply to maintain their standard of living. When wedding gold – passed down through generations and considered sacred in Indian culture – becomes collateral for grocery bills, it indicates a significant issue in our economic equation.

The numbers behind this emotional reality are equally troubling. India’s household debt to GDP ratio has surged from 26% in 2015 to 42.9% by June 2024, representing one of the fastest debt accumulations in our economic history. What makes this particularly dangerous is that 55% of this debt comes from non-housing retail loans, including personal loans and credit card debt. We are essentially borrowing to fund consumption rather than building assets, creating a cycle where families service debt without accumulating wealth.

Considering income levels reveals the depth of this crisis. With India’s GDP per capita at just $2,481 in 2023, many households find themselves trapped between rising aspirations and stagnant wages. Credit cards and personal loans, aggressively marketed as convenient solutions, transform into debt traps that consume an ever-growing portion of family budgets. The teacher’s ₹18,000 annual interest payment represents more than half her monthly salary, illustrating how quickly borrowing for essentials can spiral into unsustainable debt burdens.

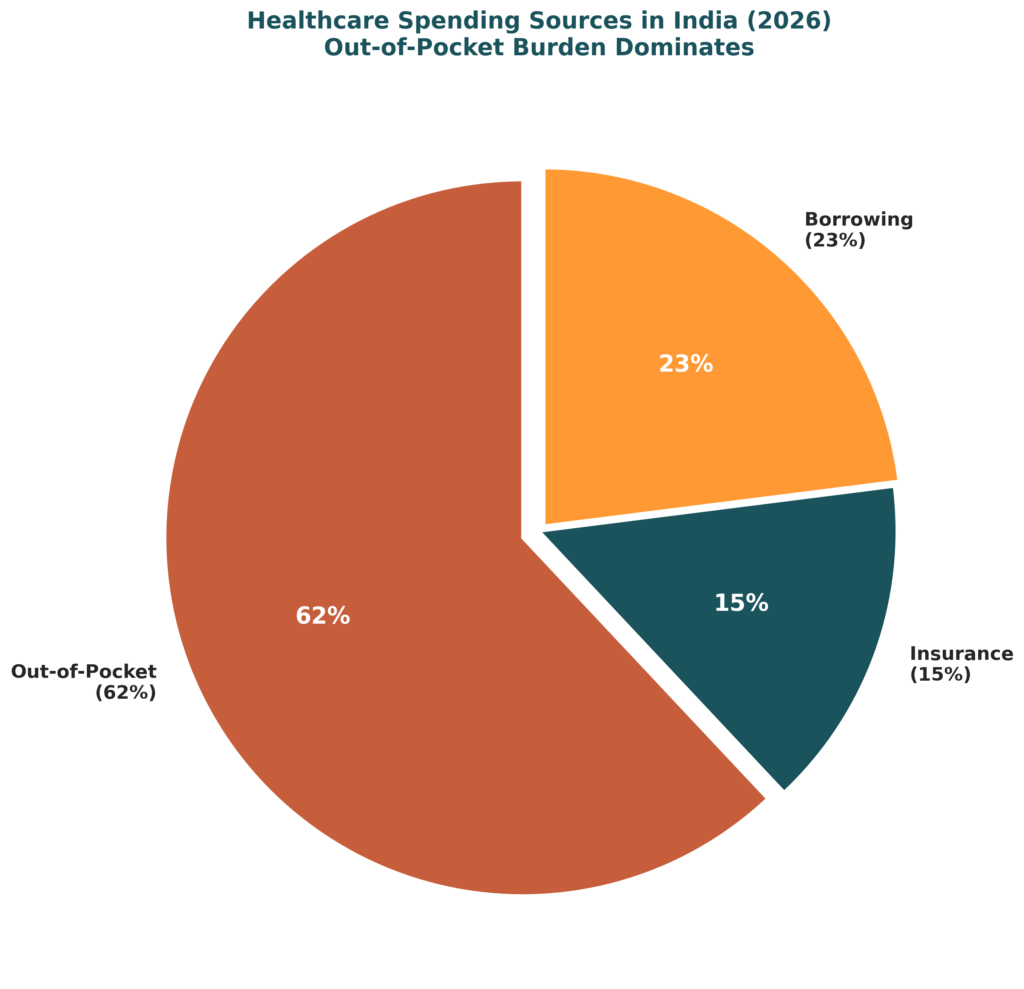

Rising Medical Insurance Cost and the 62% Out-of-Pocket Crisis

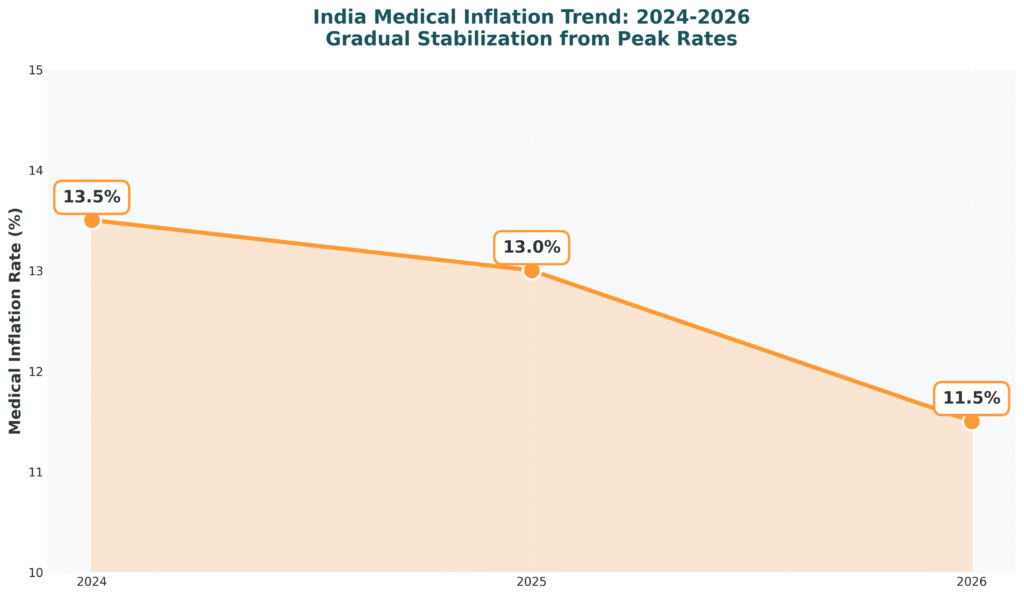

The fundamental problem extends beyond credit card interest rates. India faces a structural healthcare financing crisis where 62% of medical expenses come directly from family savings, forcing millions into debt when health emergencies strike. Insurance penetration remains critically low despite government initiatives, leaving most families financially vulnerable to medical inflation that compounds at 11.5-13% annually.

This creates a devastating cycle that our Bangalore professional and the school teacher both experienced. When health emergencies arise – and they inevitably do – families lacking adequate insurance coverage must choose between depleting savings accumulated over years or taking high-interest loans. A single hospitalization for cardiac treatment can easily cost ₹3-5 lakhs, consuming entire emergency funds and forcing families into the same debt spiral that started with small credit card purchases.

The psychological weight of this financial pressure manifests in delayed medical care, with families often postponing necessary treatments hoping conditions will improve on their own. This medical neglect frequently results in more severe health issues requiring even more expensive interventions later, perpetuating the exact financial crisis families tried to avoid. The intersection of inadequate insurance coverage, high medical inflation, and low income levels creates what financial experts call a “poverty trap” – where families cannot earn enough to build protective buffers against shocks that regularly push them deeper into debt.

Escaping this trap demands both immediate action and strategic planning that we can all implement. We must first track every expense for thirty days to understand where money actually flows, then create bare-bones budgets covering only absolute necessities. The goal shifts from managing existing debt to stopping new borrowing entirely. This often requires developing additional income streams—freelancing, tutoring, online sales, or part-time work—while building micro-emergency funds of ₹5,000-10,000 before attempting debt reduction.

The emotional toll of borrowing for necessities extends beyond financial stress and affects our dignity as individuals and families. We experience shame, desperation, and loss of self-worth when forced to seek credit for basic needs. Recovery requires recognizing that this situation often results from systemic economic pressures rather than personal failures. When we implement survival budgeting with income diversification consistently, we can stop the borrowing cycle within six months and generate additional monthly income of ₹5,000-15,000, providing the foundation for genuine financial recovery.

GST on Health Insurance and Breaking the Debt Cycle

Health Insurance Premium in 2026: Strategic Debt Reduction Planning

Most of us facing overwhelming debt need a systematic approach rather than wishful thinking. The 50-30-20 Debt Reduction Plan offers a practical framework that adapts to our Indian financial reality. We begin by calculating our total debt-to-income ratio and listing every debt with its interest rate. This reveals the true scope of our situation and helps prioritize which debts demand immediate attention. The key modification for debt-heavy households involves temporarily redirecting the traditional 20% savings allocation toward debt repayment while maintaining 50% for needs and 30% for reasonable wants.

The debt avalanche method proves most effective for reducing overall interest payments. We pay minimum amounts on all debts, then channel every extra rupee toward the highest interest rate obligation first. Credit card debt typically carries 36-42% annual interest, making it our primary target. Personal loans at 12-18% come next, followed by home loans with their relatively lower rates. This mathematical approach saves thousands in interest payments compared to paying debts equally or focusing on smallest balances first.

Beyond strategic repayment methods, engaging with our lenders directly can provide significant relief. Negotiating with lenders often yields surprising results that many of us never attempt. Banks frequently agree to extend loan tenure for lower EMIs or reduce interest rates for customers showing genuine repayment intent. We should contact each lender explaining our situation honestly and requesting modified payment terms. Document these conversations and get any agreements in writing. For those qualifying, debt consolidation loans at lower interest rates can transform multiple high-interest obligations into a single, manageable payment.

Income diversification can be beneficial when our primary salary cannot cover both living expenses and debt obligations. The digital economy offers numerous opportunities for additional earnings through freelancing platforms, online tutoring, e-commerce, or skill-based services. Even an extra ₹5,000-10,000 monthly makes substantial difference in debt repayment timelines. The crucial discipline here involves channeling this additional income directly toward debt reduction rather than allowing lifestyle improvements to consume these extra earnings, which maintains our focus on genuine financial recovery.

Building even a small emergency buffer prevents us from adding new debt during unexpected expenses. Starting with just ₹100 weekly automatic transfers to a separate account creates the savings habit without overwhelming our already tight budgets. This micro-emergency fund of ₹5,000-10,000 acts as a crucial circuit breaker, stopping the cycle of borrowing for minor crises. The psychological impact of having any emergency savings often motivates continued progress and helps us resist the temptation to use credit for non-essential purchases.

The reality of India’s rising household debt to GDP ratio means we are not alone in these struggles, but individual action remains our most powerful tool. Recovery timelines vary based on debt levels and income, but most people see significant improvement within 6-12 months of implementing these strategies consistently. Success requires treating debt reduction as a temporary lifestyle adjustment rather than permanent deprivation. Once we establish sustainable repayment schedules and break the borrowing cycle, we can gradually restore normal spending while maintaining the emergency fund habits that prevent future debt accumulation.

Medical Inflation in India: Moving Toward Financial Security

The path forward begins with a single decision today. With household debt to GDP climbing to 42.9% by June 2024, millions of Indian families share these financial pressures, but we must chart our own recovery course. The strategies we have discussed work best when implemented gradually, allowing us to build momentum without overwhelming our daily routines. Starting with debt prioritization this week, then adding the envelope method next month, creates sustainable progress that compounds over time.

Small steps produce remarkable results when maintained consistently. Setting up automatic transfers of just ₹500 monthly to debt repayment or emergency savings begins the transformation immediately. Tracking expenses for one week reveals spending patterns that seemed invisible before, often uncovering ₹1,000-2,000 in redirectable monthly expenses. These micro-changes feel manageable while creating the foundation for larger financial shifts as our confidence and skills develop.

Making these personal adjustments becomes easier when we recognize that external conditions favor our debt reduction efforts. The current economic environment actually supports our goals through increased awareness and available resources. Banks offer restructuring options more readily now, digital tools make expense tracking effortless, and the growing financial literacy movement provides support systems our parents never had. Taking advantage of these resources while implementing personal debt strategies accelerates recovery timelines significantly.

Most families see meaningful progress within three to four months of consistent application. The psychological shift happens even sooner, as taking control of finances reduces stress and improves decision-making across all areas of life. The key lies in treating this as a temporary adjustment period rather than permanent restriction, knowing that establishing these habits now prevents future debt accumulation.

Our financial freedom starts with today’s choices. Whether we begin by listing all debts, setting up one automatic transfer, or simply tracking expenses for this week, the important step is starting. The rising household debt to GDP trend affects millions, but our individual action breaks the cycle for our families and creates the foundation for long-term financial security.

FAQs

Q: How do I know if my debt level is dangerous compared to the national average?

If your total monthly debt payments exceed 40% of your income, you’re in the high-risk category. With household debt rising faster than income growth, maintaining payments below 30% of monthly income provides a safer buffer against financial stress.

Q: Should I be worried about taking a personal loan if the entire country’s debt is increasing?

Personal loans should only be considered for asset creation or emergencies, never for consumption. Rising national debt levels mean lenders may tighten criteria and increase rates, making future borrowing more expensive and difficult to obtain.

Q: What happens if I can only make minimum payments on my credit cards?

Minimum payments typically cover only interest and fees, meaning your principal debt rarely decreases. This creates the same trap our Bangalore professional faced – eventually leading to a debt spiral where interest payments consume most of your income.