Author’s Note

As I researched this piece on India’s escalating debt crisis, I kept thinking about my own early experiences with credit. Like many of us, I was drawn to the convenience of instant purchases and manageable monthly payments. But watching credit card delinquencies surge by 44% in just one year made me realize how this convenience culture is quietly reshaping our financial landscape. The stories I encountered while writing this article – from young professionals drowning in EMIs to families struggling with multiple payment deadlines – reminded me that behind every statistic is a real person grappling with choices that seemed reasonable at the time but became overwhelming in reality.

Key Takeaways

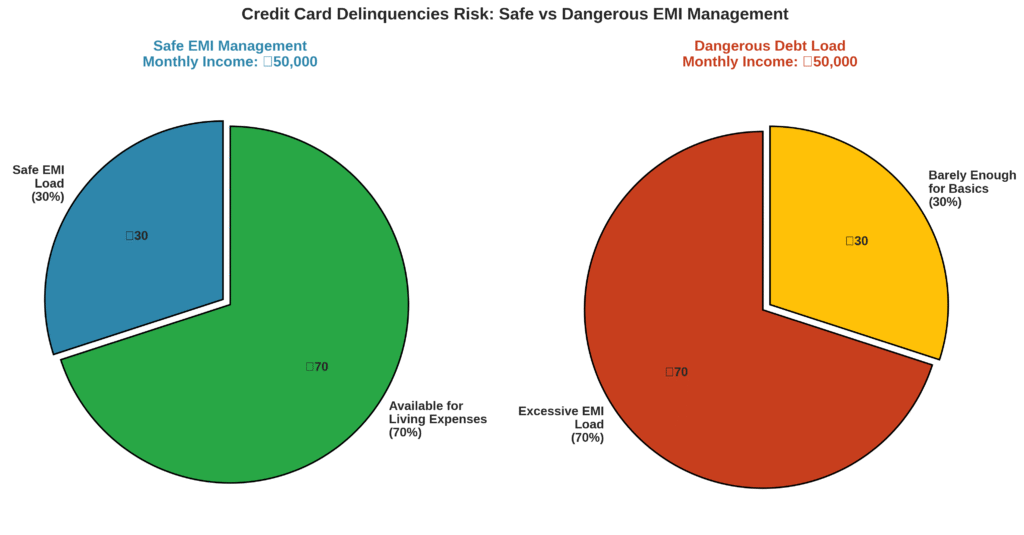

- Track all your EMI commitments in one place and ensure total monthly obligations don’t exceed 30% of your income to avoid payment stress

- Monitor credit card delinquencies by setting up automatic minimum payment transfers to prevent falling into the dangerous 91-180 day overdue category

- Understand that credit card defaults have jumped 28% because people underestimate how small EMIs accumulate into unmanageable debt loads

- Create a debt consolidation plan if you’re juggling multiple payment apps, focusing on clearing high-interest obligations first while maintaining minimum payments on others

The notification sounds seemed harmless enough at first. A young professional believed it was smart to split purchases into affordable EMIs. A laptop here, a vacation there, some trendy clothes – each purchase felt manageable at ₹2,000-3,000 per month. But when the phone buzzed with payment reminders from six different apps simultaneously, reality hit hard. Juggling ₹18,000 in monthly EMI payments on a ₹45,000 salary left little room for even basic credit card bills. Three defaults later, the realization came that buy now, pay later had become buy now, manage later.

Most of us have felt that same temptation. The allure of splitting a ₹20,000 purchase into just ₹2,000 per month feels almost too good to pass up. What we often miss is how quickly these small commitments add up, creating a web of obligations that can strangle our finances.

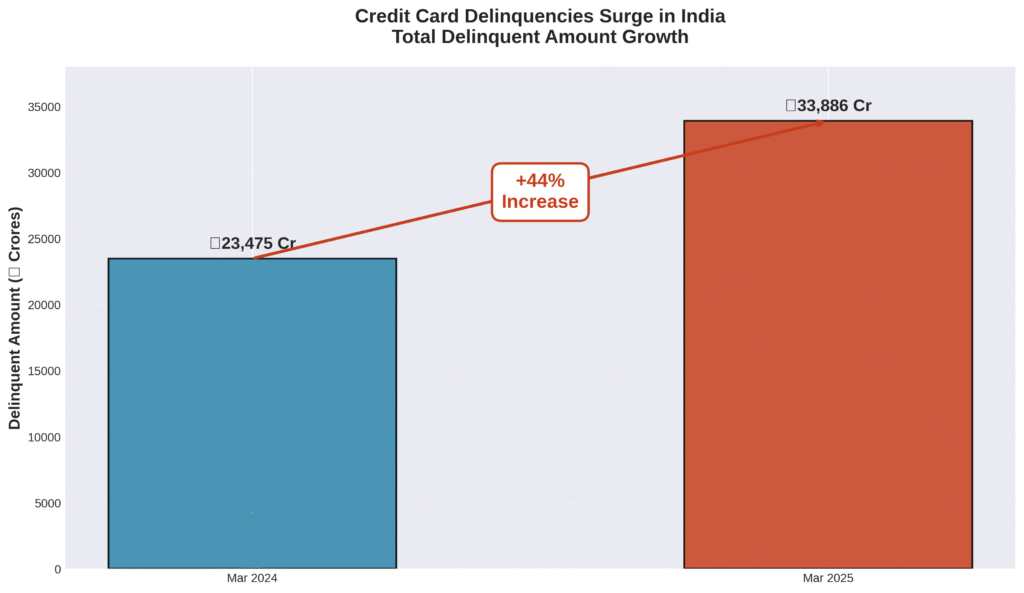

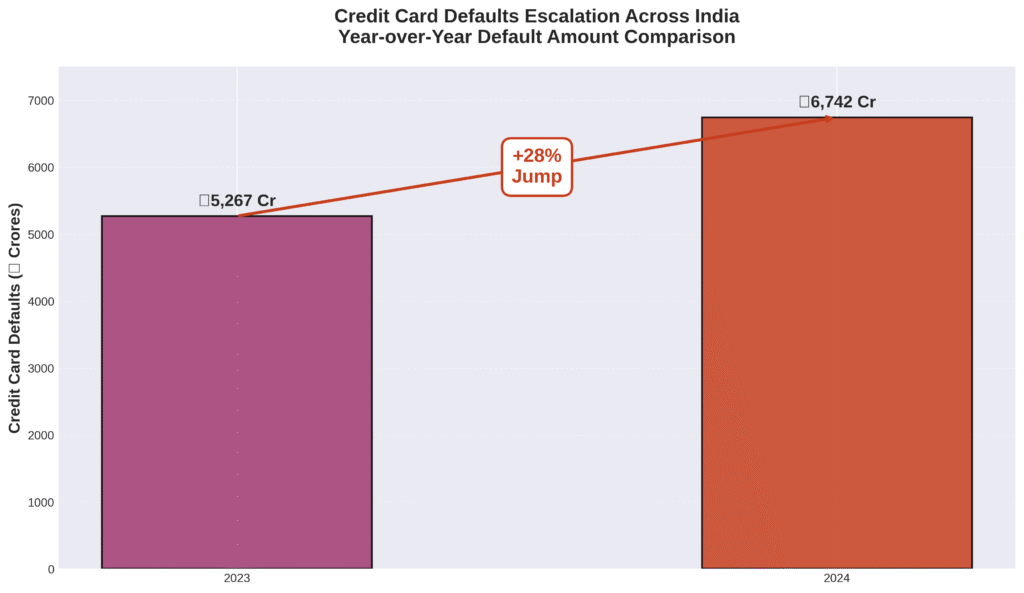

The numbers paint a sobering picture of where this mindset is leading us. Credit card delinquencies have surged to significant levels, with the total delinquent amount reaching ₹33,886 crore by March 2025 – a 44% increase from the previous year. Credit card defaults alone jumped 28% in 2024 to ₹6,742 crore, signaling that millions of Indians are struggling to keep up with their plastic money commitments.

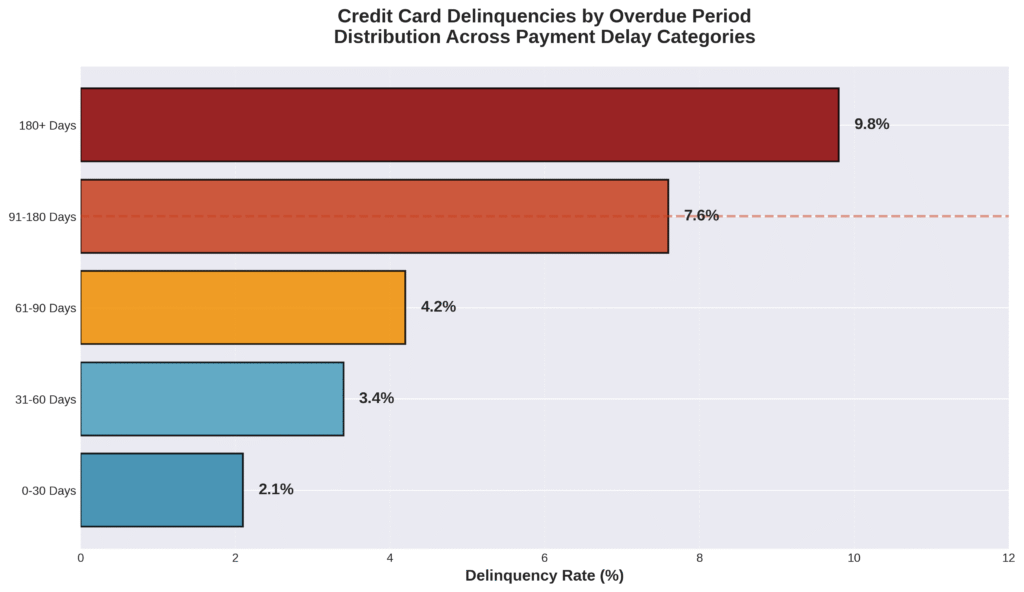

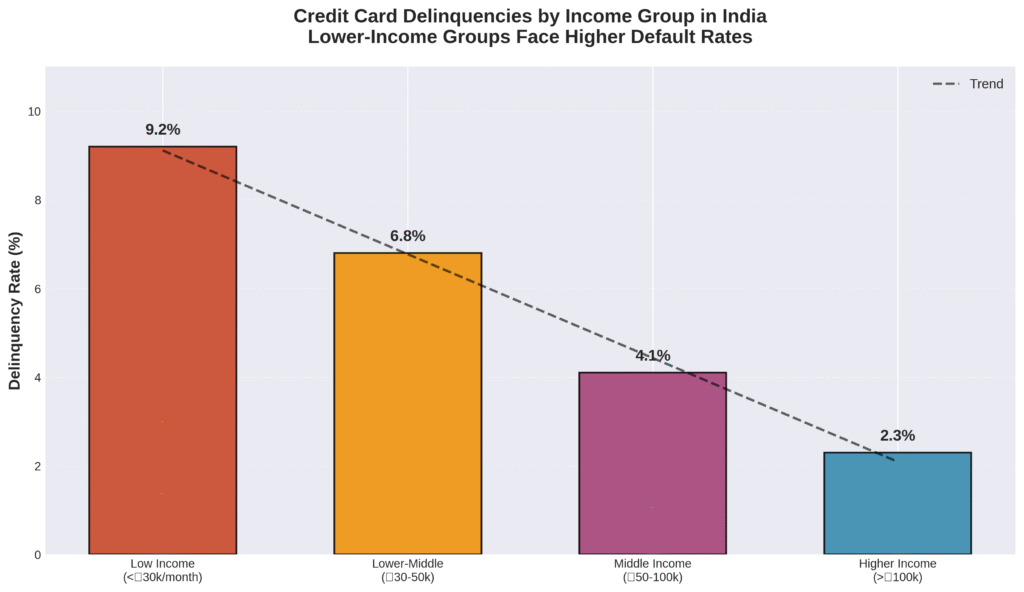

This crisis extends far beyond individual financial mistakes. When we look at the broader pattern, delinquencies in the 91-180 days overdue category have risen to 7.6%, indicating that we are not just missing one payment but falling into prolonged cycles of debt. The problem hits hardest among lower-income groups, where household debt pressures have intensified significantly.

We are witnessing a fundamental shift in how Indians manage money, and the consequences are becoming impossible to ignore. The ease of digital lending and the psychology of small EMIs have created a perfect storm that is pushing ordinary people into extraordinary financial distress. Understanding why this is happening and how to protect ourselves has never been more critical.

Understanding Credit Card Delinquencies: When Convenience Becomes Crisis

How Credit Cards Become Financial Quicksand

Most of us remember our first credit card approval email. That moment of pride, feeling like we had finally made it into the adult world of financial responsibility. What we rarely anticipate is how quickly that plastic rectangle can transform from a tool of convenience into a source of significant stress.

A software engineer from Hyderabad thought she was managing her finances perfectly. Three credit cards, each with reasonable limits, used for everything from groceries to online shopping. The monthly statements felt manageable until life threw her a curveball – a family medical emergency that required immediate funds. Within six months, her balances had spiraled to ₹1.5 lakh across all three cards. The minimum payments alone consumed 40% of her take-home salary, and her CIBIL score plummeted to 520. She felt a deep sense of disappointment when loan applications got rejected and even her phone’s EMI was declined at the store.

Her story reflects a nationwide crisis that most Indians are not fully grasping. The total delinquent amount has reached ₹33,886 crore by March 2025, representing a significant 44% increase from the previous year. This surge in credit card delinquencies signals that millions of us are falling behind on our payments, trapped in cycles we never saw coming. Consider the concerning rise in delinquencies in the 91-180 days overdue category, now at 7.6%, meaning people are not just missing one payment but struggling for months.

The problem hits hardest among those who can least afford it. Lower-income borrowers are experiencing delinquency rates that have surpassed pre-pandemic levels, while their higher-income counterparts show relatively stable payment patterns. This disparity highlights how financial literacy gaps leave vulnerable populations exposed to predatory lending practices and unrealistic debt burdens. Credit card defaults jumped 28% in 2024 to ₹6,742 crore, proving that what starts as manageable monthly payments can quickly snowball into unmanageable debt loads.

The Psychology Behind Rising Credit Card Defaults

What makes this crisis particularly dangerous is how normalized excessive credit card usage has become. Many of us witness friends booking vacations on credit, colleagues buying gadgets through EMIs, and family members treating credit limits like additional income. The psychological trap is real – when minimum payments seem affordable, we lose sight of the total debt accumulating in the background. By the time reality hits, many people find themselves drowning in interest charges that can take years to overcome, even with disciplined repayment efforts.

The Missed Payment Spiral: Credit Card Delinquencies Patterns

How Small Delays Become Major Credit Card Defaults

Most of us start with good intentions when we get our first credit card. We promise ourselves we will pay the full amount each month, treat it like cash, and never carry a balance. Yet a recent analysis of credit bureau data revealed something significant. Defaults on credit cards overdue for 3-12 months had jumped by 44% in just one year. Behind this statistic were thousands of young professionals who had started with small delays, thinking they would catch up next month. But next month brought new expenses, new EMIs, new reasons to delay. What began as a temporary cash crunch became a spiral of minimum payments, late fees, and mounting interest.

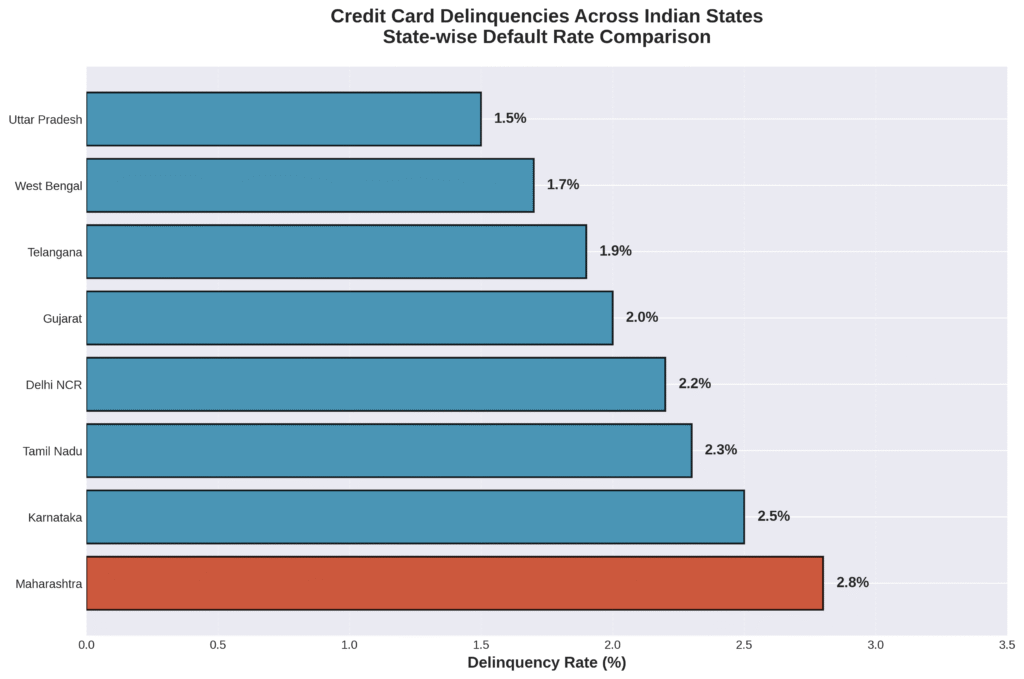

The numbers tell a story of widespread financial distress that goes far beyond individual poor choices. The total delinquent amount reached ₹33,886 crore by March 2025, representing a substantial 44% increase from ₹23,475 crore just one year earlier. This surge affects credit card users across all income segments, though the impact concentrates heavily among those who can least afford the consequences. When we examine state-wise data, Maharashtra leads with the highest delinquency rate at 2.8%, followed by other metropolitan areas where credit card penetration runs deepest. These numbers translate into real-life struggles for many individuals.

The Emotional Toll of Credit Card Delinquencies

Behind every missed payment lies a human story of shame, embarrassment, and mounting fear. The emotional toll of falling behind on credit card payments extends far beyond the financial mathematics of interest and penalties. We often describe constant worry about damaged credit scores, sleepless nights calculating minimum payments, and the growing dread of opening monthly statements. The fear of financial ruin becomes a daily companion, affecting relationships, career decisions, and mental health in ways that compound the original problem.

The pattern typically unfolds in predictable stages that many of us recognize. Someone misses a payment due to an unexpected expense or temporary cash flow issue. They assume they can catch up next month, but the late fee and interest charges make the balance higher than expected. Meanwhile, life continues with its regular expenses, leaving less room to make up the shortfall. Within three to six months, what started as a manageable delay becomes a persistent struggle that grows worse each billing cycle. These individual struggles reflect broader economic pressures that make recovery even more challenging.

Economic Pressures Driving Credit Card Defaults

What makes this crisis particularly insidious is how it intersects with broader economic pressures facing Indian households. Rising living costs, stagnant wages, and easy access to credit create perfect conditions for payment defaults. The low savings rate among Indian families means most people lack the buffer funds needed to handle temporary income disruptions or unexpected expenses. When credit cards become the primary safety net, missed payments become almost inevitable during financial stress periods.

Breaking Free: Practical Solutions to Credit Card Delinquencies

Immediate Steps to Stop the Debt Cycle

Once we have secured better terms or consolidated our debt, maintaining consistent payments becomes our next important task. Setting up automated payment systems eliminates the human error factor that causes most missed payments. Configure automatic payments for at least the minimum amount on each card, scheduled five days before the due date to account for processing delays. Create a dedicated checking account solely for credit card payments and transfer money into it weekly rather than hoping we will remember monthly payments. Build a buffer fund of ₹5,000-10,000 in this account to handle unexpected timing issues or minor income fluctuations.

The reality is that many of us struggle with payment discipline because emergency savings simply do not exist in most households. This makes systematic automation even more critical for preventing the missed payment spiral that has driven credit card delinquencies to record levels across the country. Use calendar reminders to review upcoming payments weekly, treating this like any other essential appointment.

Strategic Debt Settlement for Credit Card Defaults

For those of us already facing overdue payments, immediate debt settlement becomes a necessary step to stop mounting penalties and legal action. Contact each bank to discuss settlement options, which typically range from 40-60% of the outstanding amount. Gather all available cash, including any emergency funds or family assistance, to make lump-sum settlement offers. Never agree to settlement terms verbally or make payments without written confirmation of the final settlement amount and account closure.

After settling overdue debts, focus on rebuilding your credit profile systematically. Apply for a secured credit card with small limit, make small purchases, and pay the full balance every month. Monitor your credit report monthly through free services to track improvement and dispute any incorrect entries. Most of us can rebuild our credit score by 100-150 points within 12-18 months of settling old debts, but this requires consistent payment discipline and avoiding new debt accumulation during the recovery period.

Moving Forward: Your Action Plan Against Credit Card Delinquencies

The path forward requires immediate action, not endless planning. Most of us already know what needs to be done, we simply need to begin today with one concrete step. Whether that means setting up automatic payments for next month, calling your bank to discuss settlement options, or downloading a budgeting app, the specific action matters less than taking it within the next 24 hours.

Small steps compound into life-changing results when we maintain consistency over months and years. A software engineer earning Rs 80,000 monthly who starts tracking expenses today will save Rs 15,000-20,000 more per year than someone who waits for the perfect budgeting system. We see families who escape the credit card delinquencies crisis are those who act immediately on basic financial disciplines, not those who research endlessly without implementing anything.

Building on this momentum means we should choose the simplest possible first step that fits our current situation. Set one automatic payment reminder on your phone, transfer Rs 1,000 to a separate savings account, or commit to reviewing your credit card statement every Sunday for the next month. These micro-habits create momentum that makes larger financial changes feel natural and achievable over time.

Our financial recovery begins the moment we decide that this cycle of stress and uncertainty ends today. Thousands of families across Maharashtra, Karnataka, and other states are successfully rebuilding their finances by focusing on consistent daily actions rather than waiting for major income increases or perfect market conditions. The tools, strategies, and support systems exist, what remains is our commitment to use them starting now.

Every month we delay action, the compound effect of poor financial habits grows stronger, while the compound power of good habits remains dormant. We can choose today to join the growing number of Indian families who have taken control of their financial destiny through disciplined action and financial literacy development, regardless of our starting point or past mistakes.

FAQs

Q: How many EMIs can I safely handle on my current salary? It is recommend keeping total EMI obligations under 30% of your monthly income. If you earn ₹50,000, limit all EMIs combined to ₹15,000 to maintain healthy cash flow for essentials and emergencies.

Q: What happens if I miss credit card payments for more than 90 days? After 90 days, your account enters serious delinquency territory. Banks typically report defaults to credit bureaus, impacting your credit score for years and making future loans expensive or impossible to obtain.

Q: Should I use another credit card to pay existing EMIs? This creates a dangerous debt spiral. Instead, contact your lenders to negotiate payment plans or consider debt consolidation loans with lower interest rates than credit cards, which typically charge 24-48% annually.

External Sources

- Reserve Bank of India Bankwise ATM/POS/Card Statistics

- National Sample Survey Office Household Debt Survey Data (PDF File)

- Credit Information Bureau (India) Limited Delinquency Analysis

- Ministry of Statistics Consumer Expenditure Survey Reports

About the Author: Chitransh Saxena

Chitransh Saxena is the Founder of MoneyHum and a behavioural finance specialist with over seven years of experience in global financial markets, psychology-driven money systems, and low-risk investing frameworks. His work blends data, decision science, and financial clarity to help readers build calm, reliable wealth habits.

Learn more at the full profile: moneyhum.com/about-us/

Disclaimer: This article is for educational and informational purposes only. It is not financial advice. Consult a licensed financial advisor for personalised recommendations.

Disclosure: While the core content and ideas are human, tools were utilised for research and editing.