Author’s Note

As I researched this article, I was struck by how many families I know personally who’ve found themselves caught in similar cycles. The story of the grandmother’s necklace resonated deeply because it reflects a pattern I’ve observed across different income groups – using what we value most as collateral for basic needs. When I learned that India’s household debt to GDP ratio has climbed to 41.3%, it confirmed what many of us already sense: borrowing has become less about building wealth and more about surviving monthly expenses. This shift concerns me because it suggests we’re moving away from debt as a tool for growth toward debt as a necessity for basic living. My hope is that by understanding these trends and their underlying causes, we can help families recognize warning signs early and build stronger financial foundations that don’t depend on constant borrowing.

Key Takeaways

- Start tracking your debt-to-income ratio monthly and set alerts when it exceeds 30% to prevent dangerous borrowing cycles before they begin

- India’s household debt to GDP ratio of 41.3% signals widespread financial stress, making it crucial to distinguish between productive debt and survival borrowing

- With per capita income at $2,481, families must prioritize building emergency funds equivalent to 3-6 months of expenses rather than relying on credit for unexpected costs

- Focus on breaking the cycle by consolidating high-interest debt first, then redirecting those monthly payments toward building genuine financial assets

Most of us have been there at some point – staring at our bank balance while calculating if we can stretch our budget until the next payday. But for a professional, that familiar anxiety turned into a more pressing concern. She found herself at 2 AM, holding her grandmother’s gold necklace and a calculator, trying to figure out how to pay her daughter’s school fees. What began as pawning the jewelry for ₹25,000 as a temporary solution became a cycle of borrowing, repaying, and borrowing again.

Six months into this cycle, she discovered she was paying ₹2,800 in interest every month – more than her grocery budget – just to keep retrieving and re-pawning the same precious family heirloom. Her story reflects a growing reality across Indian households, where families increasingly rely on borrowed money to meet everyday expenses and unexpected financial emergencies.

Understanding India’s Rising Household Debt Crisis

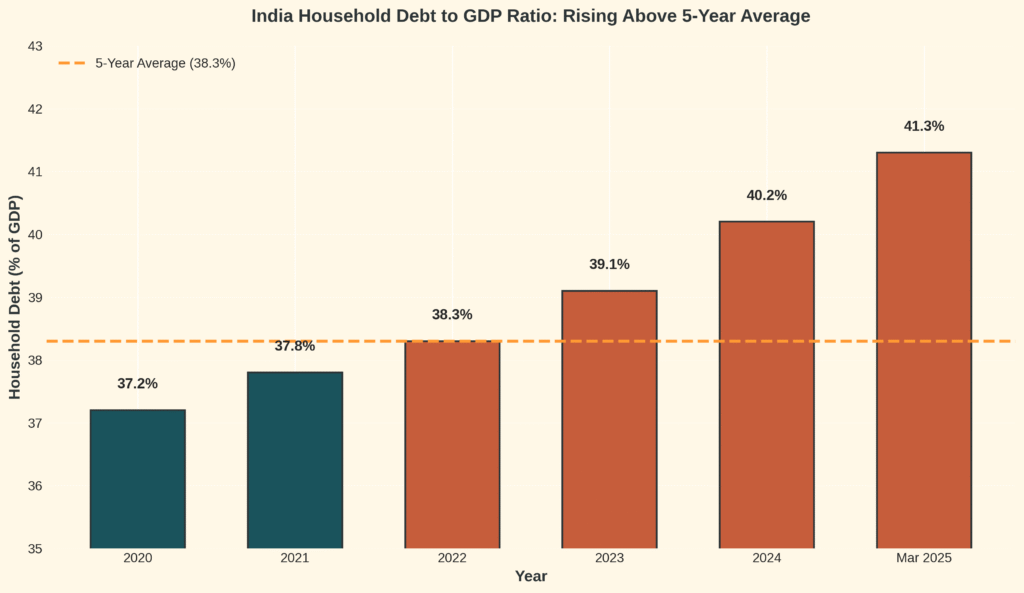

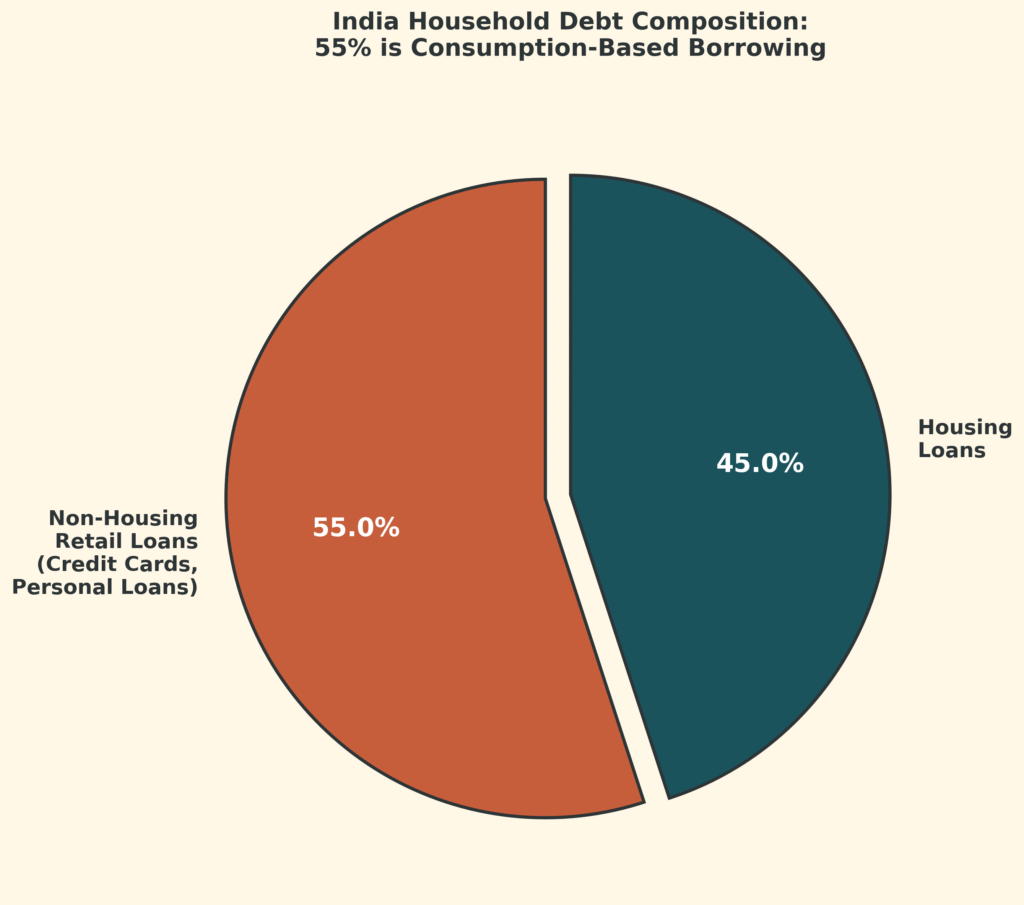

We are witnessing a significant shift in how Indian families manage their finances. Recent data shows that household debt rose to 41.3% of GDP at the end of March 2025, climbing above its five-year average of 38.3%. This household debt to GDP ratio reveals that families across the country are borrowing more than ever before, with non-housing retail loans – including credit card dues and personal loans – accounting for 55% of total household debt.

The numbers indicate a challenging situation when we consider that India’s per capita income in 2023 was $2,481, reflecting modest growth against rising borrowing levels. What makes this trend notable is how ordinary families are using debt not for wealth creation or investment, but simply to bridge gaps in their monthly cash flow.

Understanding why household debt continues climbing and how families can break free from expensive borrowing cycles has never been more critical. We need to examine the forces driving this trend and explore practical strategies that help families build financial resilience without compromising their long-term security.

When Debt Becomes Your Only Asset: The Consumption Trap

Most of us have experienced that moment when an unexpected expense forces us to reach for a credit card or consider a personal loan. The air conditioner breaks down in peak summer, a family member needs medical treatment, or a job opportunity requires immediate relocation. What starts as a temporary financial bridge often becomes a permanent burden that grows heavier each month.

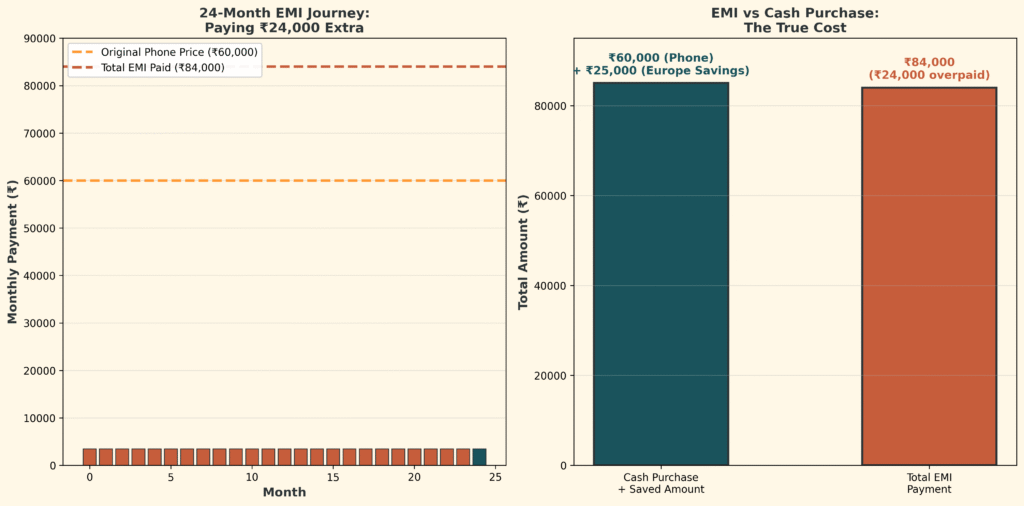

Consider a young professional who bought a smartphone on a 24-month installment plan. The salesperson made it sound reasonable – just ₹3,500 per month instead of ₹60,000 upfront. Two years later, after paying ₹84,000 total, they realized they could have bought the same phone with cash and still had ₹25,000 left for the Europe trip they kept postponing. The worst part was discovering their phone had already become two generations old, while they were still paying for it.

The Hidden Cost of Non-Housing Retail Loans

This story reflects a pattern we see across our households today. We are drowning in consumption debt with no productive assets to show for our borrowing. The household debt to GDP ratio climbing to 41.3% tells only part of the story – the real concern lies in how we use this debt. Non-housing retail loans, including credit card dues and personal loans, now account for 55% of total household debt. Unlike home loans that build equity, these consumption loans fund our lifestyle purchases, emergency expenses, and daily needs without creating any lasting value.

The emotional toll of this debt cycle cannot be understated. We find ourselves trapped in a pattern where monthly installment payments consume an increasing portion of our income, leaving little room for savings or investment. The anxiety of being unable to build wealth while servicing debt creates a stress that extends far beyond financial statements. Many of us discover we are working harder each year but moving further away from financial security.

Breaking the Consumption Debt Mindset

This shift toward consumption-based borrowing coincides with broader challenges in financial literacy, where we lack the knowledge to distinguish between good debt that builds assets and bad debt that only creates obligations. The result is households that appear financially active through their borrowing and spending, but remain fundamentally vulnerable because we own no appreciating assets.

The path forward requires recognizing that debt itself is not the enemy – how we use debt determines whether it becomes a tool for wealth creation or a trap that prevents financial progress. Breaking free from this cycle starts with understanding why consumption debt feels so accessible and learning practical strategies to redirect those same monthly payments toward building genuine assets.

When Basic Needs Become Borrowed Expenses: The Credit Card Trap

Most of us never intended to finance our groceries or children’s school fees through credit cards. This gradual shift from paying for essentials with earned income to borrowing for basic needs has become a concerning pattern in Indian household finances. What begins as a temporary solution during a difficult month transforms into a permanent dependency that keeps us trapped in debt cycles.

Consider a middle-class household that started using their credit card for weekly grocery shopping when business income faced a rough patch. It’s just groceries, we’ll pay it back next month, they reasoned. But next month brought school supplies, then festival expenses, then a medical emergency. Eighteen months later, they owed ₹1.2 lakhs on a card with a ₹50,000 limit, paying ₹8,000 monthly just in minimum payments while their actual grocery bill remained unpaid on the revolving balance.

Understanding Dangerous Debt-to-Income Ratios

This pattern reflects a broader crisis where low savings rates leave us without buffers for essential expenses. When 55% of household debt consists of non-housing retail loans including credit cards and personal loans, we see ourselves borrowing not to build assets but simply to survive month to month. The shame and desperation of being unable to afford basic needs without borrowing money creates an emotional burden that extends far beyond the financial cost.

The goal extends beyond mere budgeting to building genuine financial confidence through predictable expense management. When basic needs are funded through earned income rather than borrowed money, we can begin building emergency funds and exploring additional income sources without the constant pressure of mounting debt service obligations.

Breaking Free: Your Debt-to-Wealth Transformation Plan

Most of us have experienced the burden of debt and the desire for financial independence, yet we continue directing our income toward consumption debts that drain our wealth. We need to implement a debt-to-asset conversion strategy that transforms existing EMI payments into wealth-building investments. This approach acknowledges that most of us already have the cash flow capacity for investment – we are simply directing it toward the wrong places.

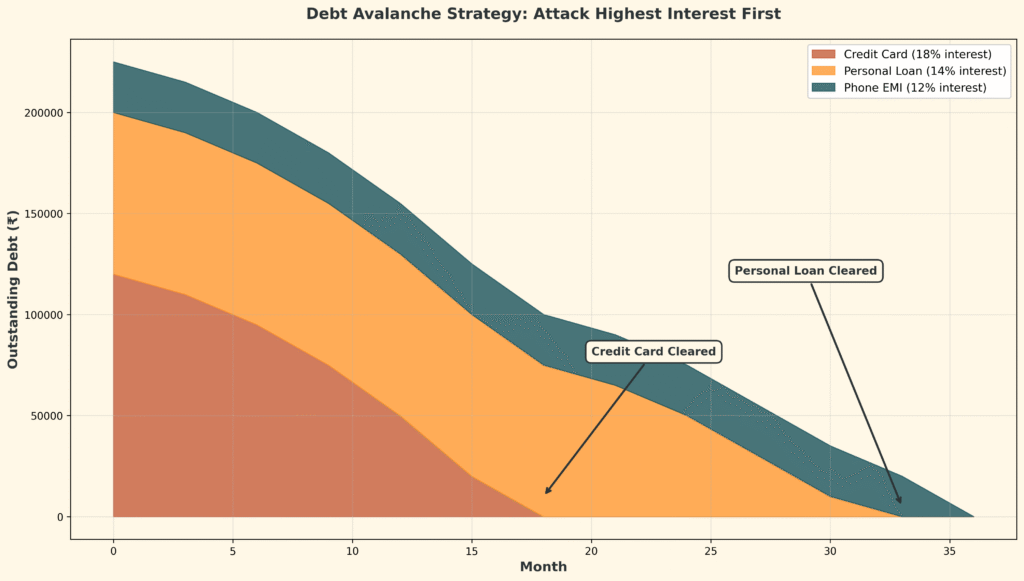

Step 1: Implement the Debt Avalanche Strategy

We should start by listing every consumption debt we currently carry, from credit cards to personal loans to electronics EMIs, along with their monthly payment amounts. Create a debt avalanche plan where we pay minimum amounts on all debts but direct any extra money toward the debt with the highest interest rate first. Once we eliminate one debt completely, we can redirect that entire EMI amount into a systematic investment plan in equity mutual funds. This strategy ensures that money previously lost to interest payments now works to build our asset base.

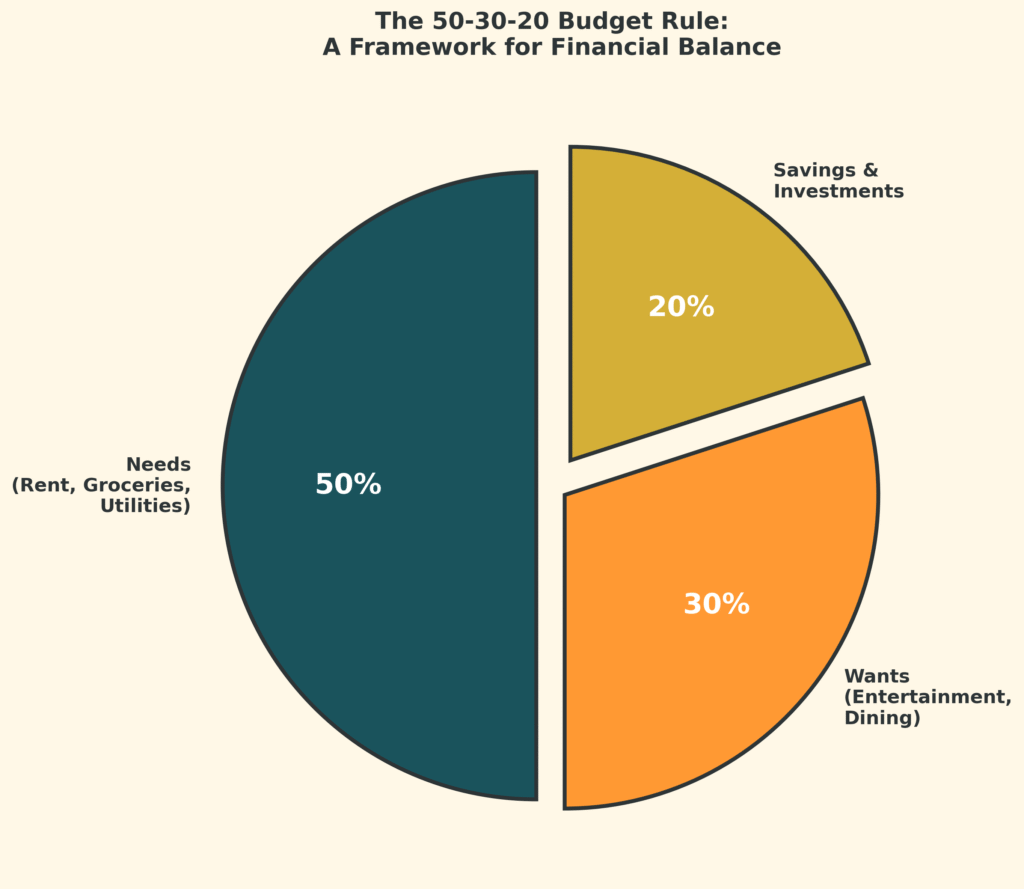

Step 2: Apply the 50-30-20 Budget Rule

Applying the 50-30-20 rule to new income allocation enhances our transformation: 50% for genuine needs, 30% for wants, and 20% for savings and investments. Any windfalls like bonuses, gifts, or salary increases should accelerate our debt payoff rather than fund new purchases. Within 6-12 months, we will see significant debt reduction momentum, and within 2-3 years, a substantial investment corpus will grow alongside our shrinking debt burden.

Step 3: Build a Basic Needs Buffer System

Breaking the cycle of borrowing for basic necessities requires us to establish what financial planners call a basic needs buffer system. We should track our personal expenses for one complete month to understand our spending habits, then create a separate bank account dedicated exclusively to rent, groceries, utilities, and school fees. Set up an automatic transfer of 60% of our income to this account immediately when our salary arrives, ensuring essential expenses are covered before any discretionary spending can occur.

This systematic approach addresses the core issue behind India’s rising household debt levels – the lack of a proper emergency fund and structured expense management. We need to build a basic needs emergency fund equal to three months of essential expenses in a liquid mutual fund, while exploring additional income sources through freelancing, part-time work, or monetizing existing skills. We should use only cash or debit cards for discretionary spending to eliminate the temptation of credit dependency.

Step 4: Evaluate All Future Purchases Carefully

For future purchases, we must implement a comprehensive evaluation system that reveals the true cost of EMI financing. Before committing to any installment purchase, we should calculate the total amount we will pay over the entire tenure and compare it with the cash price. Apply the 10-10-10 rule by asking ourselves: Will I be happy about this purchase in 10 minutes, 10 months, and 10 years? We need to create mandatory waiting periods – 48 hours for purchases under ₹5,000, one week for ₹5,000-₹25,000, and one full month for anything above ₹25,000. This simple pause often reveals that the urgency was artificial and the purchase unnecessary.

Moving Forward: Your Action Plan to Save 30% Income

The path forward begins with a single decision today. With household debt to GDP reaching 41.3% and non-housing retail loans comprising 55% of total household debt, we cannot afford to delay action any longer. Start by choosing one debt to focus on completely – typically the one with the highest interest rate or smallest balance for psychological momentum. Transfer every available rupee beyond basic survival needs toward this single target until it disappears entirely.

Immediate Steps You Can Take This Week

Once we have this debt elimination strategy in place, small steps create lasting transformation when applied consistently. Open a separate savings account this week and commit to depositing just ₹500 every month, then gradually increase this amount by ₹100 each quarter. Set up automatic bill payments to eliminate late fees and reduce the temptation to use credit when cash flow becomes tight. These seemingly minor adjustments compound over time, creating the financial stability that protects us from future debt cycles.

Leverage Technology for Better Money Management

Technology can accelerate our progress significantly. Download a expense tracking app and commit to recording every transaction for the next 30 days, no matter how small. Most of us discover we spend 20-30% more than we realize, simply because cash and digital payments feel less tangible than physical money. Use this awareness to identify specific categories where we can redirect funds toward debt elimination and emergency fund building.

Develop Your Personal Lending Policy

Understanding our spending patterns helps us become more informed borrowers, which aligns with what financial experts recommend. The Reserve Bank of India notes that household debt remains manageable when lending practices stay prudent, but this requires us to become prudent borrowers as well. Create a personal lending policy that prohibits new debt until existing obligations are cleared, except for genuine emergencies or appreciating assets like property. Write down this commitment and review it whenever the temptation for instant gratification through EMIs arises.

Invest in Financial Education

Building financial literacy becomes crucial for long-term success, especially when understanding the true cost of borrowing and the power of compound interest working in our favor rather than against us. Read one personal finance article each week, listen to financial podcasts during commutes, or join online communities focused on debt reduction and wealth building. Knowledge transforms our relationship with money from reactive to strategic.

Your financial freedom journey starts with the next decision you make about money. Whether that decision involves declining an unnecessary purchase, making an extra debt payment, or simply tracking today’s expenses, each choice moves you closer to a life where money serves your goals rather than controlling your options. The data shows household debt to GDP is rising, but it also shows that millions of Indians are successfully managing their finances through deliberate, consistent action. You can join them starting right now.

FAQs

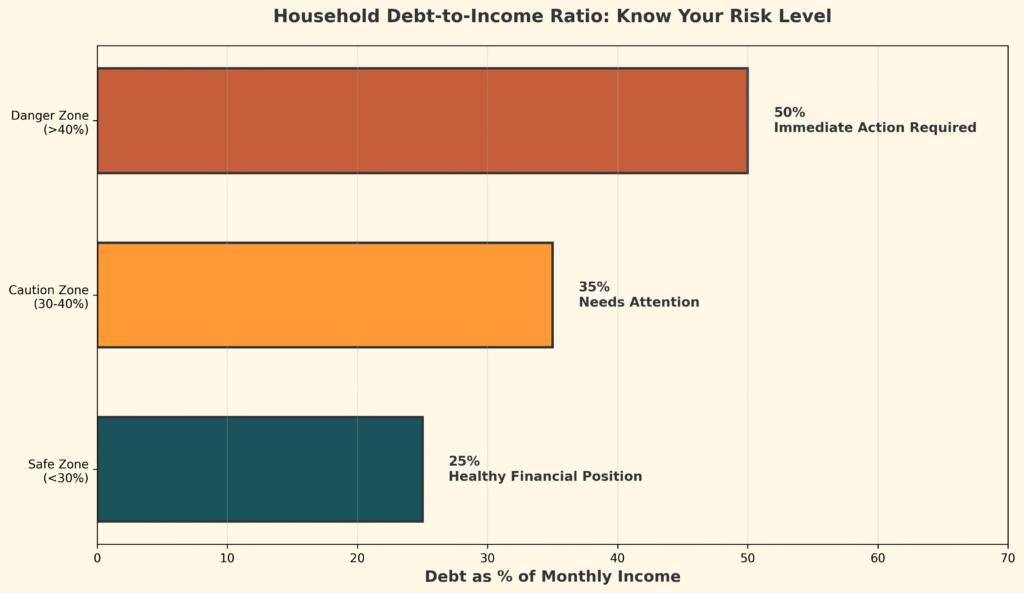

Q: How do I know if my household debt level is becoming dangerous? Calculate your total monthly debt payments as a percentage of your income. If it exceeds 40%, you’re in the danger zone. When you’re borrowing to pay existing debt or using credit for basic necessities like groceries, it’s time for immediate intervention.

Q: What’s the difference between good debt and bad debt in the Indian context? Good debt generates income or appreciates in value – like home loans or education loans that increase earning potential. Bad debt funds consumption or depreciating assets – credit cards for shopping, personal loans for weddings, or pawning jewelry for monthly expenses.

Q: What should I do if I’m already caught in a borrowing cycle? Stop taking new debt immediately. List all debts by interest rate and pay minimums on everything while attacking the highest-rate debt first. Consider debt consolidation only if it genuinely reduces your total interest burden and monthly outflow.